Municipals were slightly firmer in secondary trading while new-issues were repriced to lower yields from initial pricing wires. U.S. Treasuries were stronger and equities sold off ahead of the FOMC meeting Wednesday.

The current market technicals combined with a slowdown in issuance is creating a general malaise in the municipal market, according to a New York trader.

“The market is pretty quiet as it has been the last few weeks; there is really not a lot of supply to impact the market,” he said Tuesday. “Between low rates and the tight percentages it’s not like anyone is geared up and excited to jump and buy with both feet. The combination continues to put us in position with not enough bonds and a lot of money.”

Cash continues to build in investors’ accounts due to recent calls and redemption proceeds.

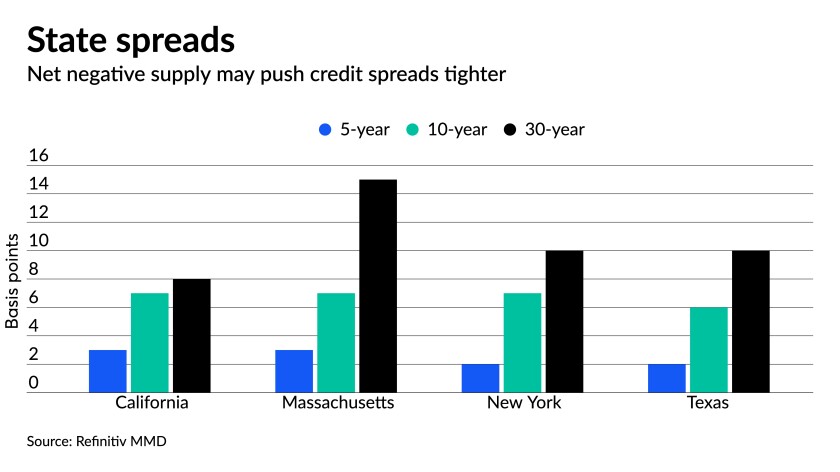

Net negative supply stands at $25.499 billion, according to Bloomberg data. The imbalance between supply and demand is most notable among large state issuers.

Texas leads with a whopping $9.8 billion net negative supply figure with California at negative $6.5 billion, New York at $3.52 billion, Massachusetts at negative $1.23 billion and Washington state at negative $643 million, even with its large GO sale Thursday.

Many participants have noted the high-tax states — California, New York and Massachusetts — will create even more demand for their paper, further pushing yields down.

In the primary, Morgan Stanley & Co. LLC priced and repriced for King County, Washington, $238.355 million of exempt limited tax general obligation refunding bonds (payable from sewer revenues), 2021, Series A (Aaa/AAA//) with bumps from a morning wire. Bonds in 2022 with a 3% coupon yield 0.05% (-1), 4s of 2026 at 0.30% (-6), 5s of 2031 at 0.92% (-1), 2s of 2036 at 1.68% (-1) and 3s of 2038 at 1.57%.

Goldman Sachs & Co. LLC priced and repriced for Philadelphia (A2/A/A-/) $297.76 million of general obligation bonds with bumps: 5s of 2022 at 0.10% (-1), 5s of 2026 at 0.47% (-3), 5s of 2031 at 1.12%, 5s of 2036 at 1.41% (+2), 4s of 2041 at 1.65% (-4) and 4s of 2042 at 1.66% (-6).

Wells Fargo Corporate & Investment Banking priced and repriced for the New Mexico Finance Authority (Aa2/AA//AAA) $235 million of state transportation revenue bonds with bumps in the repricing: 5s of 2025 at 0.24% (-7), 5s of 2026 at 0.38% (-9) and 5s of 2030 at 0.90% (-7).

