Municipal yields rose Friday to close out a rough week ahead of a smaller new-issue calendar and the Fed’s expected rate hike.

“The yield curve has been — and will continue to be — the most important indicator we watch during Fed tightening cycles and rising rate environments,” said Wells Fargo Investment Institute Investment Strategy Analyst Luis Alvarado. “Fixed income still plays a key role inside a portfolio for investors in search for yield, but also as a potential stabilizer when unexpected risks surface.”

Triple-A yield curves saw three to six basis point cuts while short UST rose two to four and the longer end pared back earlier losses.

Municipal to UST ratios showed the five-year at to 80%, 92% in 10-years and 94% in 30, according to Refinitiv MMD’s 3 p.m. read. ICE Data Services had the five at 79%, the 10 at 96% and the 30 at 97% at a 3:30 p.m. read.

Supply has been lackluster so far this year, and next week’s calendar is relatively light, as issuers hold back due to the Fed’s expected 25 basis point rate hike at its next FOMC meeting.

Next week’s potential volume is slated to be $5.110 billion, $4.392 billion of which are negotiated deals and $718.1 million of competitive loans.

The largest deal of the week comes from the Dormitory of the State of New York with $2.3 billion of exempt state personal income tax revenue bonds and $662.32 million of taxables. Other notable deals include $583 million of general revenue bonds from the Regents of the University of Michigan, $572 million of taxable bonds from the University of Massachusetts Building Authority and $370 million of wastewater system subordinate revenue bonds from the city of Los Angeles.

Guilford County, North Carolina leads the competitive calendar with two deals over $160 million.

Following Russia’s invasion of Ukraine, the flight to Treasuries came to an end this week as the 10-year Treasury yield rally came to a halt on Monday with yields subsequently rising throughout the week, said BofA Global Research strategists.

Treasury rates have increased to levels close to those seen in February’s first half. The Fed futures market now expects almost seven rate rises in 2022, they said.

“Beside the geopolitical uncertainty and the resulting impact on various entities and asset classes, the fact that the Fed ceased quantitative easing operations and is imminently preparing for a rate hike, and then quantitative tightening, appears to have led to some liquidity issues in Treasuries and elevated volatility,” they said.

The liquidity issue can also be felt in munis, as bid/ask spreads for both tax-exempt and taxable bonds widened slightly compared to last year. BofA strategists said both primary and secondary market volumes have plummeted to dangerously low levels.

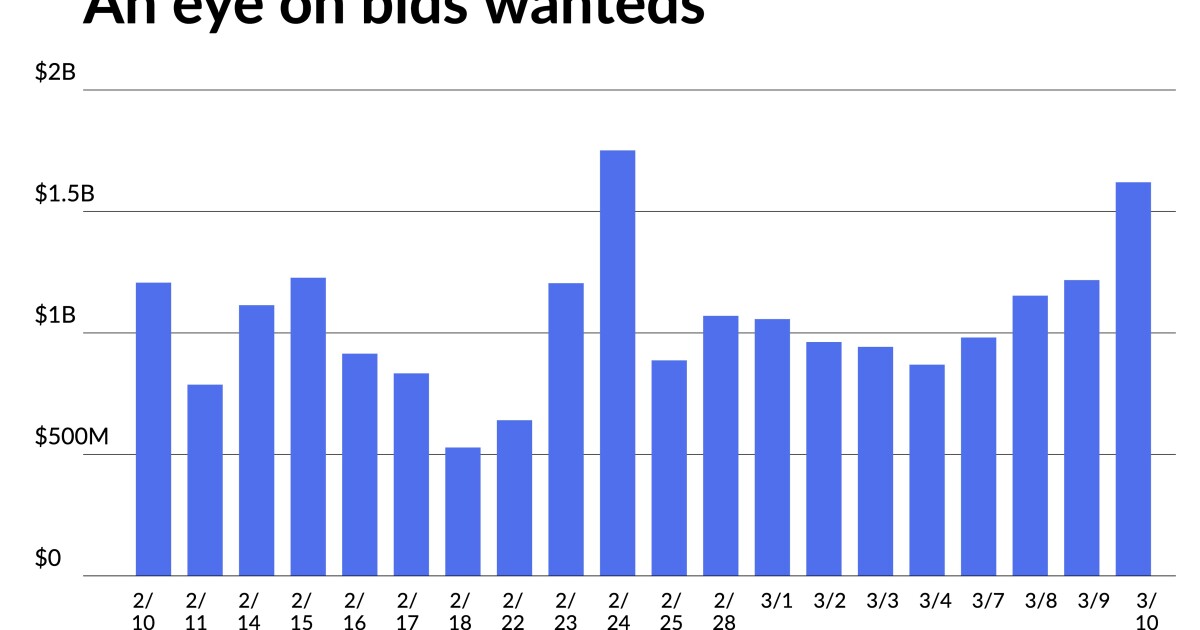

Bids wanteds reached $1.62 billion on Thursday after $1.217 billion Wednesday. Bids wanteds have eclipsed $1 billion 19 times since the start of the year.

