Municipal trading dropped 25% on Wednesday after an already very slow few days in the secondary, leaving municipal benchmark yields little changed, as U.S. Treasuries also held steady and most participants began checking out for the holiday weekend.

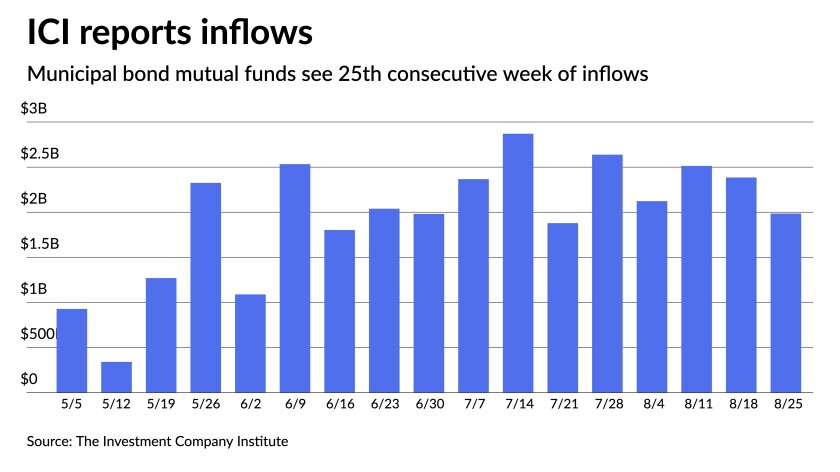

For the 25th week in a row, municipal bond mutual funds saw inflows of nearly $2 billion, bringing the total to $69 billion year-to-date.

The Investment Company Institute reported $1.985 billion of inflows into municipal bond mutual funds for the week ending August 25, following $2.385 billion of inflows the prior week.

Exchange-traded funds saw $378 million of inflows after $513 million and $210 million the two weeks prior.

Secondary trading was down 26% to a little more than $5 billion par value traded near the close, and bid-wanteds remained a little more than $400 million for the third day.

U.S. Treasury yields fell a basis point and ratios were steady Wednesday with the 10-year muni-to-Treasury ratio at 71% and the 30-year at 80%, according to Refinitiv MMD. The 10-year muni-to-Treasury ratio was at 74% while the 30-year was at 79%, according to ICE Data Services.

In the primary, RBC Capital Markets priced for institutions for the New York City Transitional Finance Authority (Aa1/AAA/AAA/) $950 million of future tax-secured subordinate bonds with five to seven basis point cuts to maturities out longer: Bonds in 8/2023 with a 3% coupon yield 0.15%, 5s of 2026 at 0.50%, 4s of 2036 at 1.64% (+5), 3s of 2041 at 2.08%, 4s of 2041 at 2.03%, 5s of 2045 at 1.85% (+5), 3s of 2048 at 2.29% (+5) and 4s of 2048 at 2.07% (+7).

The TFA sold $250 million of taxable future tax-secured bonds to Wells Fargo. Bonds in 2027 yield 1.36% at par, 1.55% in 2028 and 1.85% in 2033.

Stifel, Nicolaus & Company, Inc. priced for Akron, Ohio, (/AA-//) $114.97 million of community learning center income tax revenue refunding forward delivery bonds. Bonds in 12/2022 with 4% coupon yield 0.44%, 4s of 2026 at 0.92%, 4s of 2031 at 1.56% and 4s of 2033 at 1.67%, settlement date March 3, 2022, callable Dec. 1, 2029.

Secondary trading and scales

Trading was mostly steady. New York City Transitional Finance Authority 5s of 2022 traded at 0.07%-0.06%. California 5s of 2022 at 0.08%. Los Angeles Department of Water and Power 5s of 2022 at 0.07%.

Cary, North Carolina, 5s of 2027 at 0.57% versus 0.56% original. Wisconsin 5s of 2028 at 0.66% versus 0.63% a week ago and 0.65% original. Fairfax County 5s of 2028 at 0.69% versus 0.70% Tuesday.

Maryland 5s of 2033 at 1.10%-1.08% versus 1.05%-1.04% Tuesday.

Denver City and County 5s of 2033 at 1.06%. Washington 5s of 2035 at 1.36%. Washington 5s of 2041 at 1.43%.

New York City 5s of 2047 at 1.90%, the same as Tuesday and the original. New York City 5s of 2050 at 1.94%.

Short yields were steady at 0.08% in 2022 and 0.11% in 2023 on Refinitiv MMD’s scale. The yield on the 10-year rose one basis point to 0.93% (month change roll) while the yield on the 30-year sat at 1.52%.

The ICE municipal yield curve showed bonds steady in 2022 at 0.08% and down one to 0.11% in 2023. The 10-year maturity rose one basis point to 0.94% and the 30-year yield rose one to 1.51%.

The IHS Markit municipal analytics curve showed short yields steady at 0.08% and 0.10% in 2022 and 2023. The 10-year yield stayed at 0.93% and the 30-year yield held steady at 1.52%.

