Triple-A yields rose further Tuesday with four to six basis point cuts across the yield curve following along U.S. Treasuries while equities rallied.

Municipal to UST ratios showed the five-year at to 80%, 92% in 10-years and 96% in 30, according to Refinitiv MMD’s 3 p.m. read. ICE Data Services had the five at 79%, the 10 at 95% and the 30 at 97% at a 4 p.m. read.

Bond investors are understandably cautious in response to recent market volatility and ahead of what is expected to be a Fed rate hike Wednesday, participants say.

In the primary Tuesday, the Dormitory Authority of the State of New York saw cuts for institutional pricing from Monday’s retail offering. Bumps were then made from a preliminary pricing in the morning and the deal was upsized.

J.P. Morgan Securities priced for DASNY (/AA+/AA+/) $2.415 million of tax-exempt general purpose state personal income tax revenue bonds, Series 2022A, with five to 20 basis point cuts from its Monday retail scale. Bonds in 3/2023 with a 5% coupon yield 1.18% (+5), 5s of 2027 at 1.98% (+15), 5s of 2032 at 2.45% (+16), 5s of 2037 at 2.86%, 4s of 2042 at 3.22% (+20), 5s of 2046 at 3.11% and 3.5s of 2052 at 3.71%, callable 3/15/2032.

Siebert Williams Shank also priced $667.735 million of taxable PITs for the issuer.

In the competitive market, Guilford County, North Carolina (Aaa/AAA/AAA/) sold $120 million of general obligation school bonds, Series 2022B, to Piper Sandler & Co. Bonds in 3/2024 with a 4% coupon yield 1.44%, 5s of 2027 at 1.71%, 5s of 2032 at 1.99%, 2.875s of 2037 at 2.88% and and 3s of 2042 at 3.06%, callable in 3/1/2032.

The county (Aaa/AAA/AAA/) also sold $41 million of GO public improvement bonds, Series 2022A, to Baird. Bonds in 3/2024 with a 5% coupon yields 1.44%, 5s of 2027 at 1.71%, 5s of 2032 at 2.00%, 3s of 2037 at 2.80% and 3.125s of 2042 at 3.08%, callable in 3/1/2032.

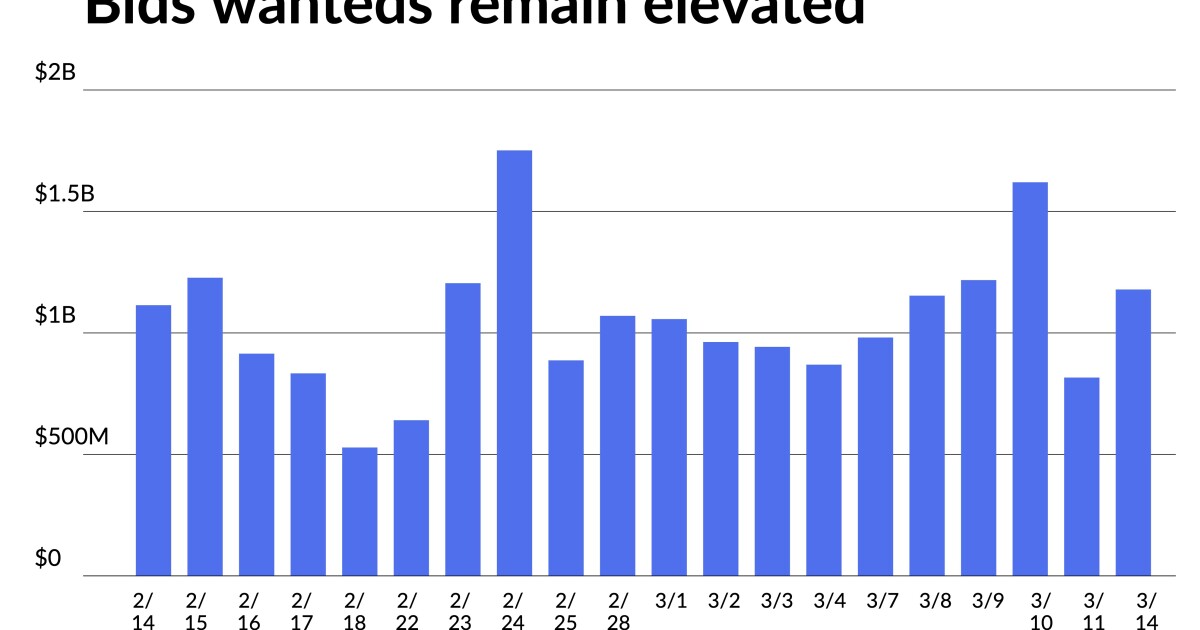

Selling pressure continues with bids wanted hitting $1.178 billion on Monday, the 20th time so far this year they’re eclipsed the $1 billion mark. At the mid-month mark, municipal returns are in the red. SO far in March, the Bloomberg main muni index has lost 1.83%, the high-yield index, 2.06%, taxables 3.78% and impact 2.42%.