Lower liquidity difficulties are largely to blame for slowly widening muni credit spreads, the BofA report said.

Treasury market volatility and the consequent outflows from mutual funds are mostly to blame for muni liquidity concerns. When the economy was rocked by the COVID-19 crisis in March 2020, the liquidity problem was credit-driven, but this time, the root of the liquidity problem is solely rate-related. Municipal credit quality continues to improve, according to BofA strategists.

As triple-A rates soared, mutual fund outflows became increasingly negative. While the Fed or the Treasury Department may have a role in improving Treasury liquidity, they said muni liquidity is mostly determined by mutual fund flows, high net worth investors’ participation and the dealer community’s willingness to take on greater inventories.

Barclays strategists said the most popular question that municipal investors are asking these days is when they should start actively buying, given that munis have consistently underperformed rates this year and muni-UST ratios are cheap at the moment — especially compared with the levels of late-2020 through 2021 when tax-exempts became extremely rich both outright and versus Treasuries.

They said investors may start buying even at current levels but believe that the 100% level on the 10-year and the 105%-110% level on the 30-year constitute solid buying indications, at least historically, if such levels are achieved.

They predict tax-exempt pressure to increase in the short term, as rate volatility will likely continue high, fund outflows will persist, and supply will gradually increase, as some issuers may contemplate expediting their deals owing to inflation and rate volatility.

As much bad news is being priced in at current levels, Barclays strategists said muni ratio highs for the year might be achieved in March and April, and investors should stay patient for now.

But while muni ratios are cheap, credit spreads are still very tight, albeit they have begun to expand in recent weeks.

“Taking the richness of credit spreads into account, investors should exercise the up-in-quality approach when accumulating municipal exposure, at least until credit spreads widen further,” they said. “Municipal credit is still in very good shape at the moment, and pressure is unlikely to build on the vast majority of municipal names, but to us it is a valuations, rather than a credit quality, call.”

Secondary trading

New York City TFA 5s of 2023 at 1.18%-1.00%. Massachusetts 5s of 2024 at 1.39-1.40%. California 5s of 2025 at 1.56-1.57%. Baltimore County, Maryland 5s of 2026 at 1.55% versus 1.26% original. NYC Municipal Water Finance Authority 5s of 2026 at 1.65-1.68% versus 1.38% on March 2 and 1.36-1.37% on March 3.

Maryland 5s of 2028 at 1.77-1.78%. Cambridge, Massachusetts 5s of 2028 at 1.63%-1.62%. Maryland 4s of 2029 at 1.88% versus 1.80% Wednesday. NYC TFA 5s of 2030 at 1.98-1.99%. Maryland 5s of 2031 at 1.89% versus 1.74% Tuesday and 1.76-1.78% Thursday. California 5s of 2030 at 2.00% versus 1.69%-1.62% on March 3.

NYC Municipal Water Finance Authority 5s of 2034 at 2.28% versus 2.15-2.19% Wednesday and 2.22-2.25% Thursday. Baltimore County, Maryland 5s of 2037 at 2.11-2.16% versus 1.94% Monday.

LA DWP 5s of 2047 at 2.55%-2.57% versus 2.45%-2.46% Wednesday and 2.39%-2.41% Tuesday and 2.31% original. New York City TFA 5s of 2051 at 2.73%-2.72%, the same as Thursday. LA DWP 5s of 2052 at 2.62%-2.61% versus 2.36% original.

AAA scales

Refinitiv MMD’s scale saw three to four basis point cuts at the 3 p.m. read: the one-year at 1.03% (+3) and 1.29% (+3) in two years. The five-year at 1.56% (+4), the 10-year at 1.84% (+3) and the 30-year at 2.26% (+3).

The ICE municipal yield curve was cut four to six basis points: 1.02% (+6) in 2023 and 1.33% (+6) in 2024. The five-year at 1.56% (+6), the 10-year was at 1.89% (+5) and the 30-year yield was at 2.29% (+5) in a 3:30 p.m. read.

