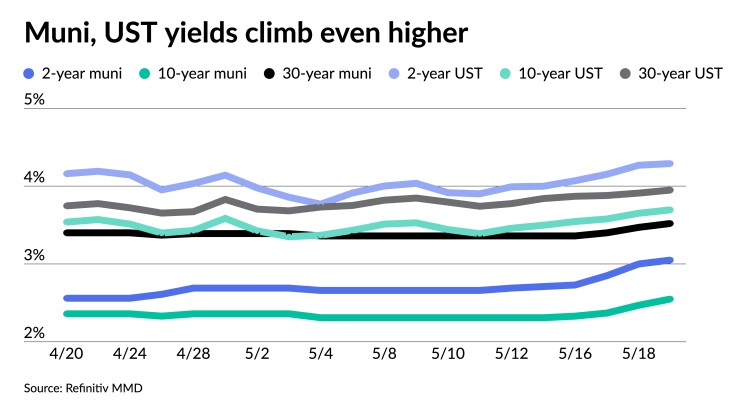

Muni yields climbed even higher to end the week, while U.S. Treasuries were weaker and equities ended down.

Muni yields, after outperforming USTs the prior week, “have adjusted higher in a hurry this week in sympathy with the UST selloff,” said Barclays strategists Mikhail Foux, Clare Pickering and Mayur Patel.

Triple-A benchmark yields rose four to 11 basis points, depending on the scale, while UST yields rose three to six basis points on Friday. For the week, triple-A muni yields rose between 11 and 29 basis points, according to MMD, while UST yields rose 11 to 32 basis points.

The Barclays strategists noted municipal to UST ratios have remained pretty much unchanged.

Municipal to UST ratios were steady. The two-year muni-Treasury ratio Friday was at 71%, the three-year at 72%, the five-year at 70%, the 10-year at 69% and the 30-year at 89%, according to Refinitiv MMD’s 3 p.m. ET read. ICE Data Services had the two-year at 72%, the three-year at 74%, the five-year at 71%, the 10-year at 71% and the 30-year at 91% at 4 p.m.

In general, they said, the muni market “has been notably stable versus U.S. Treasuries in 2023 in a drastic contrast with last year.” For example, the 30-year municipal to UST ratio “spent this year in the 88%-94% range, while ratios were quite volatile in 2022, trading the bulk of time above 97%,” they said.

Triple-A benchmark yields this week rose a “few basis points as Treasury yields trade around the very upper bounds of their ranges of the past two months,” BofA strategists said in a weekly report.

They attributed the “Treasury market weakness in short maturities … to waning hope of an early Fed rate cut, while the weakness in longer maturities was due to the hope of finding a resolution to the debt limit issue in time.”

However, they noted there are still two weeks before the June 1 X-date.

“More news on the negotiating parties’ posturing may cause day-to-day today volatility for the rest of the month,” they said.

The Barclays strategists said USTs will play a large role in what happens going forward.

“If there is a debt ceiling deal, muni yields might adjust higher but they should outperform Treasuries, in our view, mainly due to summer redemptions, while we are positive on the market,” according to the Barclays strategists.

While redemptions are still sizable, they are smaller than they have been in previous years, they noted.

Market volatility and uncertainty over the debt ceiling has left many of issuers on the sidelines, the Barclays strategists said.

“Muni investors have sizable cash balances, and should find attractive opportunities if the market underperforms,” they said.

The Barclays strategists are “less sanguine about the taxable market, as spreads remained tight despite continued pressure on corporate spreads.”

Currently, they said, “the spread differential between the taxable muni and the corporate indices is close to the widest for the year.”

While spreads of some of the benchmark names “have adjusted up slightly, the taxable index has not responded in any meaningful way as of yet,” they said.

The Barclays strategists noted this segment of the muni market continues to do well because of the lack of supply.

“Some institutional investors, mainly banks, have been focused on shortening duration and trimming their taxable muni exposure, but this shadow supply has been easily absorbed by investors,” they said.

They believe “market valuations are too rich at the moment and would not recommend adding exposure to this market segment unless taxable spreads adjust wider.”

The BofA strategists said, historically, muni yields “tend to move somewhat lower heading into the Memorial Day holiday, and for a period thereafter.”

“With the Fed’s somewhat-hawkish tone despite uncertainty surrounding the debt limit negotiation,” they said, it’s unclear if this will happen this year.

Calendar stands at $5.8B

For the coming week, investors will be greeted with a new-issue calendar estimated at $5.837 billion.

There are $4.692 billion of negotiated deals on tap and $1.143 billion on the competitive calendar.

The negotiated calendar is led by $937 million of revenue bonds from the New Jersey Transportation Trust Fund Authority in two deals, followed by $590 of electric and gas system revenue refunding bonds from San Antonio, Texas, and $485 million of water system revenue bonds from the Department of Water and Power of the city of Los Angeles.

Forsyth County, North Carolina, leads the competitive calendar with $128 million of GOs in two deals, followed by Madison Metro School District, Wisconsin, with $105 million of GOs.

Secondary trading

Connecticut 5s of 2024 at 3.65% versus 3.11% on 5/10. Washington 5s of 2024 at 3.35% versus 3.00% on 5/11 and 2.97% on 5/5. North Carolina 5s of 2025 at 3.08%.