BofA Securities priced and repriced for Colorado Springs (Aa2/AA+//) $219.117 million of utilities system refunding revenue bonds with bumps of one to three basis points. The first tranche, $38.755 million, saw 5s of 2021 at 0.07%, 5s of 2022 at 0.08%, 5s of 2026 at 0.43% (-3), 5s of 2033 at 1.08% (-2). The second, $180.415 million, saw 5s of 2022 at 0.08%, 5s of 2026 at 0.43% (-3), 5s of 2031 at 0.95% (-3), 5s of 2036 at 1.17% (-2), 4s of 2041 at 1.47% (-1), 4s of 2046 at 1.64% and 4s of 2051 at 1.71%.

The New York trader said he doesn’t expect any significant short-term change in market dynamics, until at least the fall, due to the potential for both economic volatility and the arrival of an uptick in volume.

“The specter of inflation and the global economy will impact the market if we go through another slowdown due to the new variant of COVID,” he said.

“There’s enough trepidation from the economists that there could be another slow down and shut down,” he noted. “If we go through all of that again like in the spring then all bets are off and rates will stay low.”

Secondary trading and scales

Trading showed Louisiana 5s of 22 at 0.08%. Wake County, North Carolina 5s of 2022 at 0.045%. Fairfax County, Virginia 5s of 2024 at 0.16%-0.15%. Georgia 4s of 2025 at 0.28%-0.24% versus 0.32% Monday.

Connecticut revolving fund waters 5s of 2026 at 0.36%. New York Dorm PITs 5s of 2027 at 0.45%. Howard County, Maryland 5s of 2029 at 0.81%.

Portland, Oregon 2s of 2033 at 1.41%. Los Angeles Department of Water and Power 5s of 2034 at 0.96%. Washington 5s of 2037 at 1.18%. LA DWP 5s of 2040 at 1.21%. California 5s of 2041 at 1.27%.

LA DWP 5s of 2051 at 1.44%.

According to Refinitiv MMD, yields were steady at 0.05% in 2022 and at 0.06% in 2023. The yield on the 10-year fell one basis point to 0.82% while the yield on the 30-year fell to 1.35%.

ICE municipal yield curve saw the one-year down one basis point to 0.04% in 2022 and steady at 0.06% in 2023. The 10-year maturity at 0.84% and the 30-year yield sat at 1.35%.

The IHS Markit municipal analytics curve saw the one-year steady at 0.05% and the two-year at 0.06%, with the 10-year at 0.83%, and the 30-year yield at 1.35%, both steady.

Bloomberg BVAL saw levels down one basis point to 0.04% in 2022 and steady at 0.05% in 2023 while the 10-year fell one basis point to 0.82% and the 30-year fell one to 1.34%.

Treasuries were stronger while equities were in the red. The 10-year Treasury was yielding 1.235% and the 30-year Treasury was yielding 1.888% in late trading. The Dow Jones Industrial Average lost 136 points or 0.39%, the S&P 500 fell 0.66% while the Nasdaq fell 0.43%.

NYC TFA to sell $1.1B bonds next week

The New York City Transitional Finance Authority said Tuesday it will issue about $1.1 billion of future tax-secured subordinate bonds next week.

The deal will be composed of around $934 million of tax-exempt fixed-rate bonds and about $117 million of taxable fixed-rate bonds.

The tax-exempts will be priced for institutions on Wednesday, Aug. 4, after a two-day retail order period. The bonds will be priced by book-running lead manager Siebert Williams Shank with Jefferies and Loop Capital Markets as co-senior managers.

Also on Aug. 4, TFA will competitively sell the taxable deal. Proceeds from the sale will be used to refund certain outstanding bonds for savings.

Economy

The economy continues to recover, with durable goods orders and consumer confidence suggesting strength, but concerns about the Delta variant of COVID-19 and continued supply-chain problems cloud the future outlook.

“It appears the U.S. economy continues to be on a self-sustaining pace,” according to Ed Moya, senior market analyst for the Americas at OANDA.

