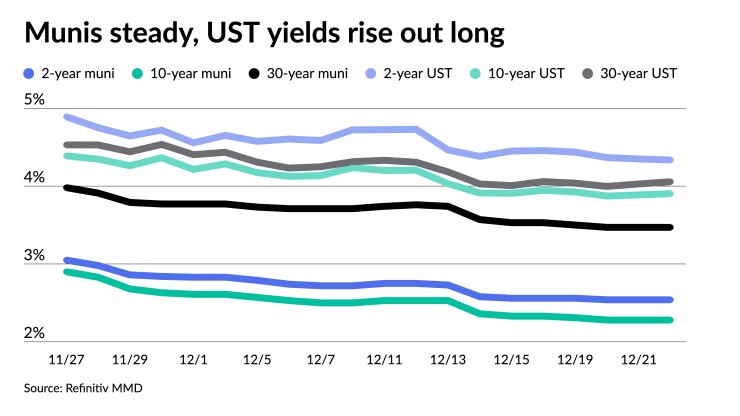

Municipals were steady to close Friday ahead of a week without new deals on the calendar. U.S. Treasuries were weaker out long and equities ended the session up.

The two-year muni-to-Treasury ratio Friday was at 58%, the three-year at 59%, the five-year at 59%, the 10-year at 58% and the 30-year at 85%, according to Refinitiv Municipal Market Data’s 1 p.m. EST read. ICE Data Services had the two-year at 59%, the three-year at 58%, the five-year at 58%, the 10-year at 60% and the 30-year at 86% at 1 p.m.

The year is ending on a strong note, said Joshua Perry, a partner, portfolio manager and municipal credit analyst at Brown Advisory.

The UST curve appears to be ending 2023 on a “point-to-point basis” from last year, he said.

The front end of the UST curve is lower than last year, but five years and out, “the rest of the curve is pretty much right on top of where it was.”

The two-year UST is at 4.333% Friday versus 4.429% on Dec. 30, 2022. The 10-year UST and 30-year UST are at 3.903% and 4.056%, respectively, compared to 3.882% and 3.968% at the end of last year.

For munis, yields are significantly lower in 2023 than last year, with as much as a 37-basis point difference, according to Refinitiv MMD.

Refinitiv MMD has the two-year at 2.54%, the five-year at 2.28%, the 10-year at 2.28% and the 30-year at 3.47% on Friday, versus the two-year at 2.60%, the five-year at 2.52%, the 10-year at 2.63% and the 30-year at 3.58% on Dec. 30, 2022.

This year has seen much volatility, Perry said.

“The volatility picked up and then had that huge scare in October, and then had crazy turnaround in November,” he said.

It’s unclear how this will play out in 2024, but Perry does not expect the volatility to subside until there is more clarity on exogenous factors, such as when the Fed

“There’s a big contingent of people that are uncertain about what that means,” he said.

This includes when the Fed cuts rates, by how much and the frequency of rate cuts, according to Perry.

“All of that is going to continue to play into some of that volatility,” he said.

But once market participants have a better understanding of the Fed’s path, volatility “probably will come down” during the second half of the year.

There continues to be a supply-demand imbalance in the market, he said.

Many issuers still have pandemic funds and have not necessarily exhausted all of those yet, he said.

“And, in a rising rate environment, it makes sense that they wouldn’t want to come back to market when they could have the cash to do that,” he said.

For a while in 2023, Perry said, it seemed that the only issuers that were coming to market were the ones that absolutely had to.

With the rally in November and December, issuers have been better able to consider if the environment was right for them.

“Do the issuers feel like it is the right time, the right structure, the right environment for them to issue based on what their needs are,” he said.

New-issue volume for 2023 is low compared to historical averages, sitting at $375.5 billion as of Wednesday. With no deals slated for next week, issuance for 2023 will not top the $390.7 billion seen in 2022.

If yearly issuance were to continue to fall “the municipal market as a whole will shrink pretty rapidly,” he said, noting there can only be a certain number of years of low supply before the entire market starts to contract.

However, most market participants believe

Perry believes issuance will rise next year because, if for nothing else, “the market is the size that it is and I don’t see any reason why the market should fundamentally be smaller than it is today.”

Secondary trading

Washington 5s of 2024 at 2.86% versus 2.91% original on Thursday. Ohio 5s of 2024 at 3.02%. Georgia 5s of 2025 at 2.75%-2.66%.

Indiana Finance Authority 5s of 2027 at 2.41% versus 2.45%-2.47% Thursday and 2.43% Tuesday. California 5s of 2028 at 2.26% versus 2.53% on 12/12. Washington 5s of 2029 at 2.32% versus 2.36%-2.34% Tuesday.

NYC Municipal Water Finance Authority 5s of 2031 at 2.25%-2.24%. DASNY 5s of 2032 at 2.35% versus 2.40%-2.34% Thursday and 2.43%-2.48% on 12/14. Boston 5s of 2037 at 2.67%.

Garland ISD, Texas, 5s of 2048 at 3.58% versus 2.57%-3.56% Thursday and 3.56% Wednesday. Massachusetts Transportation Fund 5s of 2053 at 3.70%.

AAA scales

Refinitiv MMD’s scale was unchanged: The one-year was at 2.69% and 2.54% in two years. The five-year was at 2.28%, the 10-year at 2.28% and the 30-year at 3.47% at 1 p.m.

The ICE AAA yield curve was little changed: 2.74% (unch) in 2024 and 2.55% (unch) in 2025. The five-year was at 2.27% (unch), the 10-year was at 2.31% (unch) and the 30-year was at 3.46% (unch) at 1 p.m.

Bloomberg BVAL was little changed: 2.58% (unch) in 2024 and 2.49% (unch) in 2025. The five-year at 2.20% (-1), the 10-year at 2.27% (unch) and the 30-year at 3.36% (unch) at 1 p.m.

Treasuries were slightly weaker out long.

The two-year UST was yielding 4.333% (-1), the three-year was at 4.046% (-1), the five-year at 3.882% (flat), the 10-year at 3.903% (+2), the 20-year at 4.217% (+2) and the 30-year Treasury was yielding 4.056% (+3) at 1 p.m.