Municipals were unmoved in light trading to start the last week of August while U.S. Treasuries maintained Friday’s levels and equities advanced on news the FDA gave the Pfizer COVID-19 vaccine full approval.

Municipal benchmark yield curves continued to hold steady for the seventh day as investors await a diverse primary that includes gilt-edged Montgomery County, Maryland, and low-rated Illinois in the competitive market and large transportation, airport, healthcare and housing credits in the negotiated space.

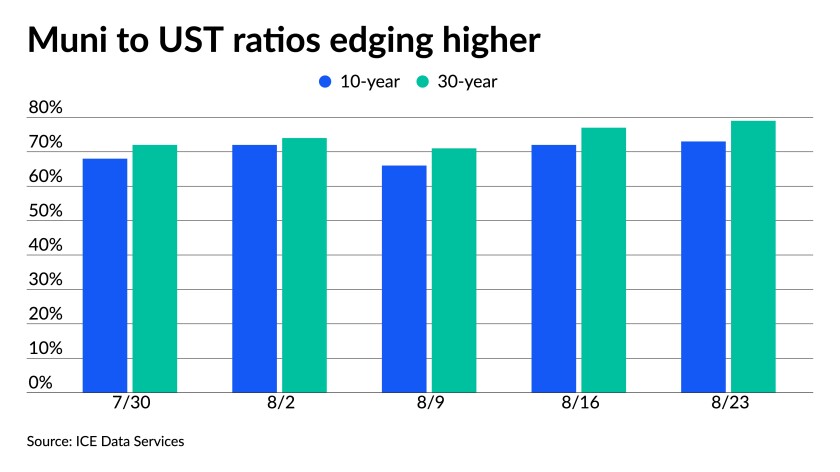

U.S. Treasuries gave little direction Monday while municipal-to-UST ratios held steady but have edged higher in August, leading some participants to argue yields and ratios are satisfactory to ride out the summer.

The 10-year muni-to-Treasury ratio was at 73% while the 30-year muni-to-Treasury ratio stood at 80%, according to MMD. The 10-year muni-to-Treasury ratio was at 73% while the 30-year muni-to-Treasury ratio stood at 79%, according to ICE.

Returns are still in the negative on the month for high-grades and high-yield, according to Bloomberg Barclays Indices, with the Municipal Bond Index at -0.29% for the month, +1.60% for 2021; the High-Yield Index has lost 0.09%, but is up 7.31% this year. Taxable munis have turned it around to positive 0.16% for August and 2.12% for the year after being in the red earlier in the month.

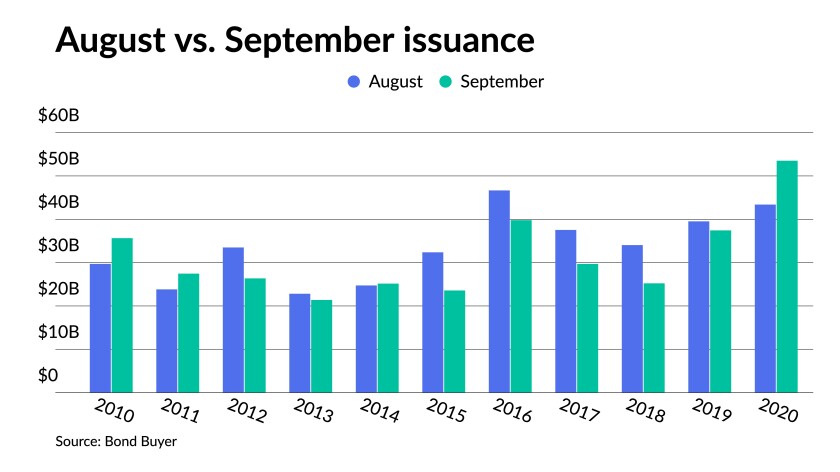

September issuance typically falls below August totals. But September’s dynamic looks a little different than the June-August period, as expected redemptions reach about $25 billion, or less than half that of August, noted Kim Olsan, senior vice president at FHN Financial.

