Municipals rallied Friday across the curve sending triple-A yields lower by as much as 13 basis points as they continued to play catch up to the moves in U.S. Treasuries, which also saw more gains after a weaker jobs report further signaled Fed rate hikes may be done. Equities closed the week in the black.

“Today’s softer than expected payroll print, specifically the combination of the rising unemployment rate and a downward revision of last month’s hot figure, should validate the view that the hiking cycle is over,” said Alexandra Wilson-Elizondo, deputy chief investment officer of multi-asset solutions at Goldman Sachs Asset Management.

“We believe the recession is delayed for now as fiscal policy continues to do the heavy lifting,” she said. The likelihood of a soft landing rose.

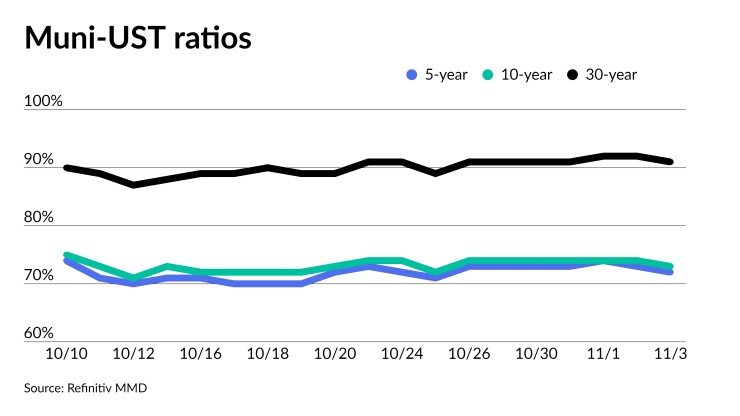

Ratios fell slightly Friday with the two-year muni-to-Treasury ratio at 70%, the three-year was at 71%, the five-year at 72%, the 10-year at 73% and the 30-year at 91%, according to Refinitiv Municipal Market Data’s 3 p.m., ET, read. ICE Data Services had the two-year at 70%, the three-year at 71%, the five-year at 69%, the 10-year at 71% and the 30-year at 89% at 4 p.m.

After the Treasury market rallied hard on Wednesday, the positive movement continued into the end of the week, “which should carry on for a while,” BofA Global Research strategists said in a weekly report.

Munis barely followed on Wednesday, but “then followed with more rigor on Thursday,” they noted. Municipals continued with force on Friday.

This is likely to continue, they said, especially if the current UST rally develops into a tradeable bullish trend.

After this week’s market performance,” it feels once again that a long-awaited muni turnaround might have occurred in late October, early November, exactly the same time as last year,” Barclays PLC said in a weekly report.

In previous years, munis “also did well in November-December, which has already provided a market-supportive backdrop,” Barclays strategists Mikhail Foux, Clare Pickering and Mayur Patel noted.

For November, BofA strategists expect $34 billion of issuance and redemptions of $40.7 billion, $27.5 billion principal redemption and $13.2 billion of coupon payments.

“Muni supply/demand is not an issue at all; the only missing item was a tradeable Treasury rally,” they said. “Now that a Treasury trend appears underway, we should have a decent muni market rally in the coming weeks.”

Bond Buyer 30-day visible supply sits at $12.96 billion.

Looking ahead, Barclays strategists remain positive on munis this week’s strong performance, “and see more upside for the asset class in 2023.”

“Supply might pick up briefly, but we are not overly concerned and feel that it would be absorbed without any problems,” they said.

“Dealers are not heavy at the moment, although mutual funds are a bit low on cash, we believe that outflows should start abating, which should help demand from this group of investors,” Barclays strategists said.

Overall, they noted “high-grade tax-exempts are attractive, as their tax-adjusted yield pickups over Treasuries and high-grade corporates are substantially wider than in recent history.”

The primary calendar ticks up next week with potential volume estimated at $8.310 billion.

There are $6.053 billion of municipal bond sales scheduled for negotiated sale next week and $2.256 billion of competitive deals on tap, per Bond Buyer and Ipreo data.

AAA scales

Refinitiv MMD’s scale was bumped 12 basis points from top to bottom: The one-year was at 3.52% (-12) and 3.41% (-12) in two years. The five-year was at 3.25% (-12), the 10-year at 3.32% (-12) and the 30-year at 4.33% (-12) at 3 p.m.

The ICE AAA yield curve was bumped 10 to 13 basis points: 3.53% (-10) in 2024 and 3.59% (-11) in 2025. The five-year was at 3.24% (-13), the 10-year was at 3.30% (-13) and the 30-year was at 4.30% (-11) at 4 p.m.

