Long-end munis were much weaker Wednesday while a large new-issue from the New York City Transitional Finance Authority took focus in the primary. U.S. Treasuries were saw losses along the curve and equities made gains ahead of the Jackson Hole event that starts Thursday.

Triple-A municipal yields rose two to 10 basis points with the largest losses out long, while U.S. Treasuries saw larger increases in yields on the front end of the curve.

The moves had muni-UST ratios hovering around recent levels, with the two- and three-year ratios around 66%. The five-year was at 70%, the 10-year at 82% and the 30-year at 97%, according to Refinitiv MMD’s 3 p.m. read. ICE Data Services had the five at 70%, the 10 at 84% and the 30 at 94% at a 4 p.m. read.

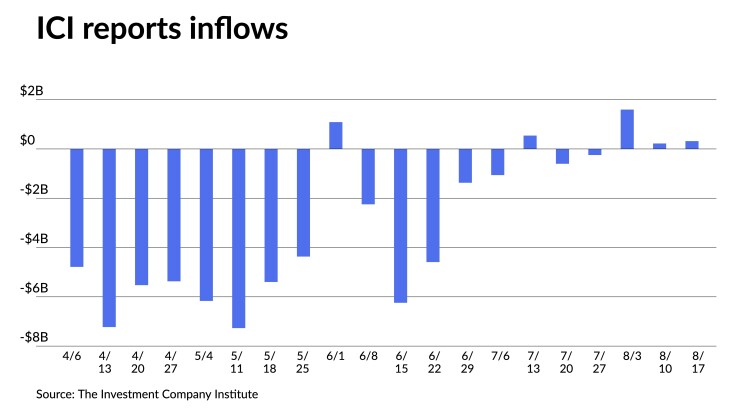

The Investment Company Institute reported $230 million of inflows into muni bond mutual funds in the week ending August 17 compared to $223 million of inflows the previous week.

Exchange-traded funds saw outflows of $200 million versus $379 million outflows the week prior, marking the second week in a row of outflows, per ICI data.

In the primary Wednesday, Ramirez & Co. priced and repriced for the New York City Transitional Finance Authority (Aa1/AAA/AAA/) $870.280 million of tax-exempt future tax-secured subordinate bonds.

The first tranche, $831.030 million of Fiscal 2023 Series B, Subseries B-1, saw 5s of 11/2023 at 2.27%, 5s of 2027 at 2.56% (+1), 5s of 2032 at 3.00%, 5.25s of 2037 at 3.55%, 5s of 2037 at 3.55% and 5s of 2038 at 3.60%, callable 11/1/2032.

The second tranche, $39.250 million of Fiscal 2023 Series C, Subseries C-1, saw 5s of 11/2022 at 2.20%, 4s of 2027 at 2.56% (+1) and 5s of 2027 at 2.56% (+1), noncall.

Wells Fargo Bank priced for Charlotte, North Carolina, (Aaa/AAA/AAA/) $477.055 million of water and sewer system revenue bonds.

The first tranche, $463.650 million of exempts, Series 2022A, saw 5s of 7/2023 at 2.22%, 5s of 2027 at 2.29%, 5s of 2032 at 2.60%, 5s of 2037 at 3.06%, 5s of 2042 at 3.76%, 5s of 2045 at 3.47% and 4s of 2052 at 4.10%, callable 7/1/2032.

The second tranche, $13.405 million of taxable, Series 2022B, saw all bonds price at par: 3.45s of 7/2023 and 3.55s of 2025, noncall.

Barclays Capital priced for the Pennsylvania Housing Finance Agency (Aa1/AA+//) $152.955 million of single-family mortgage revenue bonds. The first tranche, $129.685 million of non-AMT social bonds, Series 2022-140A, saw all bonds price at 4.3s of 10/2042 price at par, 4.45s of 2047 price at par and 5s of 2052 at 3.58%, callable 4/1/2032.

The second tranche, $23.270 million of taxable, Series 2022-140B, saw 5.156s of 10/2042 price at par, callable 4/1/2032.

In the competitive market, the Indiana Finance Authority (Aaa/AAA/AAA/) sold $250 million of green state revolving fund program bonds, Series 2022B, to Citigroup Global Markets, with 5s of 2/2028 at 2.30%, 5s of 2032 at 2.65%, 5s of 2037 at 3.13%, 5s of 2042 at 3.39% and 5s of 2047 at 3.50%, callable 2/1/2032.

For the time being, the market has found its comfort zone, said Kim Olsan, senior vice president of municipal bond trading at FHN Financial

“Municipal metrics such as bids wanteds totals, secondary float and expected supply are hovering at the upper ends of neutral but could begin to force a wider yield adjustment,” Olsan noted.