Given that COVID-related federal relief dollars continue to roll in with the three largest municipal issuers — California, Texas and New York — to be allocated about $92 billion, “or about 3 months’ worth of national supply,” it could limit some issuers’ needs for more paper, she noted.

Net negative supply is $2.124 billion for California, $7.25 billion for Texas and $227 million for New York, per Bloomberg data.

Among those states whose budgets were more strained pre-COVID — Illinois, New Jersey and Pennsylvania — the federal monies total an estimated $36 billion. Net negative supply for New Jersey is $894 million and Pennsylvania is at $224 million while Illinois supply is $173 million in the positive. The federal monies “are certain to detract from financing needs related to debt refinancing or new-money efforts,” Olsan noted.

Bond Buyer 30-day visible supply sits at $10.7 billion with net negative issuance at $13.735 billion per Bloomberg data.

“Either way, a better matchup between money cycling in and out gives bidders potential flexibility in levels heading into the new month,” Olsan said.

NYC TFA plans $1.2B sale

After a large week of New York paper, the New York City Transitional Finance Authority said Monday it will issue about $1.2 billion of future tax-secured subordinate bonds next week.

The deal features $950 million of tax-exempt fixed-rate bonds and $250 million of taxable fixed-rates.

Book-running lead manager RBC Capital Markets is expected to price the tax-exempts on Sept. 1, after a two-day retail order period. BofA Securities, Citigroup, Jefferies, JPMorgan Securities, Loop Capital Markets, Ramirez & Co., Siebert Williams Shank, and Wells Fargo are co-senior managers.

Secondary trading and scales

Secondary trading was sparse with a few high-grade trades confirming steady levels. New York City 5s of 2022 traded at 0.06%. District of Columbia 5s of 2023 at 0.10%. Gwinnett County, Georgia, 5s of 2024 at 0.20%. Delaware 5s of 2026 at 0.32%.

Norfolk, Virginia, 5s of 2030 at 0.86%. Maryland 5s of 2030 at 0.85% (last block trade on Aug. 11 at 0.86%). Maryland 5s of 2031 at 0.91% and 5s of 2033 at 1.04%-1.03%, same as Thursday. Georgia 5s of 2033 at 1.03%.

According to Refinitiv MMD, short yields were steady at 0.06% and 0.08% in 2022 and 2023. The yield on the 10-year stayed at 0.88% while the yield on the 30-year sat at 1.50%.

The ICE municipal yield curve showed bonds unchanged in 2022 at 0.05% and up one basis point to 0.09% in 2023. The 10-year maturity sat at 0.91% and the 30-year yield remained at 1.48%.

The IHS Markit municipal analytics curve showed short yields steady at 0.06% and 0.08% in 2022 and 2023, respectively. The 10-year yield was at 0.90% and the 30-year yield at 1.49%.

The Bloomberg BVAL curve showed short yields steady at 0.06% and 0.06% in 2022 and 2023. The 10-year yield was at 0.89% and the 30-year yield at 1.49%, both steady.

In late trading, Treasuries were little changed as equities traded higher.

The 10-year Treasury was yielding 1.252% and the 30-year Treasury was yielding 1.87%. The Dow Jones Industrial Average gained 266 points or 0.76%, the S&P 500 increased 0.99% while the Nasdaq gained 1.61%.

Delta and Jackson Hole

As the Delta variant lifts the number of COVID cases and deaths, uncertainty grows as the economic impact likely rises.

“There may be strong resistance to more lockdowns but the numbers will no doubt take their toll on the economic recovery one way or another,” said Craig Erlam, senior market analyst, UK & EMEA, at OANDA. “The data in recent months has been fantastic but the outlook is becoming increasingly downbeat.”