Vikram Rai, head of Citi’s municipal strategy group, though, said he expects the market to stabilize this week, in part, due to the Fed’s expected rate hike of 25 basis points at its Federal Open Market Committee meeting. Historically, he said, stabilization occurs after the first rate hike in a cycle.

“The chances of a hawkish surprise are very low,” he said on Monday. “The inflation outlook remains troubling, but I doubt the Fed is going to start hiking rates dramatically because the inflation is coming from a supply chain problem.”

Last week’s muni-UST ratios were marginally wide, with the 30 year underperforming by 1.8 ratios to 96%. The 10-year muni-UST ratio was marginally tighter (-0.6 ratio), but at 92.4%, it was still fair-to-cheap.

Rai expects muni-UST ratios will widen further, with the long ratio remaining under pressure.

“Given that mutual funds aren’t really buying, that will keep pressure on the long ratio,” he said.

He said because muni-UST ratios and spreads are at their peaks, it presents an attractive buying opportunity.

While technicals are weak, meaning there could be elevated ratios, Rai said that just means there are more windows of opportunity to put cash to work. He said investors will see more opportunities over the next six weeks.

He also expects fund flows to improve, so there’s less bearish pressure on rates. “Flows could turn very quickly if the investor sentiment does,” he said.

However, municipals are hurting from net mutual fund outflows, which total $8.6 billion of outflows year-to-date, per Refinitiv Lipper data. This makes price discovery extremely difficult and forces underwriters to reorder the primary market in favor of non-fund buyers, said Matt Fabian, partner at Municipal Market Analytics.

This leads to higher yields, ratios, spreads, and coupons in new issuance, with the latter impacting values of newly issued low-coupon structures that are already dealing with models that risk de minimus discount limit-related losses.

Increased secondary selling pressure, a strong negative trend, retail apathy, and continuous fund redemptions gives credence to investor concerns.

“Higher current yields available among better well-rated, safe-sector credits and higher coupons in the belly of the curve present a reasonable allocation either once near-term negative momentum stabilizes, or now, as the start of a sequential investment program,” Fabian said.

But credit spreads are widening, especially on less-secure structures and/or worse credits, said Peter Block, managing director of credit strategy at Ramirez & Co.

“Given this, our base case through at least April is for tax-exempt underperformance on waning investor demand, driven by volatility, inflation, higher rates, and seasonal factors. Credit spreads are also likely to continue widening as investors take a defensive posture and increase credit quality,” Block said.

Secondary trading

New York City TFA 5s of 2023 at 1.35% versus 1.28%-1.19% Monday. California 5s of 2023 at 1.38%. NYC TFA 5s of 2024 at 1.71%. San Diego County Water Authority 5s of 2026 at 1.60%. New York City TFA 5s of 2026 at 1.81% versus 1.83% Monday.

New York City 5s of 2028 at 2.08-2.14%. Wisconsin 5s of 2028 at 1.90%. Connecticut green revs 5s of 2028 at 1.87%-1.86%. New York City 5s of 2029 at 2.16-2.20%. Maryland 5s of 2031 at 2.00-2.07% versus 2.02% Monday.

Baltimore County, Maryland 5s of 2034 at 2.18-2.20%.

Washington 5s of 2038 at 2.30% versus 2.30%-2.42% Monday. California 5s of 2042 at 2.63% versus 2.44%-2.47% Thursday.

LA DPW 5s of 2046 at 2.72% versus 2.64%-2.67% Monday. New York City 5s of 2047 at 2.92%-2.97%. New York City 5s of 2050 at 2.99%-3.00%.

AAA scales

Refinitiv MMD’s scale saw three to four basis point cuts at the 3 p.m. read: the one-year at 1.16% (+3) and 1.42% (+3) in two years. The five-year at 1.69% (+3), the 10-year at 1.98% (+4) and the 30-year at 2.39% (+3).

The ICE municipal yield curve was cut four to six basis points: 1.12% (+6) in 2023 and 1.44% (+5) in 2024. The five-year at 1.69% (+5), the 10-year was at 2.03% (+4) and the 30-year yield was at 2.43% (+5) in a 4 p.m. read.

The IHS Markit municipal curve was also cut: 1.15% (+3) in 2023 and 1.42% (+3) in 2024. The five-year at 1.69% (+3), the 10-year at 1.98% (+4) and the 30-year at 2.38% (+4) at a 4 p.m. read.

