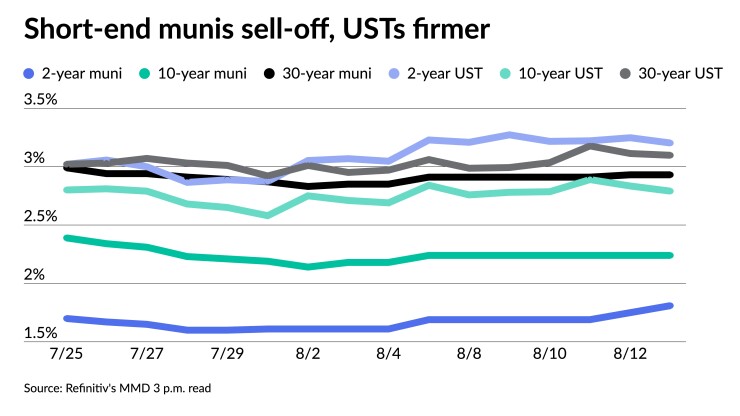

Short-end munis extended their days long selloff, continuing to play catch up to short-end U.S. Treasuries, as triple-A munis correct from recent outperformance relative to taxables. USTs were firmer, while equities were up near the close.

Triple-A benchmarks rose 11 to 15 basis points on the one-year and three to eight basis points in two years. The one-year yield is now higher than the two- to five-year. The rest of the muni curve was little changed. UST yields fell up to five basis points on the short end.

Short muni-UST ratios rose with the two- and three-year ratios at about 56%. The five-year was at 63%, the 10-year at 80% and the 30-year at 95%, according to Refinitiv MMD’s 3 p.m. read. ICE Data Services had the five at 62%, the 10 at 84% and the 30 at 93% at a 3:30 p.m. read.

“Much of fixed income is having a rough August, but some disparities in returns for tax-exempts show that this month’s losses have more to do with macroeconomic factors than credit-specific issues,” said Eric Kazatsky, head of municipal strategy at Bloomberg Intelligence.

“Demand for low-duration tax-exempts has been so strong that short maturity benchmark yields are now lower than the after-tax yields for comparably rated benchmark taxable muni and corporate bonds,” said CreditSights strategists Pat Luby and John Ceffalio.

Kazatsky noted, “the very front end of the municipal curve has lost much ‘value’ over the summer months.”

“Some richening has come as the municipal market contends with seasonally heavy cash flows,” he said. “Money managers also may be avoiding meaningful duration until more clarity on inflation and the Federal Reserve’s path is known.

“Whatever the reason, ratios for the two-year sector of the municipal curve” declined to 52% Monday from 89% as of mid-May.

“The past week of muni underperformance in the two-year tenor,” Kazatsky said, led to “some breathing room for short-exempt valuations and could be a harbinger of further normalization now that we’re past the wave of returning cash.” Before 2020, historical averages for muni-to-UST ratios in this part of the curve were 110%.

But outside of the one- and two-year triple-A benchmarks, the second week of August saw yields remain unchanged with yields on 10-year notes remaining at 2.26%, as of Friday, said Jason Wong, vice president of municipals at AmeriVet Securities.

Munis “continue to outperform Treasuries with the 10-year portion of the curve yielding 79.91% compared to the prior week when the ratios were at 80.10%,” he said, noting “the 10-year portion of the curve also performed the best compared to the rest of the curve which only outperformed treasuries slightly.”

The muni curve, though, flattened for the week to 124 basis points, “as the short end rose while the long end remained relatively unchanged,” he said.

The new-issue volume grows this week to $10.728 billion led by a $2.7 billion taxable Massachusetts social bond deal — the largest muni ESG yet — that had been delayed by some last-minute legislative spending debate that did not come to pass.

This, Wong said, is “larger than usually expected for 2022” and a good sign to see “larger issuers return to the markets as investors have been in need of supply.”

And given the heavy new-issue supply that is scheduled, CreditSights strategists expect that “yields and spreads in the one- to 10-year part of the tax-exempt market will have to cheapen if institutional demand (that is, from non-retail corporate buyers subject to the 21% corporate income tax rate) will be needed to clear this week’s deals.”

NYC TFA to sell $1.1B deal

The New York City Transitional Finance Authority said it will issue $1.1 billion of future tax-secured subordinate bonds next week.

The deals consist of about $990 million of tax-exempt fixed-rate bonds and $100 million of taxable fixed-rate bonds.

Book-running lead manager Ramirez & Co. is expected to price the tax-exempts on Aug. 24 after a one-date retail order period on Aug. 23. Citigroup and Jefferies are co-senior managers.

The TFA also plans to sell $100 million of taxables in the competitive market Wednesday.

Proceeds from the sale will be used to refund outstanding bonds for savings.

Secondary trading

Massachusetts 5s of 2023 at 1.89%. North Carolina 5s of 2023 at 1.91%-1.90%. LA DWP 5s of 2023 at 1.86% versus 1.79%-1.78% Friday. Georgia 5s of 2023 at 1.91%-1.90%. NYC 5s of 2023 at 2.04%-2.02% versus 1.81% Tuesday.

Georgia 5s of 2024 at 1.75%. North Carolina 5s of 2024 at 1.83%. Washington 5s of 2024 at 1.99%. California 5s of 2024 at 1.67%. NY MTA 5s of 2024 at 2.05%-2.01%. DC 5s of 2024 at 1.90%.

North Carolina 5s of 2027 at 1.90%. California 5s of 2027 at 1.86% versus 1.82% Thursday. Minnesota 5s of 2030 at 2.15% versus 2.13% original on 8/10.