And with questions about the outlook, could impact the Federal Reserve. “What was looking a fairly straight forward move now brings significant doubts,” Erlam said. “Jackson Hole looked the ideal platform for a taper warning but now, officials may be more inclined to see how the data unfolds over the weeks before the September meeting before dropping any major hints.”

Since Jerome “Powell has been very careful” about taper talk, “I would expect Friday’s speech to be another small step in that direction,” said Gary Pzegeo, head of fixed income at CIBC Private Wealth.

“We’ve heard a number of Fed governors and regional bank presidents favor a reduction in the Fed’s asset purchases beginning before the end of the year, but I don’t expect we’ll get an announcement on the start of tapering by Powell on Friday,” he added. “As with prior FOMC meetings, the latest Fed minutes show a difference in opinion on the timing of tapering among the Committee members.”

Besides the Fed’s stated concern about the Delta variant at its last meeting, Dallas President Rob Kaplan last week said if the rise hits consumer spending, he “could change his mind on tapering.”

While Powell will continue to state the Fed will move to taper if the economy goes as planned, “it seems the Fed would like to see more data before committing to a timeline,” Pzegeo said.

But, it remains unclear how the Delta variant will impact the economy. “High-frequency measures on seated diners and the number of people through TSA checkpoints suggest service activity has plateaued but not materially deteriorated,” Wells Fargo Securities said in a note. “The sideways move in activity, in conjunction with weaker-than-expected retail sales in July, suggests some downside risk to our personal spending estimates for the third quarter.”

And while worker shortages and supply chain issues appeared to ease in July, they said, “the latest surge in COVID cases puts the timeline of further improvement at risk.”

As for data released Monday, existing home sales jumped 2.0% in July to a seasonally adjusted annual rate of 5.99 million from a downwardly revised 5.78 million in June, first reported as 5.86 million.

Economists polled by IFR Markets expected a 5.81 million pace.

The number of homes available at the end of July grew 7.3% to 1.32 million units, but is off 12.0% from a year ago. The median sales price dipped to $359,900 in July from $362,800 in June, but still 17.8% higher than July 2020, when it was $305,600.

The number of first-time homebuyers also slipped in the month.

“The housing market appears to be moving back toward some semblance of balance this summer,” said Mark Vitner, senior economist at Wells Fargo Securities. High prices have led to more supply, which has “moderated ever so slightly, taking price gains down a notch from the mesosphere to the stratosphere.”

Also released Monday, the Chicago Fed’s National Activity Index climbed to positive 0.53 in July from negative 0.01 in June, while the three-month moving average, CFNAI-MA3, gained to positive 0.23 in July from positive 0.01 in June.

The Diffusion Index, also a three-month moving average, rose to positive 0.28 in July from positive 0.05 in June

The numbers suggest the economy is growing at an above average pace. “An increasing likelihood of a period of sustained increasing inflation has historically been associated with values of the CFNAI-MA3 above positive 0.70 more than two years into an economic expansion,” the Fed said.

Primary market to come

In the competitive market on Tuesday, Illinois (//BBB+/) is set to sell $130 million of junior sales tax Build Illinois Bonds at 10:30 a.m. eastern.

Montgomery County, Maryland, (Aaa/AAA/AAA/) is set to sell $335.25 million of general obligation bonds at 10 a.m.

Dallas, Texas, (/AAA/AA+/) is set to sell $127.55 million of waterworks and sewer system revenue refunding bonds at 11 a.m.

Wisconsin (/AAA/AAA/) is set to sell $100 million of environmental improvement revenue refunding green bonds at 10:45 a.m.

On Wednesday, Federal Way SD #210, Washington (Aaa///) is set to sell $107.25 million of unlimited tax general obligation bonds at 11:30 a.m.