Business investment “disappointed” in June, leaving it up slightly in the quarter, according to Diane Swonk, chief economist at Grant Thornton. She expects a rebound in the summer months, but “the largest hurdles are supply chain bottlenecks and uncertainty triggered by the spread of the Delta variant.”

Durable goods rose 0.8% in June after climbing a revised 3.2% in May, first reported as a 2.3% gain.

Excluding transportation, new orders increased 0.3% in June after rising 0.5% in May, originally reported as a 0.3% increase. Excluding defense, new orders gained 1.0% following a revised 2.8% increase, first reported as a 1.7% climb.

Economists polled by IFR Markets surveyed anticipated a gain of 2.1% in May for the headline number, and a 0.8% rise excluding transportation.

Also released Tuesday, the consumer confidence index ticked up to 129.1 in July (its highest since 132.6 in February 2020) from 128.9 in June, while the present situation index gained to 160.3 from 159.6 and the expectations index dipped to 108.4 from 108.5, the Conference Board said.

Economists polled estimated a 124.1 read.

“Economic growth in Q3 is off to a strong start,” said Lynn Franco, senior director of economic indicators at The Conference Board. “Consumers’ optimism about the short-term outlook didn’t waver, and they continued to expect that business conditions, jobs, and personal financial prospects will improve.”

She also noted, “Short-term inflation expectations eased slightly” and more “consumers said they planned to purchase homes, automobiles, and major appliances in the coming month,” suggesting “consumer spending should continue to support robust economic growth in the second half of 2021.”

This, in turn, will allow companies to continue “passing on rising costs,” said OANDA’s Moya.

Separately, home prices jumped 16.6% in May from a year earlier after a 1.4% increase, S&P CoreLogic Case-Shiller.

The 10-city composite increased 16.4% from a year ago after a 14.5% rise a month earlier, while the 20-city jumped 17.0% after a 15.0% rise in April.

On a month-over-month basis, the national index gained 2.1%, while the 10-city rose 1.9% and the 20-city climbed 2.1%.

Economists expected a 1.5% increase for the month and a 16.3% rise annually for the national numbers.

Price gains were at record levels in May, said Craig J. Lazzara, managing director and global head of index investment strategy at S&P DJI, with prices nationally accelerating for 12 months in a row.

The housing market “remains hot after breaking home price records in May, but this is likely the peak,” said Moya.

Also released Tuesday, the service sector in Texas “accelerated” in July and although prices “eased” slightly, they remain near record levels, according to the Texas Service Sector Outlook Survey, released by the Federal Reserve Bank of Dallas.

The general business activity index slipped to 33.3 in July from 36.2 in June, while the company outlook rose to 25.0 from 21.7.

The revenue index increased to 21.7 in July from 16.7 in June. The employment index rose to 13.5 from 11.1, while the part-time part-time employment index grew to 8.3 from 5.4 and the hours worked index dipped to 8.5 from 10.8.

Input prices slipped to 42.0 from 44.9 and selling prices decreased to 24.4 from 28.6.

Service sector activity in the Richmond area softened in July, according to the fifth district service sector survey released by the Federal Reserve Bank of Richmond. The indexes for revenues, demand and local business conditions were all down in the month, although still suggesting expansion.

Prices paid rose to 5.94 from 5.24, while prices received inched up to 3.41 from 3.29.

“Growth of prices paid outpaced that of prices received, but participants expected the gap between them to narrow in the near future,” said the report.

The regional manufacturing sector “strengthened” in July, the Richmond Fed reported.

The manufacturing index ticked up to 27 in July from 26 the prior month.

Prices paid rose to 11.16 from 8.57 and prices received gained to 6.93 from 4.70.

“Respondents expected price growth to slow over the next year,” said the report.

The employment index rose while average workweek fell. “Survey results indicated that many firms increased employment and wages in July, but they struggled to find workers with the necessary skill,” the survey said.

Lynne Funk and Chip Barnett contributed to this report.