Municipals sold off Thursday with more cuts across the curve as a correction has ensued for the asset class just ahead of the summer reinvestment season. U.S. Treasuries saw losses and equities were also in the red.

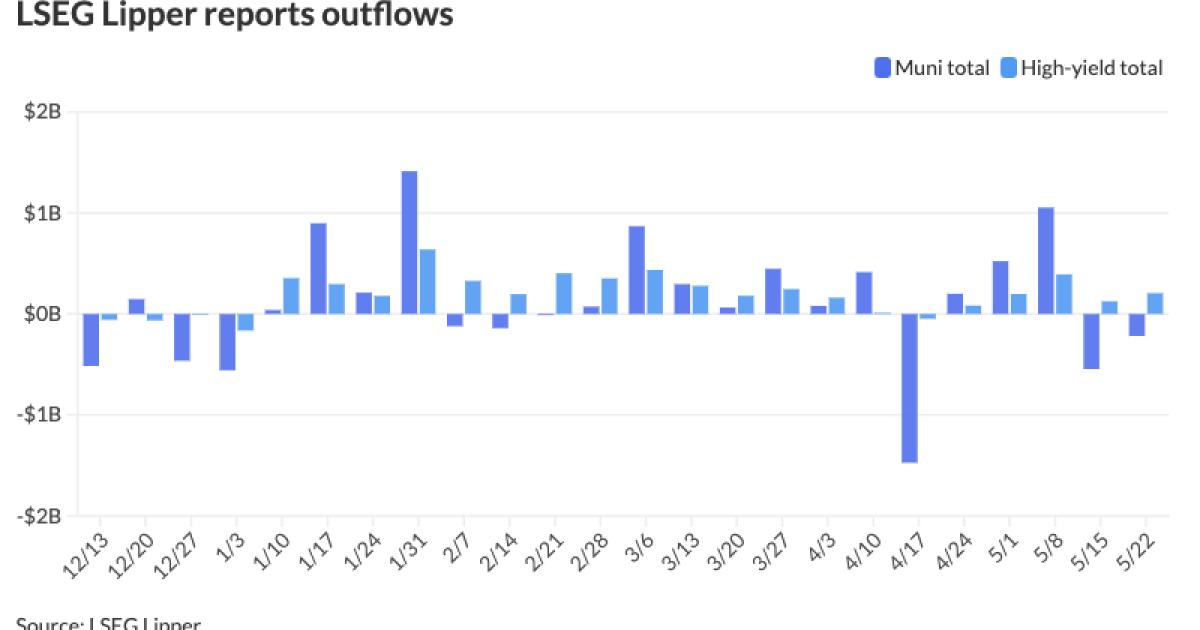

Municipal bond mutual funds saw the second week of outflows as investors pulled $217.6 million from the funds after $546.2 million of outflows the week prior, according to LSEG Lipper.

High-yield continued to show strength, though, with inflows of $206.5 million after $125.7 million of inflows the previous week.

The market correction may have finally begun, as triple-A yields have risen as much 13 to 17 basis points on the front end and belly of the curve since Monday, noted Barclays strategists Mikhail Foux and Clare Pickering.

Due to this, muni-UST ratios have risen more than 5 percentage points on 10 years and in with a smaller rise longer out the curve, climbing to highs last seen in late 2023, they said.

The two-year muni-to-Treasury ratio Thursday was at 67%, the three-year at 67%, the five-year at 67%, the 10-year at 67% and the 30-year at 84%, according to Refinitiv Municipal Market Data’s 3 p.m. EST read. ICE Data Services had the two-year at 67%, the three-year at 67%, the five-year at 68%, the 10-year at 68% and the 30-year at 85% at 3:30 p.m.

Supply is the primary reason behind the selloff, “hardly a surprise as we had around seven $10-plus billion supply weeks in a row,” Barclays strategists said.

Meanwhile, they noted fund inflows are “anemic” and unless valuations become more attractive, institutional investors are “staying on the sidelines and seem unlikely to buy munis.”

Supply falls to $2.337 billion next week — $1.5558 billion in the negotiated market and $778.7 million in the competitive market — due to the Memorial Day holiday, potentially helping the muni market recover somewhat, they said.

“But we do not think that buyers will re-emerge in droves, hence we expect rather subdued activity, and see a challenging trading environment subsequently” due to various factors, Barclays strategists noted.

For one, they expect issuance to be heavy throughout the summer into early fall as issuers opt to come to market ahead of the November elections, they said.

Additionally, in recent history June is “rarely kind to tax-exempt investors” outside of a few exceptions, with the 10-year muni-UST ratios widening an average of two percentage points and the 30-year muni-UST ratio widening an average of four basis points since 2018, they said.

