Municipals were weaker amid larger losses in U.S. Treasuries while equities ended mixed as markets were quieter ahead of the FOMC rate-hike decision Wednesday.

Triple-A benchmark yields were cut five to eight basis points, depending on the scale, while USTs rose six to 11 basis points.

Muni-to-UST ratios were at 66% in five years, 84% in 10 years and 99% in 30, according to Refinitiv MMD’s 3 p.m. read. ICE Data Services had the five at 67%, the 10 at 83% and the 30 at 98% at a 4 p.m. read.

In the primary, J.P. Morgan Securities priced for Riverside County, California, $360 million of 2022 tax and revenue anticipation notes, with 5s of 6/2023 at 2.15%, noncall.

BofA Securities priced for Washington (/AA//) $118.1 million of federal highway grant anticipation revenue refunding bonds, Series R-2022E, with 5s of 9/2022 at 1.55% and 5s of 2024 at 2.33%, noncall.

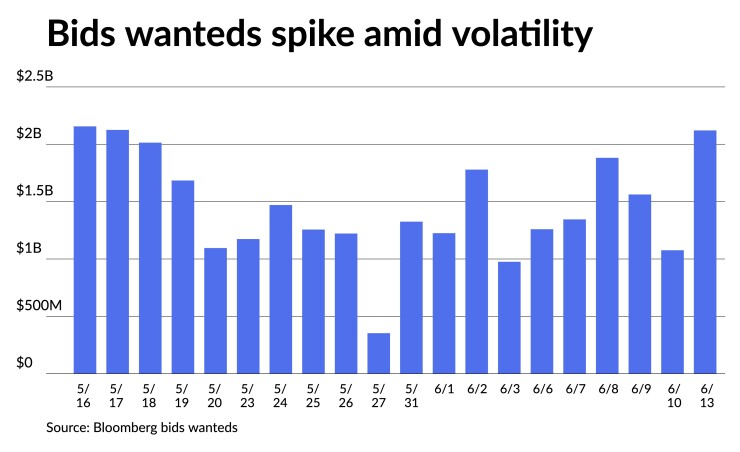

Bids wanteds spiked Monday amid the volatility, with Bloomberg’s bid system tally reaching $2.1 billion. This is 70% above the 2022 average and marks the 11th time this year the figure has exceeded $2 billion.

Volatility somewhat eased Tuesday as investors took pause ahead of the Federal Open Market Committee meeting. A half-point rate hike was expected, but the hotter-than-expected inflation report released Friday has some increasing the bets on 75 basis points instead.

“Seventy-five is very much on the table,” said Michael Contopoulos, director of fixed income at Richard Bernstein Advisors. And while Fed officials ruled out the larger hike before the latest inflation data, he said, “the Fed has been just as clear about it being data-dependent.”

Municipal Market Analytics expects a tumultuous time ahead for the municipal market, with rampant inflation and deteriorating consumer confidence hanging over, leading to higher yields and lower prices. With the potential 75-basis-point rate hike on Wednesday, more pain will be felt at the front end of the yield curve.

The growing risk of recession threatens long-end losses, further flattening or inverting the UST curve.

“These twin risks indeed threaten municipals from both a bond and credit performance perspective, but tax-exempt bonds are also being carried by strong, endogenous factors (i.e., persistent bond scarcity, upward rating momentum, and very constructive credit prospects for core [investment grade] borrowers) that imply continued outperformance of taxables and a still-very-investible framework through year-end, but risks after that are rising,” according to the report.

“New buyers should also be looking to get ahead of what may well be persistent volatility in the coming months by focusing allocations on higher coupon, higher grade, intermediate maturity structures,” the report noted.

The potential for munis to outperform UST is based on the supply-demand imbalance for the rest of the year. A majority of the $150 billion of tax-exempt principal slated to mature or be called by the year’s end is expected to be reinvested into muni securities, despite new issuance of tax-exempts continuing to “underwhelm.”

A first-quarter report from the Fed showed a $20 billion dip in the size of the outstanding municipal market, an indication that new issuance has slowed due to amortization. Indeed, volume is down year-over-year and many market participants are downsizing expectations for 2022’s supply prospects.

Aggregate municipal credit quality is also in limbo under current economic conditions. While a recession would negatively impact municipal credit quality, ongoing inflation is a “near-term positive as it amplifies property, income, sales, and special tax revenues that, with the upcoming drop in capital gains tax receipts, will be needed in FY23,” according to the report.

“Most states are sitting on unusually large capital reserves and expecting additional budget surpluses. All these are constructive for near-term rating prospects,” according to MMA.

“By FY24 however, the revenue effects of any actual economic weakness will be exacerbated by widespread state tax cuts being implemented now (and which will encourage state aid cuts to locals going forward), not to mention what could be material downside budget surprises for pension obligation bond borrowers, real estate dependent credits, and the health care sectors (acute care and senior living), to the detriment of related investor demand and credit spreads,” the report said.

Muni CUSIP requests rise

Municipal request volume rose in May, following a decrease in April, according to CUSIP Global Services. For muni bonds specifically, there was an increase of 11.1%, though requests are down 15.7% year-over-year.