The S&P Global Market Intelligence municipal curve was bumped 12 to 13 basis points: The one-year was at 3.54% (-13) in 2024 and 3.44% (-13) in 2025. The five-year was at 3.29% (-13), the 10-year was at 3.33% (-13) and the 30-year yield was at 4.33% (-13), according to a 3 p.m. read.

Bloomberg BVAL was cut bumped 11 to 12 basis points: 3.58% (-11) in 2024 and 3.51% (-11) in 2025. The five-year at 3.29% (-11), the 10-year at 3.37% (-10) and the 30-year at 4.38% (-12) at 3:30 p.m.

Treasuries rallied.

The two-year UST was yielding 4.834% (-14), the three-year was at 4.633% (-14), the five-year at 4.498% (-14), the 10-year at 4.57% (-10), the 20-year at 4.945% (-6) and the 30-year Treasury was yielding 4.% 766 (-5) at the close.

Employment report

Friday’s employment report was good news for the Federal Reserve, with fewer jobs created and a smaller rise in earnings, leading analysts to cautiously increase expectations that the hiking cycle is over.

“This is a very Fed-friendly report,” said Sal Guatieri, BMO senior economist, pointing to slower job growth, a growing unemployment rate, and cooling wages. “The only wrinkle is that the labor force shrank, as Chair Powell is counting on rising participation and population growth to increase the labor supply faster than demand to support a further easing in inflation pressures.”

The numbers, including a 101,000 downward revision to the two previous months, he said, “will go a long way to keeping the Fed on the sidelines for a third straight meeting in December.”

Payrolls grew by 150,000 in October, while the September gain was lowered to 297,000.

“The headline figure was padded, yet again, by a hefty increase in government hiring (51,000) that brought the total back to pre-pandemic levels,” Guatieri said. The strike by UAW workers lowered manufacturing employment by 35,000, he noted, but the “tentative deal with the Big Three suggests a rebound in the November report.”

The unemployment rate edged up to 3.9% from 3.8% a month earlier, bringing it “one-half-percentage point above the cycle (and half-century) low,” he said.

Average hourly earnings rose 0.2% in the month and 4.1% on an annual basis. “The three-month annualized rate of 3.2% is the lowest since March 2021,” Guatieri said.

“While seemingly counterintuitive, weak job data is sparking a risk-on mentality,” said Bryce Doty, senior vice president and senior portfolio manager at Sit Investment Associates. “Today’s jobs data cements the much-needed relief from Fed rate increases. Credit spreads should continue to ratchet in and bond yields will come down as investors see it as now safe to pile into bonds.”

The report gave the Fed the “more tempered economic data” it sought, said Morning Consult senior economist Jesse Wheeler. “I think this report will be received well by markets that were already riding high this week after Chair Powell’s remarks convinced many that the rate hiking cycle may have come to an end.“

The was uncertainty whether “the correlated rally post Fed and refunding announcement will stick or if markets will revert to rejecting the current policy mix of loose fiscal and tight monetary,” Wilson-Elizondo said. “We maintain the view to push against the ‘glass half empty’ response to earnings season as sentiment, Fed calls, and year-end seasonals should provide support to the market. That said, we have preferred relative value views over directional, favoring the broad index over high capex and leverage sectors like REITS and utilities. We also believe that rates offer portfolio construction value as we continue to expect the unexpected going into 2024.”

“It looks like the recovery we had seen since late last year is now starting to level off — the participation rate and the labor force both declined slightly in October,” said Fitch Ratings Chief Economist Brian Coulton.

The data “still suggests robust expansion in labor demand and that was confirmed by the JOLTS data showing another rise in job openings in September,” he added. Although growth in wages “eased” in October, “the Fed will be concerned that labor market conditions remain tight, maintaining upward pressure on wages.”

While the Fed “could not realistically have hoped for a better jobs report,” it will take “a number of positive economic reports over the coming months” before the Fed can “declare victory,” according to Craig Erlam, senior market analyst UK & EMEA at OANDA.

The Fed hopes this report is “a sign of things to come rather than a blip in the data,” he said. “We have been seeing the labor market cooling slightly but just not nearly enough until now and this could be a sign of that accelerating.”

Still, ING Chief International Economist James Knightley noted, “Labor market numbers are always the last thing to turn in an economic cycle so the softening in employment and wage growth and the rise in the unemployment rate makes it all the more likely that the Federal Reserve won’t hike interest rates again.”

Gary Siegel contributed to this report.