Bloomberg BVAL saw three to four basis point cuts: 1.14% (+4) in 2023 and 1.39% (+4) in 2024. The five-year at 1.68% (+4), the 10-year at 1.97% (+4) and the 30-year at 2.38% (+3) at a 4 p.m. read.

Treasuries were weaker while equities rallied.

The two-year UST was yielding 1.853%, the five-year was yielding 2.109%, the seven-year 2.168%, the 10-year yielding 2.157%, and the 30-year Treasury was yielding 2.493% at the close. The Dow Jones Industrial Average gained 599 points or 1.82%, the S&P was up 2.14% while the Nasdaq gained 2.92% at the close.

Economy

Data released Tuesday showed inflation continues to rage, with expectations the Russia-Ukraine war will keep energy prices soaring.

The producer price index rose 0.8% in February after an upwardly revised 1.2% gain in January, first reported as a 1.0% increase. Economists polled by IFR Markets expected a 0.9% gain. Year-over-year prices are up 10.0%, the same as in January.

The core rate, which excludes volatile food and energy categories, grew 0.2% in the month after an upwardly revised 1.0% climb, first reported as a 0.8% rise. Economists were looking for a 0.6% gain.

“It is important to note that this report doesn’t really capture the inflationary impact of the Ukraine-Russia conflict and the heavy sanctions that have been imposed since,” said Scott Anderson, chief economist at Bank of the West. “The smallest monthly gain in producer prices since October was driven by a 2.4% jump in goods prices — the largest on records that begin in 2009 — with two-thirds of the increase due to a surge of 8.2% in energy prices.”

And while services prices were steady in the month, the first time it hadn’t risen since December 2020, he said, “it is still too early to say if this is the start of a moderating trend.”

Separately, the Empire State Manufacturing Survey showed a contraction of activity in the state’s manufacturing sector, as the general business conditions index plunged to negative 11.8 in March from positive 3.1 in February.

Economists expected a 7.25 read.

While the prices paid index slipped to 73.8 from 76.6, the prices received rose to a record 56.1 from 54.1, “signaling ongoing substantial increases in both input prices and selling prices,” the report said.

Neither report will stop the 25-basis-point Fed rate increase on Wednesday, “and signaling many more rate hikes this year,” Anderson said.

“A softer-than-expected PPI report and a disappointing Empire survey supports the idea that the Fed won’t have to be aggressive with tightening policy over the next few meetings,” said Edward Moya, senior market analyst at OANDA.

“With an uncertain outlook over the medium-term, the Fed will hold off committing any additional beyond five for the year,” he said. “There is no benefit to overcommit on tightening expectations given all the geopolitical risk and inflation uncertainty that is on the table and potential recession risk from abroad.”

But, it may not be a unanimous decision, said Nikko Asset Management Chief Global Strategist John Vail. “The Fed will likely prove, just as the ECB did, somewhat more hawkish than just the expected 25 bps hike, with perhaps one or more dissents for 50 bps and rhetoric about 50 bps being prominently on the table next meeting,” he said.

The price of oil will be an important consideration for the FOMC, he added.

“The Fed is also cognizant of the 1960s when political considerations, the Vietnam war in that case, were used to pressure the Fed to remain dovish but unfortunately eventually led to sustained high inflation,” Vail said.

But, Bryce Doty, senior vice president/portfolio manager of Sit Investment Associates, expects a more hawkish Fed. “We expect the Fed to push short term yields to 2% as rapidly as possible without destabilizing financial markets,” he said.

While the Fed will engage in quantitative tightening, it “will have minimal effect initially given the excess liquidity in the financial system but could still spook investors,” he said.

“The Treasury yield curve will flatten, ”Doty said, “and likely even invert as short-term rates rise more quickly (due to the Fed) than long term yields as slower growth reduces long term inflation concerns.”

Still, a soft landing is difficult to negotiate, said Ned Davis Research Chief Global Macro Strategist Joe Kalish. Had the Fed moved earlier, their job on inflation would have been easier, he said.

“The overall evidence points to a stagflationary outcome at this point,” he said. “Except for real yields, financial market indicators are not yet warning of recession. On the economic side, except for consumer sentiment, the data do not yet support a recession call.”

But investors need to look past this rate hike, said Scott Ruesterholz, portfolio manager at Insight Investment. “The primary challenge for the markets and investors is not the first rate hike — policy is still quite accommodative — but the trajectory thereafter,” he said.

“The Fed faces a difficult paradox,” according to Ruesterholz. “On the one hand, with inflation already nearly 8%, the need to move quickly is enhanced by rising commodity prices, which threaten to keep inflation higher for even longer — we expect inflation to remain above target through 2023. However, rising commodity prices act like a tax on the economy, squeeze disposable incomes, and will force consumers to either save less or spend less on discretionary items. This can slow the economy, and a slowing economy is typically one where central banks tighten less.”