Municipals faced pressure outside of 10 years Wednesday, moving benchmarks on those bonds cheaper by two basis points, while U.S. Treasuries were little changed and new issues showed the spread tightening that continues on sought-after credits.

In the primary, an airport deal out of Pittsburgh saw compelling levels for the sector that has seen spread compression as it rebounds from COVID-related damage. To show the dramatic tightening on the short end, the A2-rated Allegheny County Airport Authority five-year bonds came a basis point richer than the gilt-edged state credit.

Maryland 5s of 2026 were bought at 0.42% Its five-year with a 5% coupon was priced plus four basis points to triple-As while its 10-year maturity of non-AMT bonds was +19 to benchmark yields. Maryland sold $614 million of general obligation bonds to wider spreads than triple-As on some maturities.

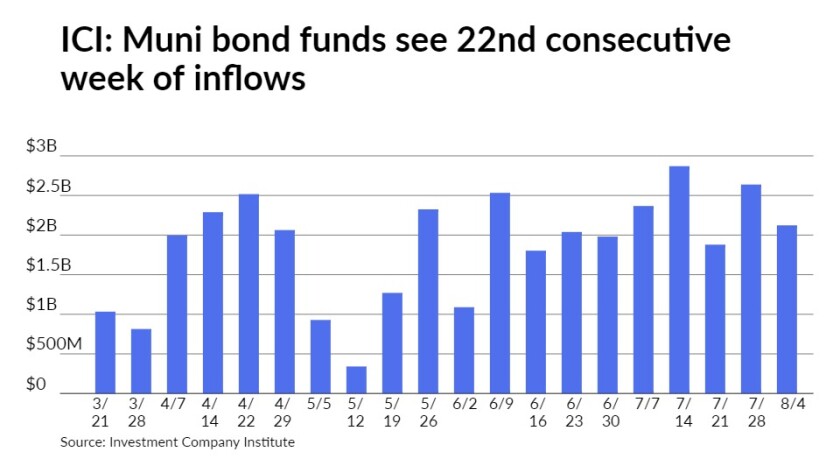

Another $2 billion-plus was reported flowing into municipal bond mutual funds in the latest week, continuing to be a supportive demand component for munis.

Citigroup Global Markets Inc. priced for the Allegheny County Airport Authority (A2//A/A+) $823.55 million of Pittsburgh International Airport AMT and non-AMT revenue bonds. The first, $711.13 million AMT, saw 5s of 2026 at 0.47%, 5s of 2031 at 1.26%, 5s of 2036 at 1.63%, 4s of 2036 at 1.77%, 4s of 2046 at 2.06%, 5s of 2051 at 2.03%, 5s of 2056 at 2.08% and 4s of 2056 at 2.23%. The second, $111.16 million non-AMT, saw 5s of 2026 at 0.41%, 5s of 2031 at 1.09%, 5s of 2036 at 1.43%, 4s of 2041 at 1.69%, 4s of 2046 at 1.84%, 5s of 2051 at 1.81% and 5s of 2056 at 1.86%.

Gilt-edged Maryland sold $539.95 million of exempt unlimited tax general obligation bonds to J.P. Morgan Securities. The first tranche, $258.95 million, saw bonds in 2026 with a 5% coupon yield 0.42% and 5s of 2031 at 0.94%. The second, $281 million, had 5s of 2032 at 1.00% and 4s of 2036 at 1.33%.

Wells Fargo won $75 million of taxable Maryland GOs: 2024 priced at par at 0.46% and 0.67% in 2025.

Goldman Sachs & Co. LLC priced for the CSCDA Community Improvement Authority, California (nonrated) $229.5 million of essential housing revenue social bonds. The first, $104.5 million, saw 3s of 2057 at 2.67%. The second, $75 million, with bonds priced at par at 2.45% in 2047. The last, $50 million, had 4s of 2057 at 2.90%.

The Investment Company Institute reported another week of inflows, $2.123 billion for the week ending August 4, down from $2.639 billion the week prior. The fund complex hit its 22nd consecutive week of inflows.

Exchange-traded funds saw a drop to $105 million of inflows versus $623 million the week before.

Total assets held now total $62 billion year-to-date, according to ICI.

A view from the buyside

Municipals remain attractive as an asset class, and could potentially outperform Treasuries as the summer comes to an end, depending on changing market technicals, buy-side analysts said this week.

In the near term, summer technicals have generated very visible net negative supply conditions, according to Jeff Lipton, managing director and head of municipal credit and market strategy and municipal capital markets at Oppenheimer & Co.

While municipals continued to show positive performance in July, they underperformed U.S. Treasuries with the year-to-date performance gap through July revealing further tightening from the prior month, Lipton said in a weekly report on Tuesday.

“If we see enduring Treasury market softness over the coming weeks, we believe that summer municipal technicals have the potential to push munis to outperform Treasuries over the near-term,” Lipton wrote.

Even with the elevation to higher yields, municipals remain historically rich to Treasuries, he added.

Municipal to UST ratios sat at 66% in 10 years and 74% in 30, according to Refinitiv MMD, while ICE Data Services had the 10-year at 67% and the 30 at 73%.

“If the outlook for the future tax bite stays muted for a while longer and we continue to receive heavier doses of hawkish Fed speak and higher inflation data points, yields may experience continued upward pressure,” he added.