The aggregate total of identifier requests for new municipal securities, including municipal bonds, long-term and short-term notes, and commercial paper, climbed 16.3% versus April totals. On a year-over-year basis, overall municipal volumes were down 15.3%.

Secondary trading

Prince George’s County 5s of 2023 at 1.81%-1.79%. Maryland 5s of 2024 at 2.21%-2.11%.

Baltimore County 5s of 2025 at 2.29%-2.24%. Mecklenburg County, North Carolina, 5s of 2026 at 2.41%-2.34%.

Maryland 5s of 2027 at 2.45% versus 2.35% Monday. California 5s of 2028 at 2.76%. Maryland 5s of 2029 at 2.72% versus original 2.30%.

New York City 5s of 2029 at 3.02%. Anne Arundel County, Maryland, 5s of 2029 at 2.71%. Washington 5s of 2031 at 2.96%-2.95%. Loudoun County, Virginia, 5s of 2033 at 3.18%.

Washington 5s of 2037 at 3.57%. Washington 5s of 2039 at 3.61%-3.40%. California 5s of 2041 at 3.62% (2.88% on 6/1).

New York City TFA 5s of 2045 at 4.11%-4.10%. NYC TFA 5s of 2047 at 4.11%-4.10%. NYC 4s of 2051 at 4.56%-4.55% versus 4.35% Friday.

AAA scales

Refinitiv MMD’s scale was cut six to eight basis points at the 3 p.m. read: the one-year at 1.72% (+6) and 2.06% (+6) in two years. The five-year at 2.36% (+6), the 10-year at 2.91% (+8) and the 30-year at 3.38% (+6).

The ICE municipal yield curve saw cuts of five to six basis points: 1.73% (+6) in 2023 and 2.08% (+5) in 2024. The five-year at 2.39% (+6), the 10-year was at 2.83% (+6) and the 30-year yield was at 3.36% (+6) at a 4 p.m. read.

The IHS Markit municipal curve saw seven basis point cuts: 1.75% (+7) in 2023 and 2.09% (+7) in 2024. The five-year at 2.36% (+7), the 10-year was at 2.92% (+7) and the 30-year yield was at 3.38% (+7) at 4 p.m.

Bloomberg BVAL saw five to seven basis point cuts: 1.74% (+5) in 2023 and 2.03% (+6) in 2024. The five-year at 2.37% (+6), the 10-year at 2.89% (+7) and the 30-year at 3.36% (+7) at a 4 p.m. read.

Treasuries sold off.

The two-year UST was yielding 3.424% (+6), the three-year was at 3.580% (+9), the five-year at 3.590% (+11), the seven-year 3.573% (+11), the 10-year yielding 3.473% (+10), the 20-year at 3.717% (+10) and the 30-year Treasury was yielding 3.434 (+8) at the close.

FOMC preview: Will they go 75?

With inflation data showing no real signs of letting up, some analysts now think the Federal Open Market Committee could surprise with a 75-basis-point rate increase instead of the 50-basis-point climb that officials have promoted.

Wells Fargo Securities Chief Economist Jay Bryson and Economist Michael Pugliese believe “it is likely that the Committee will opt to hike rates by 75 bps, which would take the target range for the fed funds rate to 1.50% to 1.75%.”

They said reports of a 75-basis-point increase were “likely were confirmed by off-the-record comments by Fed officials,” who couldn’t comment because of the pre-meeting blackout period.

And while an extra 25-basis-points at this meeting “would definitely rattle that equilibrium,” said Jan Szilagyi, CEO of Toggle, “Friday’s inflation number was an unwelcome surprise to both policymakers and markets and diminished hopes for short-term relief from rising rates.”

But, the Fed has other tools it can use, he said. “In particular, they can raise borrowing costs for longer-dated loans by signaling a faster pace of hikes, or a higher ending point.”

While the markets wonder about the possibility of a 75-basis-point increase, a 50-basis-point increase has been priced in, said Wilmington Trust Chief Economist Luke Tilley.

“We think a 50bp hike is more likely,” he said, “but accompanied by comments from [Fed Chair Jerome] Powell that a 75 bp hike in July would be on the table, or perhaps even the baseline expectation.”

The two biggest risks for the Fed are moving too slowly or ending the hiking cycle too soon, Szilagyi said. “This calls for a nimbler tool than merely hiking the benchmark rate in surprisingly large increments. Markets would lose faith in the Fed that hiked for two meetings, then eased only to hike again at the following one. Forward guidance, on the other hand, can be much more finely tuned.”

But talk alone won’t solve the inflation problem, said Eric Winograd, senior economist at AllianceBernstein. And while “there are no good answers,” the Fed must stay hawkish, he said.

“While they might be tempted to believe that they could accomplish their goals this week simply with words, I doubt that will be enough to get the job done — I think they will have to do something more tangible than just talking tough,” Winograd said.

One option is raising more than 50 basis points, he noted, or “they could indicate that they are willing to raise rates by more than 50 bps in July, having previously signaled that 50 bps was likely at that meeting.”