In the negotiated market, The Pennsylvania Turnpike Commission is set to price on Tuesday $600 million of refunding bonds with $246.5 million oil franchise tax senior revenue bonds, Series A of 2021 (Aa3//AA/AA) serials 2021-2032, terms 2046, 2051; and $353.42 million oil franchise tax subordinated revenue bonds, Series B of 2021 (A2//A+/AA-), serials 2021-2032, 2037-2041 and terms 2046, 2051, 2053. Jefferies LLC.

The Hospital Authority of Hall County and Gainesville, Georgia, will sell $456 million of taxable revenue anticipation certificates (/AA/AA/) on Thursday for the Northeast Georgia Health System, Inc. project. BofA Securities.

The Utah Military Installation Development Authority is set to price $260 million of tax allocation and hotel tax revenue Series 2021A-1 and tax allocation revenue bonds Series 2021A-2 on Thursday. Piper Sandler.

Love Field Airport Modernization Corp. is set to price $246.72 million of Series 2021 AMT general airport revenue refunding bonds (/A-/) on Thursday. BofA Securities.

North Carolina is set to price $245.45 million of Series 2021 grant anticipation revenue vehicle bonds (A2/AA/A+/) on Wednesday. BofA Securities.

Campbell, California, Union High School District is set to price $224.76 million taxable GO bonds (AAA/AA+//). RBC Capital Markets.

Houston is set to price $210.27 million of airport system special facilities revenue bonds (//B-/) on Tuesday on behalf of United Airlines, Inc. terminal improvement projects. Citigroup.

New York City Housing Development Corp. is set to price $200 million of Series 2021 Series G multifamily housing revenue bonds (Aa2///) on Thursday. Ramirez & Co.

The Cleveland County Educational Facilities Authority (Aa3/A+//) is set to price $159.34 million of Moore Public Schools Project lease revenue bonds, 2022-2031. D.A. Davidson & Co.

The Wisconsin Public Finance Authority (nonrated) is set to price on Tuesday $153 million of Sky Harbour Capital LLC Aviation Facilities Project senior special facility revenue bonds. Goldman Sachs & Co. LLC.

The North Carolina Housing Finance Agency (Aa1/AA+//) is set to price on Thursday $150 million of home ownership revenue bonds, series 47 (non-AMT) (1998 Trust Agreement), serials 2022-2033, terms 2036, 2041, 2044, 2051. Wells Fargo Corporate & Investment Banking.

Denton, Texas, (/A+/A+/) is set to price on Thursday $141 million of utility system revenue refunding bonds, taxable series 2021. Citigroup Global Markets Inc.

The City of Miami Beach Health Facilities Authority (Baa1//A-/) is set to price on Wednesday $139.325 million of Mount Sinai Medical Center of Florida hospital revenue bonds, serials 2030-2041, terms 2046, 2051. Raymond James & Associates, Inc.

The City and County of Broomfield, Colorado, (Aa2///) is set to price on Tuesday $132.61 million of water activity enterprise revenue bonds, serials 2022-2043, term 2046. Wells Fargo Corporate & Investment Banking.

The California Community Housing Agency is set to price on Wednesday $129.595 million of essential housing revenue bonds, series 2021A-1 senior bonds (non-AMT), Series 2021A-1T senior bonds (federally taxable), Series 2021A-2 junior bonds (non-AMT), (The Exchange ay Bayfront Apartments). Jefferies LLC.

The North Fort Bend Water Authority, Texas, (/AA//) is set to price on Tuesday $119.52 million of water system revenue and revenue refunding bonds, Build America Mutual Assurance insured. Piper Sandler & Co.

Tacoma, Washington, (/AA/AA-/) is set to price on Wednesday $118.26 million of electric system revenue green bonds, serials 2036-2041, terms 2046, 2051. Citigroup Global Markets Inc.

The Tennessee Housing Development Agency (Aa1/AA+//) is set to price on Wednesday $99.99 million of residential finance program social bonds, serials 2022-2033, terms 2036, 2041, 2046, 2051, 2052. RBC Capital Markets.