Municipals were mixed Thursday as inflows into muni mutual funds returned, while U.S. Treasuries were weaker, and equities ended down.

The three-year muni-UST ratio was at 53%, the five-year at 54%, the 10-year at 60% and the 30-year at 87%, according to Refinitiv MMD’s 3 p.m. ET read. ICE Data Services had the three at 54%, the five at 56%, the 10 at 61% and the 30 at 89% at 4 p.m.

The municipal yield curve “continues to be in flux with the ultra-short end undergoing a significant repricing while maturities past 2028 hold most of their value,” said Kim Olsan, senior vice president of municipal bond trading at FHN Financial.

“A 10% drop in municipal money market balances in the last month (holders reallocating into high-yielding T-bills or committing out the curve in tax-exempts?) has meant floating-rate debt is much less in demand,” she said.

Weekly-floater rates “rose nearly 200 basis points over the course of the week and have pushed generic 1- and 2-year AAA spots well higher vis-à-vis the balance of the curve,” she noted.

The 1-30 year MMD curve has compressed to 66 basis points, its flattest in the last five years, Olsan said.

Several wider-trading credits “have approached 3% bidsides in 2024/2025 maturities, a level which may eventually filter into higher-rated bonds if the Fed’s pronouncements come to fruition about the status of rates,” she said.

As a means to temper some of the richness in the intermediate range, she said “seasoned calls have drawn back some audience where concessions remain.”

A bids wanteds “for Washington GO 5s due 2031/callable 2025 traded at 2.64%, spread +49/MMD — well wide to where the state’s noncallable bonds would trade in 2031,” according to Olsan.

Opinions run wild as “to how long the Fed will hold rates at a higher range, creating ongoing interest for duration — bonds for everyone, essentially,” she said.

Syndicate results “drew a slightly softer tone — New York City’s Transitional Finance final pricing saw yields cut 4 basis points in select intermediate maturities (again, recognizing ultra-tight ratios),” she said.

The calendar ramps up next week, she said, “but is absent high-grade, general-market names.”

In light of reduced benchmark names, Olsan said, the consumer price index and producer price index releases “could influence broader interest rate action.”

“Average market consensus calls for interest rates to stabilize as we head into 2023,” said Goldman Sachs strategists Scott Diamond, Sylvia Yeh and Davis Alter.

“A great deal of variability exists with this forecasting as (1) there is debate around if and at what pace inflation returns to acceptable levels, (2) whether the U.S. enters a recession, and (3) how the Fed’s monetary policy will respond to economic data,” they said.

This tug-of-war between “views on inflation and economic data may be a persevering theme” throughout the upcoming year, they noted.

But unless inflation takes an unexpected turn upward, “the market believes we are closer to the end, rather than the beginning, of the Fed rate hiking cycle,” Goldman Sachs strategists said.

The fed funds rate is expected to peak at 5% in mid-2023, “with the market pricing in a possibility of rate cuts towards the end of the year,” they said.

Municipal mutual funds saw their largest ever annual outflows in 2022 ― more than $140 billion ― shattering the previous record set in 2013.

“Fear of rising interest rates were seen as the main reason for the outflows; however, tax loss harvesting may also have played a significant role,” they said.

Other municipal investment vehicles, including separately managed accounts exchange-traded funds, and individual bond buying, “generally saw positive momentum as yields peaked during the middle of the year and into the fall,” they noted.

The Goldman Sachs strategists believe “elevated tax-free yields, coupled with a steady interest rate backdrop, will drive strong demand across all municipal investment vehicles in 2023.”

Mutual funds, they said, “may benefit disproportionately, given the level of withdrawals encountered and their asset base relative to the size of the overall municipal market.”

“Demand from non-traditional buyers of municipal debt, such as banks, insurance companies, and foreign investors, will continue to be driven by relative valuations versus other fixed-income asset classes,” they said.

They believe “the combination of a stable interest rate environment, elevated absolute tax-free yields, muted new issue supply, increased demand, and continued strong credit fundamentals will lead municipals to outperform in 2023.”

Expected outperformance should lead to munis trading at the tighter end of historical valuations.

Muni-UST ratios, they said, should “be on the lower end versus recent history given the supportive technical backdrop.”