DASNY 5s of 2028 at 2.94%. NYC 5s of 2028 at 2.77% versus 2.47% on 5/9. Prince George’s County, Maryland, 5s of 2029 at 2.74%.

Loudoun County, Virginia, 5s of 2033 at 2.74%-2.73% versus 2.37% original on Wednesday. St. Johns County water, Florida, 5s of 2035 at 2.82%-2.81% versus 2.77%-2.72% on 5/2.

Union County, North Carolina, 5s of 2043 at 3.35% versus 3.16%-2.95% Thursday and 3.19% Wednesday. Baltimore County, Maryland, 5s of 2047 at 3.58%.

AAA scales

Refinitiv MMD’s scale was cut five to eight basis points: The one-year was at 3.26% (+5) and 3.05% (+5) in two years. The five-year was at 2.65% (+8), the 10-year at 2.55% (+8) and the 30-year at 3.52% (+5) at 3 p.m.

The ICE AAA yield curve was cut five to 11 basis points: 3.32% (+5) in 2024 and 3.07% (+8) in 2025. The five-year was at 2.67% (+11), the 10-year was at 2.57% (+10) and the 30-year was at 3.54% (+7) at 4 p.m.

The IHS Markit municipal curve was cut five to eight basis points: 3.25% (+5) in 2024 and 3.05% (+5) in 2025. The five-year was at 2.65% (+8), the 10-year was at 2.54% (+8) and the 30-year yield was at 3.52% (+5), according to a 4 p.m. read.

Bloomberg BVAL was cut four to seven basis points: 3.08% (+4) in 2024 and 2.96% (+5) in 2025. The five-year at 2.60% (+6), the 10-year at 2.52% (+6) and the 30-year at 3.56% (+5) at 4 p.m.

Treasuries were weaker.

The two-year UST was yielding 4.300% (+3), the three-year was at 3.980% (+5), the five-year at 3.756% (+6), the 10-year at 3.697% (+5), the 20-year at 4.079% (+4) and the 30-year Treasury was yielding 3.948% (+4) at 4 p.m.

Primary to come:

The New Jersey Transportation Trust Fund Authority (A2/A-/A/A/) will price $674 million of Series AA transportation program bonds on Thursday. Jefferies.

The authority (A2/A-/A/) is also set to price $262.780 million of Series A transportation system bonds on Thursday. Jefferies.

San Antonio, Texas, (Aa2/AA-/AA-/) is set to price $589.995 million of electric and gas systems revenue and revenue refunding bonds on Tuesday. Serials 2024 to 2044; term in 2050. Loop Capital Markets.

The Department of Water and Power of the city of Los Angeles (Aa2/AA+/AA/) is set to price $485.475 million of 2023 Series A water system revenue refunding bonds on Tuesday. Serials 2023 to 2044; terms 2049 and 2053. Wells Fargo Bank.

The Metropolitan Washington Airports Authority (Aa3/AA-/AA-/) is set to price $433.115 million of Series 2023 A airport system revenue and refunding bonds subject to the AMT on Wednesday. Barclays Capital.

The Pennsylvania Housing Finance Agency (Aa1/AA+//) is set to price $387.270 million of Series 2023 -142A, non-AMT single-family mortgage revenue social bonds on Wednesday. Serials 2028 to 2034; terms in 2038, 2041, 2043, 2046, 2048, 2050, 2053. Jefferies.

The Oregon Department of Transportation (Aa2/AA+/AA+/) is set to price $210.640 million of Series 2023 A highway user tax revenue subordinate lien bonds on Wednesday. Serials 2035 to 2042. Wells Fargo Bank.

The Fremont, California, Union High School District (Aaa/AAA//) is set to price $210 million of Series 2023 general obligation bonds on Tuesday. Morgan Stanley.

Pflugerville, Texas, (Aa1///AA+) is slated to price $153 million of combination tax and limited revenue certificates of obligation Series 2023 bonds on Tuesday. Serials 2024 to 2043; terms 2048 and 2053. Sibert Williams Shank.

Fort Bend County, Texas, (Aa1//AA+/) is set to price $134.090 million of Series 2023 A, B, and C bonds on Tuesday. J.P. Morgan Securities.

The Iowa Finance Authority (Aaa/AAA//) is set to price $130.750 million of 2023 Series C non-AMT and Series D taxable single-family mortgage-backed bonds on Tuesday. Morgan Stanley.

Georgetown, Texas, (/AA//) is set to price $101.400 million of Series 2023 utility system revenue bonds insured by Build America Mutual Assurance Co. on Wednesday. Serials 2024 to 2043; terms 2048, 2053. Bok Financial Securities.

San Antonio, Texas, (Aa3/A-plus/AA-minus/) is set to price $100.300 million of electric and gas systems variable rate junior-lien Series 2023 revenue refunding bonds on Wednesday. Term in 2053. Barclays Capital.

Brazoria County, Texas, Industrial Development Corp. is set to price $100 million of solid waste disposal facilities revenue bonds for the Aleon Renewable Metals LLC Project on Wednesday. Truist Securities.

Competitive:

The Madison, Wisconsin, Metropolitan School District is set to sell $105 million of GO debt on Monday.

Forsythe, North Carolina, (Aaa/AAA/AAA/) is set to sell $127.7 million of GO paper on Tuesday in two deals.

Christine Albano contributed to this story.