Muni mutual fund flows remain “anemic,” and summer redemptions will be lower than in recent years, Barclays strategists said.

“Dealers seemed to be quite heavy going into this week’s correction, and likely got even longer as other municipal buyers largely remained cautious,” Barclays strategists said.

A primary driver of demand over the past year and a half has been separately managed accounts, they said.

“This week’s market selloff has been especially notable in the 5-10 year part of the curve where these investors are particularly active, which implies that even this investor group is stepping back,” they said.

The muni selloff may continue, “albeit punctuated by pauses,” Barclays strateigsts said.

“Even after this week’s correction, muni ratios are still quite rich compared with historical levels,” they said. “Hence, we would not be in a hurry to re-enter, as we think there will be better entry points down the line — if 10-year ratios fall into the low 70s, we could see more buyers reemerging; and after this week’s outperformance, the long end is probably more vulnerable at the moment.”

In the primary market Thursday, Ramirez priced for Corpus Christi, Texas, (/AA-/AA-/) $244.765 million of utility system senior lien revenue improvement and refunding bonds, Series 2024, with 5s of 7/2025 at 3.50%, 5s of 2029 at 3.32%, 5s of 2034 at 3.37%, 5s of 2039 at 3.65%, 5s of 2044 at 3.99%, 5s of 2049 at 4.20% and 4.25s of 2054 at 4.53%.

AAA scales

Refinitiv MMD’s scale was cut three to ninebasis points: The one-year was at 3.36% (+5) and 3.30% (+5) in two years. The five-year was at 3.03% (+9), the 10-year at 3.01% (+9) and the 30-year at 3.87% (+3) at 3 p.m.

The ICE AAA yield curve was cut three to eight basis points: 3.33% (+3) in 2025 and 3.28% (+5) in 2026. The five-year was at 3.03% (+8), the 10-year was at 3.00% (+8) and the 30-year was at 3.85% (+4) at 3:30 p.m.

The S&P Global Market Intelligence municipal curve was cut two to seven basis points: The one-year was at 3.38% (+8) in 2025 and 3.28% (+8) in 2026. The five-year was at 3.01% (+7), the 10-year was at 2.97% (+8) and the 30-year yield was at 3.85% (+3), according to a 3 p.m. read.

Bloomberg BVAL was cut up to 11 basis points: 3.38% (+4) in 2025 and 3.26% (+4) in 2026. The five-year at 2.99% (+10), the 10-year at 2.98% (+10) and the 30-year at 3.82% (unch) at 3:30 p.m.

Treasuries were weaker throughout most of the curve.

The two-year UST was yielding 4.931% (+5), the three-year was at 4.710% (+5), the five-year at 4.524% (+5), the 10-year at 4.473% (+4), the 20-year at 4.676% (+3) and the 30-year at 4.478% (+3) at 3:30 p.m.

FOMC minutes

Although there were surprises in the minutes from the latest Federal Open Market Committee meeting, they did not move the markets much, analysts said.

Treasury bond yields continued drifting higher and stocks’ mild selloff persisted, noted Scott Anderson, chief U.S. economist and managing director at BMO Economics.

But Chris Low, chief economist at FHN Financial, called it surprising that many Fed officials questioned “whether the neutral rate has increased and some … ‘mentioned a willingness to tighten policy further should risks to inflation materialize in a way that such action became appropriate.'”

In his press conference after the meeting, Fed Chair Jerome Powell ruled out a rate hike. “But the minutes are a reminder that while the Fed does not see another rate hike as likely — and certainly does not see it as a base-case — it will not rule out hikes if inflation does not behave,” Low said.

Still, he said, “despite a lot of nuance … the accepted characterization of the press conference — that it was a dovish shift from recent communication — was not accurate. The tone of FOMC remarks since the meeting has been, if anything, a shade more hawkish than the tone before, and the minutes reveal no change of heart during the meeting.”

While the Fed hopes inflation will decelerate and allow rate cuts, “the FOMC will not make policy on the basis of hope alone,” Low said. “The Fed must see actual inflation progress.”

Ipek Ozkardeskaya, senior analyst at Swissquote Bank also commented about Powell’s answer to the rate hike question, which she said, “brought joy to investors.”

Her take is Powell “was referring to a hawkish discussion among Fed members during a meeting where many questioned whether the ‘high-for-longer’ rhetoric was restrictive enough to tame inflation, and if hiking rates might be a better idea.”

Sill, the latest consumer price index report, which showed slower inflation in April allayed hike concerns, Ozkardeskaya said.

Anderson said the minutes “showed a general lack of confidence around the inflation outlook and much uncertainty around the timing of potential rate cuts.”

Some participants, he noted, “suggested that the disinflation process would likely take longer than previously thought.”

Gary Siegel contributed to this story.