Bloomberg bid list totals have reached the $1 billion-plus per day area, with its secondary offer platform has risen into the $10 billion range,” she said.

Bond Buyer 30-day visible supply sits at $10.04 billion.

“Taken together the three figures indicate growing caution,” she said.

“While some of August redemption proceeds appears to be rolling into fixed reinvestments (muni money market fund balances have fallen below $100 billion), new-issue results point to a steady pace ahead of key FOMC and economic news releases,” she said.

Since the market’s selloff in the spring, 3s and 4s have been used by “buyers stratifying the curve and credit for optimum spread,” according to Olsan.

She noted Delaware yesterday sold transportation bonds with a five-year spread of +10/AAA MMD and the last five years of the loan were bought with sub-4% coupons spread +80 range to AAA spot levels.

She noted that AMT shows “continual widening,” where the “yield gap has grown from earlier 2022 issuance.”

Minneapolis, Minnesota, yesterday “priced NR/A+ non-AMT and AMT-subject airport bonds: the non-AMT spreads were comparably priced to AA GO new issues — a 7-year maturity +32/AAA MMD but the AMT series pointed to the growing penalty as the 7-year AMT spread was 67 basis points wider; the AMT 5s due 2047 were spread nearly 50 basis points wide to a similarly rated Hawaii Airport issue from January,” she said.

An upcoming pricing of a total of $1.6 billion Chicago O’Hare Airports, Illinois, “will offer nearly $1 billion in AMT-subject bonds due 2048-2055, with the potential for mid-4% yields or higher,” she said.

Informa: Money market muni assets rise

Tax-exempt municipal money market funds saw inflows continue as $2.43 billion was added the week ending Monday, bringing the total assets to $99.86 billion, according to the Money Fund Report, a publication of Informa Financial Intelligence.

The average seven-day simple yield for all tax-free and municipal money-market funds fell to 1.33%.

Taxable money-fund assets added $2.95 billion to end the reporting week at $4.412 trillion of total net assets. The average seven-day simple yield for all taxable reporting funds rose to 1.86%.

Secondary trading

Washington 5s of 2023 at 2.24%. NYC TFA 5s of 2023 at 2.30%-2.29%. Austin, Texas, 5s of 2024 at 2.26%-2.22%. North Carolina 5s of 2025 at 2.26%.

Maryland 5s of 2025 at 2.26% versus 1.71% on 8/5. California 5s of 2026 at 2.25%. Ohio 5s of 2027 at 2.32%.

Maryland 5s of 2034 at 2.77%.

California 5s of 2041 at 3.24% versus 3.15% Monday and 3.13% on Friday.

AAA scales

Refinitiv MMD’s scale was cut two to 10 basis points at a 3 p.m. read: the one-year at 2.19% (+2) and 2.21% (+3) in two years. The five-year at 2.26% (+4), the 10-year at 2.54% (+6) and the 30-year at 3.23% (+10).

The ICE AAA yield curve was cut two to five basis points: 2.20% (+2) in 2023 and 2.24% (+3) in 2024. The five-year at 2.28% (+3), the 10-year was at 2.60% (+5) and the 30-year yield was at 3.14% (+5) at a 4 p.m. read.

The IHS Markit municipal curve was also cut: 2.18% (+3) in 2023 and 2.21% (+3) in 2024. The five-year was at 2.24% (+3), the 10-year was at 2.52% (+3) and the 30-year yield was at 3.22% (+8) at a 3 p.m. read.

Bloomberg BVAL was cut three to eight basis points: 2.24% (+3) in 2023 and 2.24% (+4) in 2024. The five-year at 2.23% (+4), the 10-year at 2.53% (+5) and the 30-year at 3.24% (+8) at 4 p.m.

Treasuries were weaker.

The two-year UST was yielding 3.402% (+10), the three-year was at 3.405% (+6), the five-year at 3.241% (+7), the seven-year 3.203% (+7), the 10-year yielding 3.111% (+6), the 20-year at 3.556% (+6) and the 30-year Treasury was yielding 3.316% (+6) just before the close.

Primary to come:

The Alamo Community College District, Texas, (Aaa/AAA//) is set to price Thursday $244.170 million of maintenance tax notes, Series 2022, serials 2023-2030. Siebert Williams Shank & Co.

Richmond, Virginia, (/AA-//) is set to price Thursday $156.285 million of taxable pension refunding bonds, Series 2022, serials 2026-2037, term 2044. Loop Capital Markets.

The Dormitory Authority of the State of New York (Aa3//AA-/) is set to price Thursday $111.795 million of school district revenue bond financing program revenue bonds, Series 2022C, serials 2023-2041. RBC Capital Markets.