Weakness moved out the yield curve Thursday as secondary bid-wanteds were still elevated while U.S. Treasuries pared earlier losses and equities sold off in the afternoon as news out of Afghanistan grew worse.

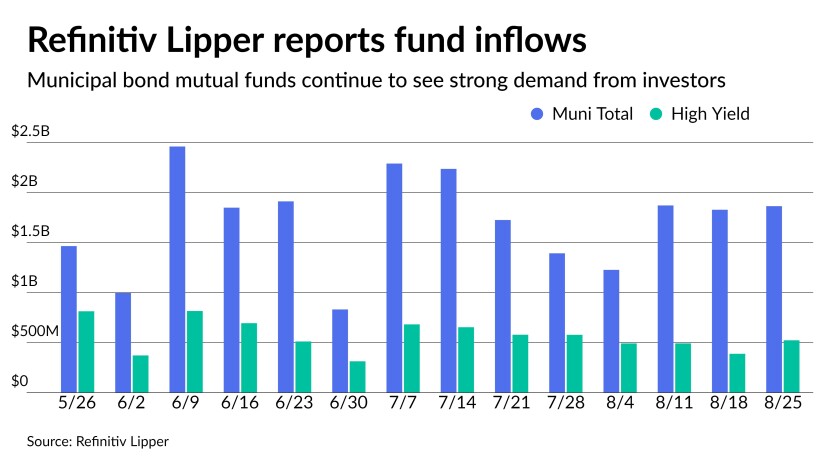

For the 25th straight week, Refinitiv Lipper reported inflows into municipal bond funds. Investors put $1.9 billion of cash into the mutual funds, with high-yield seeing $524 million of that amount.

After a few sessions of a more active secondary market with larger-than-average totals of bonds out for the bid — $725.37 million Wednesday and $708 million Tuesday — activity slowed into the afternoon Thursday with par value traded at just over $5 billion versus $10 billion Wednesday.

The focus turned away from the few deals priced in the primary and to Jerome Powell’s speech in Jackson Hole following hawkish comments from two Fed presidents on tapering.

“What started as a modest increase in secondary bid list volume has become a more concentrated effort among a broader range of sellers as month-end approaches,” said Kim Olsan, senior vice president at FHN Financial. “End-of-month positioning is partially in play, but perhaps there’s also a sense that rates are more inclined to be nudged higher with limited opportunity to move much lower for the front third of the curve.”

Triple-A benchmarks were cut one to two basis points, the larger of which was outside of 10 years. Ratios were little changed with the 10-year muni-to-Treasury ratio at 68% and the 30-year at 78%, according to Refinitiv MMD. The 10-year muni-to-Treasury ratio was at 69% while the 30-year was at 77%, according to ICE Data Services.

In the primary, Piper Sandler priced for the Utah Military Installation Development Authority $260 million of tax allocation and hotel tax revenue bonds Series 2021A-1 and tax allocation revenue bonds Series 2021A-2. The first series saw bonds in 6/2036 with a 4% coupon yield 3.52%, 4s of 2041 at 3.71%, and 4s of 2052 at 3.90%, callable Sept. 1, 2029. The second, $138.725 million, saw 4s of 2036 at 3.62%, 4s of 2041 at 3.81% and 4s of 2052 at 4%.

BofA Securities priced and repriced for the Love Field Airport Modernization Corp. (/A-/A/) $250.495 million of Series 2021 AMT general airport revenue refunding bonds with a mix of bumps and cuts: 5s of 11/2022 at 0.22% (-5), 5s of 2026 at 0.72% (-2), 5s of 2031 at 1.49% (+3), 4s of 2036 at 1.90% (+5) and 4s of 2040 at 2.06%, callable Oct. 1, 2031.

Refinitiv Lipper reports $1.9B inflow

In the week ended Aug. 25, weekly reporting tax-exempt mutual funds saw $1.865 billion of inflows, Refinitiv Lipper said Thursday. It followed an inflow of $1.830 billion in the previous week.

Exchange-traded muni funds reported inflows of $265.218 million, after inflows of $360.393 million in the previous week. Ex-ETFs, muni funds saw inflows of $1.600 billion after inflows of $1.469 billion in the prior week.

The four-week moving average remained positive at $1.699 billion, after being in the green at $1.581 billion in the previous week.

Long-term muni bond funds had inflows of $1.020 billion in the latest week after inflows of $1.021 billion in the previous week. Intermediate-term funds had inflows of $253.323 million after inflows of $402.029 million in the prior week.

National funds had inflows of $1.745 billion after inflows of $1.714 billion while high-yield muni funds reported inflows of $523.509 million in the latest week, after inflows of $388.520 million the previous week.

Secondary trading and scales

New Mexico 5s of 2022 at 0.08% versus 0.09% Wednesday. Georgia 5s of 2023 at 0.12%. Connecticut 4s of 2024 at 0.17%. NYC 5s of 2026 at 0.44%. NYC TFA 5s of 2024 at 0.44%-0.43%.