The IHS Markit municipal curve was also cut: 1.02% (+4) in 2023 and 1.29% (+4) in 2024. The five-year at 1.56% (+4), the 10-year at 1.84% (+4) and the 30-year at 2.24% (+4) at a 4 p.m. read.

Bloomberg BVAL saw two to three basis point cuts: 0.99% (+2) in 2023 and 1.24% (+3) in 2024. The five-year at 1.53% (+2), the 10-year at 1.83% (+3) and the 30-year at 2.24% (+3) at a 3:30 p.m. read.

Treasuries were weaker while equities ended in the red.

The two-year UST was yielding 1.739%, the five-year was yielding 1.948%, the 10-year yielding 1.997%, and the 30-year Treasury was yielding 2.360% near the close. The Dow Jones Industrial Average lost 176 points or 0.53%, the S&P was down 0.99% while the Nasdaq lost 1.79% just before the close.

FOMC preview

Predicting the future is never easy. The Federal Reserve’s job entails predicting the economy’s path and coming out of a pandemic and with a war raging, the task gets harder.

“The Fed is currently navigating in an economic and financial environment that is more complicated than any other in recent history,” Wells’ Alvarado said. “We believe that the number of rate hikes in 2022 remains flexible and dependent on how the economy, the pandemic, and inflation levels continue to evolve.”

The first of those 25 basis point hikes is expected on Wednesday, after the Federal Open Market Committee’s two-day meeting. What happens after that is unknown.

With the consumer price index coming in as expected, Jake Remley, senior portfolio manager at Income Research + Management, said the likely outcome is a quarter point hike.

“Ostensibly, the Fed is trying to balance inflation and economic growth,” he said. “However, historically runaway inflation has proven harder to break than growth.”

And while he thinks the Fed doesn’t consider this runaway inflation, policymakers’ concerns will lead to “continued hawkish rhetoric as they collect more data.”

Things are “far more challenging for central bankers,” said DWS Group U.S. Economist Christian Scherrmann “Geopolitical risks emanating from the Ukraine/Russia conflict have made the economic outlook far more uncertain and have worsened financial conditions and may prolong some price pressures that might otherwise have moderated.

Also, monetary policy cannot solve some issues that have elevated inflation. “Price pressures provoked by global supply chain disruptions, for example, will not vanish because policy rates are raised,” he said. “For now, the central banks’ primary target must therefore be to control inflation expectations, which depends on central bankers retaining people’s confidence that they will enact the policies needed to stabilize prices.”

The meeting, Scherrmann said, “will therefore be an important test of credibility.”

The uncertainty may mean balance sheet reduction “could be more moderate than initially expected,” he said, although when the minutes of the meeting are released, they provide insight “on how the Fed intends to design the reduction of its balance sheet.”

Directing a soft landing “won’t be easy,” Scherrmann added, “but at present we don’t believe the economy is set on a path to recession as rates rise.”

While labor markets are “recovering” and the economy appears “robust,” he said, growth probably falls victim to inflation and higher interest rates. “We expect that scenario to be reflected in the FOMC’s updated Summary of Economic Projections,” Scherrmann said. “In terms of credibility, the longer-run projections on the appropriate policy path will be crucial in the March meeting. Too low interest rates might suggest to the markets that the Fed is not taking its inflation fighting role seriously enough. Too high rates, on the other hand, might weigh heavily on financial conditions.”

The Fed may still view inflation as transitory, said Jeff Klingelhofer, co-head of investments and portfolio manager at Thornburg Investment Management, “but officials have been forced to quiet their rhetoric on the notion because it’s no longer politically acceptable to utter the word transitory.”

And while the Fed was likely to face a hiking cycle, he said, “President Biden strong-armed” them to abandon “the word transitory and commit to a hiking cycle.”

As a result, Klingelhofer said, “the Fed has painted themselves into a corner, holding a timeline for transitory,” which forces them to continue raising rates as long as inflation is elevated. “Officials at the Fed have their fingers crossed that inflation falls before they get much above a 1% fed funds rate which is likely to be close to neutral.”

And this is bad for the bond market, he added. “Spreads entered the rising rate environment from an already tight positioning, even with the belief that rising rates resulted from strong and sustained rates of growth,” Klingelhofer said. “Simply put, spreads have minimal room to continue to tighten. On the flip side, rates have moved higher and can absolutely move up from here, resulting in a tough outcome for many bond investors.”

But there’s hope for investors, he said. “Higher rates aren’t a recipe for doom and gloom,” Klingelhofer said, especially if the Fed negotiates a soft landing.