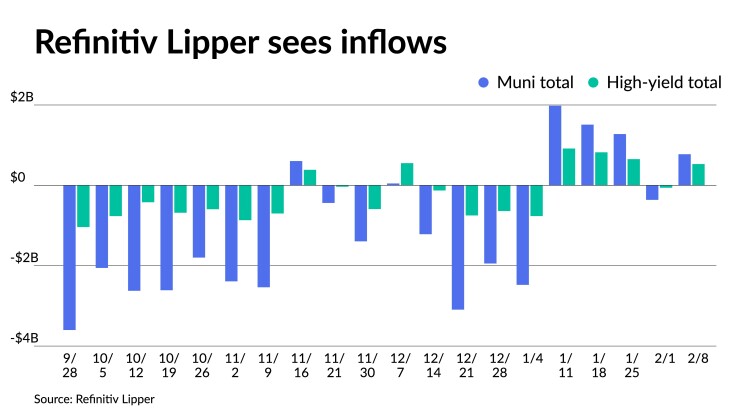

Inflows returned as Lipper reported $775.006 million was added to municipal bond mutual funds in the week ended Wednesday after $361.649 million of outflows the week prior.

High-yield saw $530.316 million of inflows after $59.788 million of outflows the week prior, while ETFs saw outflows of $474.684 million after $713.581 million of outflows the previous week.

In the primary, BofA Securities priced for the Delaware Valley Regional Finance Authority (A1/A+//) $141.030 million of local government revenue bonds, 2023 Series A, with 4s of 3/2033 at 3.01%, callable 9/1/2032, and 4s of 2035 at 3.39%, callable 9/1/2034.

Secondary trading

LA USD 5s of 2024 at 2.50% versus 2.31%-2.30% Tuesday. Boston 5s of 2025 at 2.32% versus 2.36% Wednesday. NYC TFA 5s of 2025 at 2.51%.

Seattle 5s of 2028 at 2.19%-2.16%. Massachusetts 5s of 2029 at 2.15%. Georgia 5s of 2030 at 2.12% versus 2.12% on 1/26 and 2.12% on 1/25.

Montgomery County, Maryland, 5s of 2036 at 2.71%-2.68% versus 2.70%-2.66% on 1/25. LA DWP 5s of 2037 at 2.70%-2.66%. California 5s of 2037 at 2.76% versus 2.76% on 1/23 and 2.73% on 1/20.

DC 5s of 2047 at 3.47%-3.46%. Fort Lauderdale, Florida, 5s of 2029 at 3.32%-3.40% versus 3.55% on 2/1. San Jose Financing Authority, California, 5s of 2052 at 3.33% versus 3.30%-3.31% on 1/27 and 3.30%-3.29% on 1/24.

AAA scales

Refinitiv MMD’s scale was bumped up to two basis points. The one-year was at 2.58% (unch) and 2.35% (unch) in two years. The five-year was at 2.09% (unch), the 10-year at 2.21% (-2) and the 30-year at 3.24% (unch) at 3 p.m.

The ICE AAA yield curve was mixed: 2.64% (+2) in 2024 and 2.41% (+2) in 2025. The five-year was at 2.34% (-1), the 10-year was at 2.20% (-1) and the 30-year yield was at 3.28% (-1) at 4 p.m.

The IHS Markit municipal curve was unchanged: 2.58% in 2024 and 2.33% in 2025. The five-year was at 2.09%, the 10-year was at 2.24% and the 30-year yield was at 3.24% at a 4 p.m. read.

Bloomberg BVAL was cut up to four basis points: 2.62% (+4) in 2024 and 2.33% (+2) in 2025. The five-year at 2.14% (+1), the 10-year at 2.27% (+1) and the 30-year at 3.29% (+1).

Treasuries were weaker.

The two-year UST was yielding 4.497% (+6), the three-year was at 4.164% (+7), the five-year at 3.869% (+6), the seven-year at 3.792% (+6), the 10-year at 3.674% (+4), the 20-year at 3.893% (+5) and the 30-year Treasury was yielding 3.740% (+5) at 4 p.m.

Mutual fund details

Refinitiv Lipper reported $775.006 million of municipal bond mutual fund inflows for the week that ended Wednesday following $361.649 million of outflows the previous week.

Exchange-traded muni funds reported outflows of $474.684 million after outflows of $713.581 million in the previous week. Ex-ETFs, muni funds saw inflows of $1.250 billion after inflows of $351.932 million in the prior week.

Long-term muni bond funds had inflows of $1.018 billion in the latest week after inflows of $231.352 million in the previous week. Intermediate-term funds had inflows of $233.018 million after outflows of $24.783 million in the prior week.

National funds had inflows of $556.638 million after outflows of $52.125 million the previous week while high-yield muni funds reported inflows of $530.316 million after outflows of $59.788 million the week prior.