Fairfax County 4s of 2029 at 0.81% versus 0.75% Friday. California 5s of 2031 at 1.01%-1.00% versus 1.01%-0.99% Tuesday. Georgia 5s of 2032 at 0.98% (0.95% on Aug. 18). Maryland 5s of 2033 at 1.07%-1.05% versus 1.05% Wednesday. Maryland 5s of 2034 at 1.10%-1.11%.

Washington 5s of 2042 at 1.52%-1.51% versus 1.51%-1.43% on Tuesday. Washington 5s of 2045 at 1.63%-1.62% (1.49% on Aug. 5).

Georgia road and tollway 3s of 2048 at 2.03%-1.90%. Dallas waterworks 3s of 2050 at 2.02% versus 2.00% original.

Short yields were cut steady at 0.07% in 2022 and 0.10% in 2023 on Refinitiv MMD’s scale. The yield on the 10-year rose two basis points to 0.91% while the yield on the 30-year rose two to 1.52%.

The ICE municipal yield curve showed bonds steady in 2022 at 0.08% and 0.11% in 2023. The 10-year maturity sat at 0.92% and the 30-year yield was at 1.50%.

The IHS Markit municipal analytics curve showed short yields steady at 0.07% and 0.09% in 2022 and 2023. The 10-year yield rose one to 0.92% and the 30-year yield rose one to 1.51%.

The Bloomberg BVAL curve showed short yields steady at 0.07% and 0.07% in 2022 and 2023. The 10-year yield rose one basis point to 0.92% and the 30-year yield rose two to 1.51%.

In late trading, Treasuries were steady as equities were weaker.

The 10-year Treasury was yielding 1.340% and the 30-year Treasury was yielding 1.939%. The Dow Jones Industrial Average lost 157 points or 0.45%, the S&P 500 lost 0.46% while the Nasdaq fell 0.50%.

Warm up

While Friday’s speech by Federal Reserve Board Chair Jerome Powell is the highlight of the Jackson Hole symposium, two Federal Reserve Bank presidents on Thursday renewed the call for tapering in televised interviews.

Kansas City Fed President Esther George said the panel should begin tapering its asset purchases “sooner rather than later” this year despite the issues the Delta variant may cause.

“I don’t think [the rise of the Delta variant] changes my own calculus that it is time to begin to make those adjustments, given the gains we have seen so far,” she said during an interview on Bloomberg TV.

The key, she said, was “to get started,” with details — including about exact start date and pace — less important.

Separately, Federal Reserve Bank of St. Louis president James Bullard told CNBC the asset purchases are no longer necessary, and he expects the Federal Open market Committee will agree on a wind-down plan, although he did not provide a timeline. “It does seem that we are coalescing around a plan.”

Powell seems to be less eager to begin tapering, although since the meeting and his semiannual monetary report to Congress, a strong employment report was released. At that time, the chair still believed the employment goal was “a ways away.”

Members of the Fed seem to be divided among those who are ready to taper now, those who want to see one more good employment report, and those looking for two more big gains in nonfarm payrolls before cutting back asset purchases.

The market will be keyed on Powell’s speech to see if his stance has changed and if he gives any definitions, timeline or hints about “substantial further progress” toward its employment goal.

George also spoke to Fox Business, where she said the baseline outlook is for more jobs and strong economic growth, adding Delta may trim employment gains, but it shouldn’t “derail the economy.”

Indeed, the preliminary second quarter gross domestic product read showed 6.6% growth in the three month period, better than the 6.5% gain in the advance read and the 6.3% climb in the first quarter.

Economists polled by IFR Markets expected a 6.7% gain.

“There were no surprises in today’s release but merely a reminder that the economy is recovering robustly from the economic disruptions of last year,” said Matt Peron, director of research at Janus Henderson Investors.

“The data continue to show that GDP growth was driven primarily by consumer spending, although business fixed investment spending also made a positive contribution to topline GDP growth,” said Wells Fargo Securities Chief Economist Jay Bryson and Economist Shannon Seery.

Corporate profits were at record levels in the period, they noted. “Wide profit margins suggest that businesses may have the ability to avoid passing on all cost increases to customers.”

Also released Thursday, initial jobless claims crept to 353,000 in the week ended Aug. 21 from a revised 349,000 a week earlier, first reported as 348,000.

Economists expected 350,000 claims.

Continuing claims slid to 2.862 million in the week ended Aug. 14 from 2.865 million the week before.

“The pandemic has demonstrated that few things move in a straight line and the latest snapshot of jobless claims is consistent with that,” said Bankrate Senior Economic Analyst Mark Hamrick. “The nation’s unemployment rate has dropped significantly from last year’s peak and may be poised to move lower.”

The four-week moving average fell to 366,500, a pandemic low, in the week ended Aug. 21 from 378,000 a week earlier. This suggests “the labor market continues to gradually recover,” said Scott Anderson, chief economist at Bank of the West.

Chip Barnett contributed to this report.