We sell a short competitive refunding. The financial advisor informs us of the low bid, and we make the award. Then, the FA resizes the maturities for the coupons on the winning bid.

Because it is a competitive bid, we know we got the best deal available, the only problem is, we didn’t.

What went wrong? Could we potentially have done better for our constituents? The answer lies with our choice of couponing. When an issuer selects the winning bid prior to resizing it can sometimes result in a suboptimal structure as a higher bid with lower coupons can lead to a lower all-in yield with the lowest debt service after resizing.

We must remember that we are issuers not traders. When it comes to non-callable bonds, we need to stop focusing on individual bond yields, because what we really care about is overall portfolio debt service and the proceeds generated. These may sound like the same thing, but they are not.

For an issuer that uses a level debt structure (or any other structure with a specific debt profile), the coupon selected for one maturity impacts the relative sizing of the maturities around it. For example, in a level debt structure, lowering the coupon in one maturity increases the par size of the shorter maturities, which in turn lowers the structure’s average maturity. When combined with a positively sloping yield curve, using lower coupon non-callable bonds lowers total debt service and all-in yields. The steeper the slope of the yield curve, the greater the benefit of lower coupon bonds.

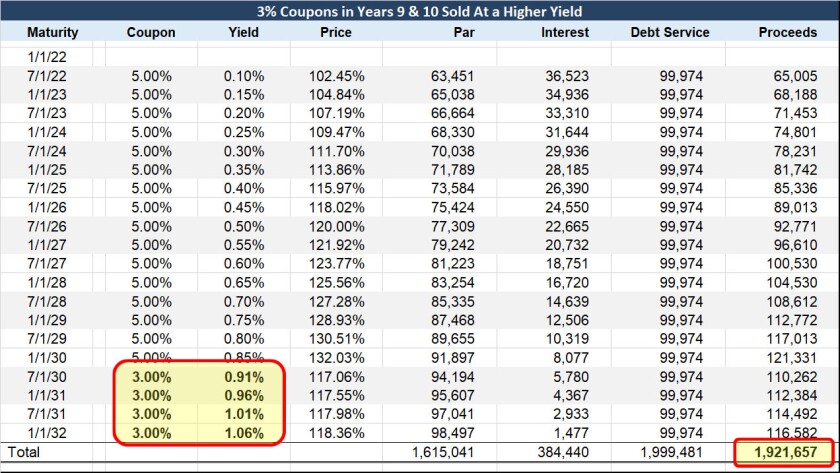

The example below shows a yield curve with a slope of 10 basis points per year (5 basis points every 6 months). In this example, the issuer is better off selling bonds with 3% coupons than 5% coupons in years 9 and 10. This is true even if the 5% coupons enabled the issuer to sell these bonds 1 basis point tighter.

The lower coupon (even with the higher yield) results in the same proceeds, lower debt service and lower transaction yields (0.762% vs. 0.767%). If the 3% coupons are sold at the same yield as the 5% coupons, the lower coupon approach has a 1 basis point benefit in transaction yield.

What can issuers do? For starters, we can award competitive transactions to the bid that produces the lowest yield after resizing.

As for negotiated sales, issuers should strongly consider offering lower coupon, non-callable bonds, especially in the longer non-callable maturities.

What if there is no market for lower coupons? As issuers we can drive the market. Looking back to the days of Build America Bonds (BABs), we were told that there was no market for premium taxable bonds. However, when having a premium became the key to a winning bid, suddenly everyone sold premium BABs.

Ultimately, issuers must remember that they are issuers. When it comes to non-callable bonds, for most issuers, once pricing is over, we have bond proceeds and debt service.

Our goals should be focused on these two outputs. Coupons, insurance, and original yields are not relevant. We must focus on minimizing debt service and/or maximizing proceeds. That means selling lower coupon non-callable bonds when possible. For competitive transactions, it could mean awarding the winning bid based on the resized structure as opposed to the preliminary structure.

With interest rates expected to rise, and mom and pop retail expected to become more relevant, there may be an opportunity for issuers to save money in a part of the curve that has been ignored for too long.

Phil Wasserman is Deputy Budget Director of the Nassau County Office of Management and Budget.