Other options would be to extend the guidance for 50-basis-point moves beyond July, or “significantly increase the terminal rate forecast for this cycle, making clear that they anticipate moving rates into meaningfully restrictive territory,” Winograd said.

But a 75-basis-point increase at this meeting “is unlikely, he said. “They have been careful to preserve forward guidance as a policy tool throughout this cycle, and intentionally surprising the market this week would pose risks their ability to conduct monetary policy in the future.”

Others agreed that the half-point hike is the likely outcome of this meeting.

“I still think 50 bps is the call,” said Joe Boyle, fixed income product manager at Hartford Funds. “That said, the possibility of 75 bps and even 100bps has increased and if the Fed feels that level of hikes is necessary, I’d expect [Fed Chair Jerome] Powell to indicate as such. The market will be all ears during this press conference.”

If the Fed does raise rates by three-quarters of a point it “would be a happy” surprise, said Nancy Tengler, CEO & CIO of Laffer Tengler Investments. “The question now is whether the economy can avoid recession.”

While the four recession indicators she watches — the yield curve, credit spreads, leading economic indicators and the unemployment rate — aren’t signaling a recession, they “could at any time,” Tengler said.

Wells Fargo’s Bryson and Pugliese expect “a meaningful upward shift in the so-called dot plot, which would indicate that Fed policymakers believe even more monetary tightening is appropriate in coming quarters.”

At yearend, they expect a fed funds rate target of 3.375% and 4.125% at the end of 2023.

Also, look for higher inflation and lower growth forecasts in the Summary of Economic Projections, Bryson and Pugliese said. The March SEP suggested 4.3% inflation this year. “We would not be surprised if the June SEP has a median projection north of 5%.”

But future inflation projections shouldn’t rise much as the Fed expects “food and energy prices [will] decelerate and perhaps even decline somewhat in 2023 and beyond.”

GDP growth, estimated at 2.8% in the previous SEP could fall to between 2.0% and 2.25%, they said, as Wells Fargo projects 1.7% growth this year.

“The public is losing patience on inflation and there are loud calls for the Federal Reserve to boost interest rates more aggressively,” said David Kelly, chief global strategist at J.P. Morgan Asset Management. “However, powerful forces outside the Fed’s control largely caused the current inflation spike and a reversal of those other forces will likely cure it. For the Fed, the most important task is to recognize the strength of those forces and maintain a balanced and flexible approach to allow inflation to fade without triggering a recession.”

The post-meeting statement, he said, will likely “first emphasize the undesirable persistence of inflation pressures seen in a red-hot May CPI report and continued very high energy prices. They may note that the decline in the unemployment rate has slowed but they will likely assert that labor markets remain very tight.”

While the markets see a 50-50 chance the Fed will raise 75 basis points, Kelly said, “were they to do this, we would likely see both a further increase in short-term rates and a decline in long-term rates as investors bet more heavily on rate hikes in 2022 leading to recession in 2023.”

Inflation projections could rise to 5.5% for headline inflation, with a slight increase in core projections.

“There will be more dots in the Fed dot plot this time around with the addition of Lisa Cook and Philip Jefferson to the Board of Governors,” he noted. But still “the median forecast for the end-of-2022 federal funds rate [is] likely to climb from 1.9% in March to at least 2.6% and possibly 2.9%. 2.6% would reflect 50 basis point hikes in June and July and 25 basis point hikes in the three remaining meetings of the year. 2.9% would presumably reflect an expectation that the September hike is likely to be 0.5% rather than 0.25%.”

DWS Group U.S. Economist Christian Scherrmann is eying the SEP. “We are especially keen to see how members diverge in their expectations for 2023 and 2024. Might one or more of the FOMC members already be secretly penciling in a downturn? If so, it would provide an early clue of how seriously the Fed is likely to take market fears of a recession during its next few meetings.”

But he expects no “major surprises” at the meeting. “We expect the Fed to reassess the stance of monetary policy, and inflation, in August and see the September meeting as potential pivot point.”

But Sebastien Galy, senior macro strategist at Nordea Asset Management, says the “economy is potentially headed for a slow train wreck as the Fed is forced to tighten policy more quickly and raise interest rates higher to appease fears of consumers and some corporates, when in reality monetary policy works with a lag.”

If they overtighten, he said, it could lead to recession. “An economic equilibrium which was uncertain between a slowdown, stagflation and recession is becoming ever clearer as inflation widens out forcing the hand of the Fed,” he said. “The question now is whether the Fed can control the narrative again and dampen expectations regarding the terminal rate.”

Even if the Fed decides on a 50-basis-point hike, Galy said, “a more rapid pace of rate hikes is unlikely to be well received.”

Primary to come:

The Public Finance Authority, Wisconsin, (Baa2///) is set to price Thursday $275 million of taxable federal lease revenue bonds, Series 2022. Mesirow Financial Inc.

The Aurora Highlands Community Authority Board, Colorado, is set to price Thursday $163 million of special tax revenue bonds, Series 2022. Jefferies LLC.

Gabriel Rivera contributed to this report.