Washington 5s of 2038 at 2.92% versus 2.85%-2.86% on 8/8.

AAA scales

Refinitiv MMD’s scale saw a 13-basis-point cut on the one-year at the 3 p.m. read: the one-year at 1.87% (+13) and 1.81% (+6) in two years. The five-year at 1.82% (unch), the 10-year at 2.24% (unch) and the 30-year at 2.93% (unch).

The ICE AAA yield curve was cut on the short end: 1.92% (+16) in 2023 and 1.80% (+4) in 2024. The five-year at 1.84% (+1), the 10-year was at 2.29% (unch) and the 30-year yield was at 2.91% (unch) at 4 p.m.

The IHS Markit municipal curve was cut on the front end: 1.83% (+11) in 2023 and 1.84% (+8) in 2024. The five-year was at 1.83% (unch), the 10-year was at 2.24% (unch) and the 30-year yield was at 2.93% (unch) at a 3 p.m. read.

Bloomberg BVAL was weaker on the short end: 1.78% (+11) in 2023 and 1.82% (+7) in 2024. The five-year at 1.84% (unch), the 10-year at 2.24% (-1) and the 30-year at 2.96% (+1) at 4 p.m.

Treasuries were firmer at the close.

The two-year UST was yielding 3.201% (-5), the three-year was at 3.130% (-5), the five-year at 2.911% (-5), the seven-year 2.860% (-4), the 10-year yielding 2.789% (-5), the 20-year at 3.311% (-2) and the 30-year Treasury was yielding 3.098% (-1) at 3:45 p.m.

NY Fed Index posts second largest decline on record

The New York Fed’s Empire State Manufacturing Survey fell 42.4 points to -31.3 in August, marking the second largest decline on record.

This comes “at a time when financial markets are coming to grips with whether the economy is currently in recession or heading into one, this is not an encouraging development for measures of industrial production,” said Wells Fargo economists Tim Quinlan and Shannon Seery.

However, “this is just one monthly report for one region of the country (albeit an important one), and it is not cause for full-blown alarm,” they said. “But coming on the heels of back-to-back declines in manufacturing production for the broader economy, the sudden drop in activity should not be dismissed out of hand.”

New orders dropped 35.8 points to -29.6 in August, and shipments cratered. The 49.4 point drop between July and August ranks third among the biggest monthly swings on record, Wells Fargo economists said.

“The strength of the job market is still the best argument for why the economy is not in recession at present,” they said, but “there was some deterioration evident in today’s Empire survey for the job market in the New York area.”

“The number of employees fell to 7.4 from 18.0 last month, and the average workweek fell to -13.1 showing a decline in hours worked,” according to Quinlan and Seery.

“To the extent that there was “good” news, the prices paid measure came in at 55.5 versus 64.3 in the prior month,” they said.

Primary to come:

Massachusetts (Aa1//AAA/AAA) is set to price $2.69 billion of taxable special obligation social revenue bonds (unemployment trust fund); $2.001 billion Series A, serials 2023-2032; $639.35 million Series B, term 2033. Jefferies LLC.

The Oklahoma Development Finance Authority (Aaa//AAA/) is set to price $1.354 billion of taxable ratepayer-backed Oklahoma Natural Gas Company bonds. J.P. Morgan Securities LLC.

The Regents of the University of California (Aa2/AA/AA/) is set to price on Wednesday $1.25 billion of general revenue bonds $713.23 million of exempt general revenue bonds, Series BK, $65.24 million of Series BL taxable, and $318.625 million of Series BM forward-delivery bonds. Goldman Sachs & Co. LLC

New York City (Aa2/AA/AA-/AA+) is set to price on Wednesday (retail Tuesday) $950 million of general obligation bonds, serials 2024-2029, 2033-2046. Jefferies LLC.

The Eagle Mountain-Saginaw Independent School District, Texas, PSF guarantee, is set to price $185.64 million of unlimited tax school building bonds, serials 2023-2052. HilltopSecurities.

The Equitable School Revolving Fund (/A//) is set to price on Wednesday $164.455 million of national charter school revolving loan fund social revenue bonds via the Arizona Industrial Development Authority, serials 2027-2042, terms 2047, 2052. RBC Capital Markets.

Dallas County, Texas, (/AAA//) is set to price on Wednesday $150 million of certificates of obligation, serials 2023-2042. Ramirez & Co., Inc.

The Fort Worth Independent School District (Aaa///) is set to price on Wednesday $135.185 million of unlimited tax school building bonds, PSF guaranteed, serials 2023-2042, term 2047. Siebert Williams Shank & Co., LLC.

The Fresno Unified School District, California, (Aa3///) is set to price on Tuesday $125 million of general obligation bonds. Stifel, Nicolaus & Company, Inc.

The Community Facilities District No. 2021-1 of Orange County, California, is set to price on Wednesday $118.720 million of Series A of 2022 special tax bonds. Piper Sandler & Co.

Competitive:

Miami-Dade County, Florida, (/AA/AA/) is set to sell $479.735 million of transit system sales surtax revenue bonds, Series 2022, at 10:30 a.m. eastern Tuesday.

Mecklenburg County, North Carolina, (Aaa/AAA/AAA/) is set to sell $451.335 million of general obligation school bonds at 11 a.m. Tuesday.

Minneapolis, Minnesota, (//AA+/) is set to sell $123.635 million of general obligation bonds at 11 a.m. Wednesday.

New York City (Aa2/AA/AA-/AA+) is set to sell $125 million of taxable general obligation bonds at 11:15 a.m. Wednesday.

Chip Barnett contributed to this story.