However, Lipton said that scenario would likely be “distilled” given the summer technicals that are generating visible net negative supply conditions.

“We believe that munis still have the ability to generate positive performance, although admittedly such performance could be compromised should technicals become much less constructive and prospects for higher taxes fade considerably — even from currently elevated levels of doubt,” he said.

“While summer technicals should support muni performance, just how munis perform relative to U.S. Treasuries will be largely determined by the Treasury market’s response to Fed-speak and future inflationary data,” he said.

Even without a rise in federal tax rates, municipals should continue to offer “very desirable credit quality and diversification attributes,” which are expected to further entice foreign investment into the asset class, according to Lipton.

“Against this backdrop, we do not foresee a material loosening up in credit spreads or even a substantive reversal in the currently rich muni valuations that have characterized the market for some time now,” he said, adding that when technicals drivers alter course, he will be on the lookout for advantageous investment opportunities ahead.

Meanwhile, in a weekly report Bill Merz, director of fixed income at Minneapolis-based U.S. Bank Wealth Management, said that even though incremental yields over Treasuries on investment-grade corporate and municipal bonds are at or near all-time lows there is still value to be had.

“High-yield corporate and municipal bond yields are also low relative to the past, but can still provide meaningful income,” as well as low default rates for now, to remain low for now, according to Merz, who helps oversee $282 billion in assets under management.

Secondary scales

Refinitiv MMD saw levels steady at 0.06% in 2022 and at 0.08% in 2023. The yield on the 10-year steady at 0.88% while the yield on the 30-year rose two to 1.48%.

ICE municipal yield curve saw steady at 0.06% in 2022 and at 0.08% in 2023. The 10-year maturity was at 0.90% and the 30-year yield rose two to 1.46%.

The IHS Markit municipal analytics curve saw the one-year steady at 0.07% and the two-year at 0.08%, with the 10-year up one to 0.90%, and the 30-year yield up one to 1.46%.

Bloomberg BVAL saw levels at 0.06% in 2022 and 0.06% in 2023, while the 10-year rose one to 0.90% and the 30-year up two to 1.47%.

Treasuries were slightly lower while equities were mixed. The 10-year Treasury was yielding 1.328% and the 30-year Treasury was yielding 1.992% in late trading. The Dow Jones Industrial Average gained 219 points or 0.62%, the S&P 500 rose 0.25% while the Nasdaq lost 0.16%.

Informa: Money market muni funds fall

Tax-exempt municipal money market fund assets fell by $407.8 million, lowering their total to $91.16 billion for the week ending August 10, according to the Money Fund Report, a publication of Informa Financial Intelligence.

The average seven-day simple yield for the 157 tax-free and municipal money-market funds fell to 0.01% from 0.02% the previous week.

Taxable money-fund assets fell by $4.02 billion, bringing total net assets to $4.355 trillion. The average, seven-day simple yield for the 763 taxable reporting funds fell to 0.01% from 0.03% the prior week.

CPI rises modestly

The Consumer Price Index rose a seasonally adjusted 0.5% in July after rising an unrevised 0.9% in June, while the core rate also jumped 0.3% after a unrevised 0.9% gain in June.

Economists polled by IFR Markets had estimated CPI to rise 0.5% and the core to climb 0.4%.

On a year-over-year basis, the CPI was up 5.4%, its biggest 12-month increase since a 5.4% rise in August 2008. The core grew 4.3% on a year-over-year basis.

Economists anticipated an annual increase of 5.3% in CPI and 4.3% in core for the year.

“The CPI report adds credence to the argument that while inflation is high, it likely is at or near its peak,” said Scott Ruesterholz, portfolio manager at Insight Investment. “In particular, we are seeing signs that volatile categories that have driven much of the recent surge in prices, like rental cars and used cars, are moderating in keeping with high-frequency data like used car auctions, which point to normalizing prices.”

Core inflation is “starting to show signs of cooling from the pandemic-induced surge during the spring months, as some of that is due to the emergence of the Delta variant, which could dampen inflation in August,” said Diane Swonk, chief economist at Grant Thornton. “It is notable that the Delta variant is disrupting both supply and demand, which will leave the Federal Reserve uneasy as we move into the turn of the year. The Fed is still expected to taper its asset purchases; timing on rate hikes is still further out.”

Primary to come

The Triborough Bridge and Tunnel Authority is set to price on Thursday $450 million of MTA Bridges and Tunnels payroll mobility tax senior lien bonds. J.P. Morgan Securities LLC.

The City of Lubbock, Texas (A1/A+/A+/) is set to price on Thursday $254.32 million of electric light and power system revenue bonds. BofA Securities.

The Windy Gap Firming Project Water Activity Enterprise, Colorado (Aa2/AA//) is set to price on Thursday $165.665 million of Windy Gap Firming Project senior revenue bonds. Goldman Sachs & Co. LLC.

The University of North Dakota is set to price on Thursday $130.4 million of certificates of participation. Stifel, Nicolaus & Company, Inc.

Pecos-Barstow-Toyah Independent School District (/AAA//) (PSF Guarantee) is set to price on Wednesday $111.79 million of unlimited tax school building bonds, serials 2022-2041. RBC Capital Markets.

Aaron Weitzman contributed to this report.