The Bloomberg BVAL curve showed short yields steady at 0.07% and 0.07% in 2022 and 2023. The 10-year yield stayed at 0.92% and the 30-year yield at 1.51%.

In late trading, Treasuries were a basis point better and equities were mixed.

The 10-year Treasury was yielding 1.30% and the 30-year Treasury was yielding 1.917%. The Dow Jones Industrial Average lost 59 points or 0.17%, the S&P 500 rose 0.03% while the Nasdaq gained 0.33%.

Jobs, jobs, jobs

The jobs situation remains in focus, and despite expectations for a 728,000 increase in nonfarm payrolls in the employment report for August, signs are suggesting those projections, and the belief of upcoming improvement in the labor market, could be optimistic.

Wednesday’s data — including the ADP report, which missed expectations and the Institute for Supply Management’s manufacturing survey, which showed employers continue to struggle to attract and retain help — could be concerning, analysts said.

“The ADP and ISM reports both highlight the problems employers are having with filling vacancies and that could start to raise the question of whether the economy will make substantial progress in the labor market over the next few months,” said Ed Moya, senior market analyst for the Americas at OANDA.

“Weakness in the labor market is becoming a consistent theme across the Fed regional surveys,” he added. “Employers are still having trouble filling vacancies and that will complicate the economy from hitting the Fed’s substantial progress goal.”

The issue, he said, “won’t get rectified anytime soon unless wages go up even more.”

The ADP report showed private-sector employment up 374,000 in August, following a downwardly revised 326,000 gain in July. Economists polled by IFR Markets expected 637,500 jobs added.

“The Delta variant of COVID-19 appears to have dented the job market recovery,” said Moody’s Analytics Chief Economist Mark Zandi. “Job growth remains strong, but well off the pace of recent months. Job growth remains inextricably tied to the path of the pandemic.”

The miss could be “a terrible warning sign ahead of Friday’s jobs report,” said Craig Erlam, senior market analyst, UK & EMEA, at OANDA. “The data piqued the interest of those in the markets but didn’t get much of a reaction, owing to its rare ability to actually provide reliable insight into the jobs report two days later.”

The number “will certainly get people thinking about the potential for a big miss in Friday’s NFP number,” he said.

Bank of the West projects a below-consensus 665,000 nonfarm payrolls jobs added, said its Chief Economist Scott Anderson, “but the disappointing ADP report implies our nonfarm payrolls forecast might still be too optimistic.”

But, Interactive Brokers’ Chief Strategist Steve Sosnick, asserted, “It is important to note that the ADP numbers have been a decent, but hardly foolproof indicator of the more important release two days later.”

He noted, last year, “ADP overshot” the nonfarm payrolls report “probably because the big businesses that use ADP recovered more quickly than small ones,” more typically surveyed for by the Bureau of Labor Statistics for the employment report.

However, “early this year, ADP lagged NFP by a month,” he said in an analysis.

Historically, ADP has not been a good indicator of what the employment report will show, he said. “Over the past 20 years, the correlation stinks. It is essentially random.”

Over the 16 months, albeit which is a limited scope, “it shows a better result,” Sosnick said, with a five-year look offering “a decent but unreliable correlation.”

The markets may understand ADP’s usefulness although it doesn’t necessarily foretell what will come in the employment report, Sosnick said, “because they barely reacted to a major miss this morning.”

Alternately, he said, “it could be that market nihilism means that investors simply don’t care or that the Goldilocks effect will allow investors to create a market-friendly narrative out of statistics no matter what.”

Jason England, global bonds portfolio manager at Janus Henderson Investors, agreed the two reports don’t always mesh. “Last month there was a similar large miss on expectations for the ADP report, yet the NFP print was still a solid number. So, although this does give us some concern that the employment report on Friday could disappoint, the more important concern for us is what impact the Delta variant had on jobs during August.”

Separately, the ISM report showed slightly faster expansion in August, with the new orders and production indexes both rising in the month, but employment fell to a contractionary read of 49.0 from expansionary 52.9 a month earlier, and the prices index retreated to 79.4 from 85.7, its first reading below 80 since December.

The employment read, suggests “a weak print in manufacturing payrolls in the BLS report,” Anderson said.

Despite “a very difficult environment,” Wells Fargo Securities senior economist Tim Quinlan said, “the manufacturing sector is finding ways to thrive.”

Perhaps the biggest issue is, “businesses cannot find the people to do the work in the nation’s factories,” he said. “The difficulty finding labor in August is warning sign that Friday’s headline number will not likely get much help from manufacturing payrolls and that a lack of labor remains a challenge to hiring more broadly.”

Wells cut back its expectations for payrolls to a 750,000 rise.

Also released on Wednesday, July construction spending grew an as-expected 0.3% after a revised flat reading in June, first reported as a 0.1% gain.

Primary market to come

Santa Cruz County, California, (/AAA//) is set to price $124.19 million of taxable pension obligation bonds on Thursday. Serials 2022-2036, terms 2041, 2047. Stifel, Nicolaus & Company, Inc.

In the competitive market on Thursday, Fremont Unified School District, California, is set to sell $116 million of taxable refunding bonds at 12:30 p.m.