The Fed hikes might come “at precisely the wrong time,” he said, as inflation wanes and the economy slows. “We take solace in that the Fed remains patient and will pause at a level that remains below neutral.”

But a 50-basis-point liftoff was never considered by Julian Brigden of Macro Intelligence 2 Partners, “in part because such a move would suggest the Fed was behind the curve, something a central bank doesn’t want to admit.”

Also, since this will be a tightening cycle, he said, “there is no need for initial shock and awe. Better to start slow and steady.”

Federal Reserve Board Chair Jerome Powell’s will offer a hawkish message in his press conference, Brigden said. “Bottom line, even if headline inflation peaks into the summer, the Fed is embarking on a multiyear tightening of rates and reduction in the balance sheet. That’s the message that Powell will have to convey.”

The Fed faces “an unenviable choice,” said Huw Roberts, head of analytics at Quant Insight. “Their ability to engineer a soft landing was already fraught but now the Ukrainian conflict and its impact on energy and food makes it nigh on impossible.”

The question is how tight financial conditions become in response to Fed tightening, he said. “That answer will include the level of credit spreads, shape of the yield curve, currency strength etc.”

Turning to the Summary of Economic Projections, Ivan Naranjo, fixed income portfolio manager at Homestead Funds, expects “a more hawkish tone from the Fed to counterbalance the latest uptick in inflation.”

The median long-term expectations will offer a clue about where the Fed expects the terminal rate, he said, “and could give us a hint of how worried they are about higher inflation for longer.”

At future meetings, Naranjo said, “the possibility of a 50 bps rate hike … is very real.”

Wilmington Trust Chief Economist Luke Tilley and Senior Economist Rhea Thomas, agree about the possibility of “larger rate hikes going forward.”

Most “FOMC participants will raise their inflation and rate hike forecasts in the Summary of Economic Projections next week, but reduce GDP expectations,” they said. “That’s not necessarily stagflation, but it puts them in an increasingly uncomfortable spot with higher inflation and slowing growth.”

And uncertainty will take center stage, with a reminder that policy will depend on data, Tilley and Thomas said. “That need to remain nimble is always the case, but should get more air time in the current environment.”

Separately, the University of Michigan consumer sentiment index fell to 59.7 in the preliminary march read from the final 62.8 in February, as the war in Ukraine has caused gas prices to spike.

The current conditions index fell to 67.8 from 68.2 and the expectations index dropped to 54.4 from 59.4.

The one-year inflation expectations climbed to 5.4%, a level not seen since 1981, from 4.9%, while the five-year inflation read held at 3.0%.

Primary to come:

Dormitory Authority of the State of New York is set to price Tuesday $2.314 billion of general purpose tax-exempt state personal income tax revenue bonds, Series 2022A, serials 2023-2042, terms 2047, 2052. J.P. Morgan Securities.

DASNY will also price on Tuesday $663.32 million of taxable personal income tax revenue bonds, serials 2023-2037. Siebert Williams Shank.

The Regents of the University of Michigan (Aaa/AAA//) is set to price daily $582.74 million of taxable general revenue bonds, Series 2022C. Goldman Sachs.

University of Massachusetts Building Authority (Aa2/AA-/AA/) is set to price Tuesday $571.84 million of taxable senior bonds, consisting of $351.95 million of project revenue bonds, Series 2022-2, serials 2024-2037, terms 2042 and 2052 and $219.89 million of refunding revenue bonds, Series 2022-3, serials 2022-2037, term 2041. Citigroup Global Markets.

Los Angeles, California (/AA/AA/AA/) is set to price Tuesday $370.345 million of wastewater system subordinate revenue bonds, Refunding Series 2022-C, serials 2023-2032. Jefferies.

Francis Howell R-III School District, Missouri (/AA//) is set to price Thursday $146.645 million of general obligation bonds, Series 2022, serials 2023-2024 and 2026-2042. Stifel, Nicolaus & Co.

The Arizona Sports and Tourism Authority (/AA//) is set to price daily $144.835 million of senior revenue and revenue refunding bonds, Series 2022, serials 2023-2036, insured by Build America Mutual. RBC Capital Markets.

Competitive:

Guilford County, North Carolina (Aaa/AAA/AAA/) is set to sell $41 million of general obligation public improvement bonds, Series 2022A at 11:30 a.m. eastern Tuesday.

Guilford County, North Carolina (Aaa/AAA/AAA/) is set to sell $120 million of general obligation school bonds, Series 2022B at 11 a.m. Tuesday.