Municipals were better Friday after catching a bid in the secondary, finally following U.S. Treasuries in a flight-to-quality, while still underperforming, keeping valuations above 100% on the 10- and 30-year. Equities pared back earlier losses to end mixed after the S&P 500 dipped into bear market territory earlier in the session.

“The correlation between stocks and U.S. Treasuries is finally starting to normalize,” noted Barclays PLC in a weekly report. “Whereas the two were selling off or rebounding in sync amid higher inflation expectations and a hawkish Fed, over the past several weeks, the relationship has reverted to historical averages, with equities selling off in a risk-off environment while Treasuries rallied.”

Given that the volatility of risk assets looks set to remain high, “if the focus on the flight-to-safety increases, rates might remain in check, and all fixed-income assets could benefit as a result, including municipals,” Barclays strategists said.

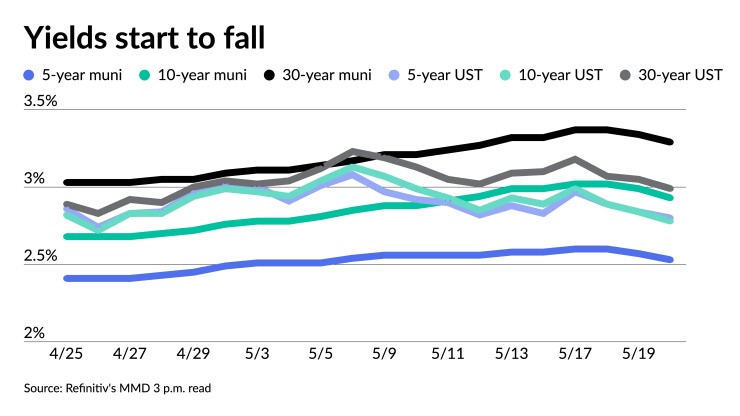

Municipals still underperformed UST on the week, but saw yields fall four to six basis points Friday while UST saw stronger gains out longer.

Muni to UST ratios were at 90% in five years, 105% in 10 years and 109% in 30, according to Refinitiv MMD’s 3 p.m. read. ICE Data Services had the five at 90%, the 10 at 104% and the 30 at 110% at a 4 p.m. read.

Investors will be greeted Monday with a decrease in supply with the new-issue calendar estimated at $5.763 billion in $4.192 billion of negotiated deals and $1.570 billion of competitive loans.

The primary calendar is led by $1.075 billion of general obligation bonds from Connecticut. Other notable deals include $268 million from Katy Independent School District, Texas; $225 million from Tarrant County, Texas; and $209 million from the Metropolitan Washington Airports.

Gilt-edged Loudoun County, Virginia, is expected to sell $157 million to lead the competitive calendar, along with Fort Worth, Texas, with $150 million.

As Treasuries rallied, tax-exempts mostly moved in the opposite direction this week, with the exception of Friday. The intermediate sector and long end underperformed, Barclays PLC said in a weekly report.

The 30-year municipal to UST ratio touched 110%, which is the highest of the year and a level last reached in late October 2020 and August 2015 before that, Barclays strategists said.

“In our view, this is attractive from a relative value standpoint, but for investors who are still looking to remain defensive, five-year and 10-year ratios also look compelling, currently at 90% and 105%; in general, we prefer 10-year ratios from a relative value perspective,” they said.

Barclays said that judging from the most recent market episode that is reminiscent of the current market environment — the Taper Tantrum of 2013 — even if rates stabilize, outflows may continue for quite some time. They noted that for the Taper Tantrum, from March 2013 to January 2014, outflows continued, but muni ratios reached their highest level against Treasuries and started to recover well before that.

“If rates indeed start to stabilize, another near-term support for the muni market is summer redemptions,” they said. This year’s redemptions are slightly below the usual pace (by about $10 billion year-to-date); however, starting in June, “they should become one of the main driving forces.”

Spread widening picked up speed this week, said BofA strategists Yingchen Li and Ian Rogow in a weekly report.

Spread widening for all credits was very mild in the first quarter of the year, but there was an observable acceleration in April and May, they said. High-yield munis also have seen significant spread widening since April, they said.

They noted that “spread risk cannot be ignored any more as high inflation and an unrelenting Fed are bound to cause more damage to the economy.”

“At this point, it is hard to envision how this credit widening will end as the Fed is trying hard to engineer a soft landing in its determined fight against inflation,” they said.

By certain measures, Li and Rogow said, “munis’ year-to-date selloff reached important milestones.” For instance, 5-year and up triple-A yields “surpassed the peak levels reached in the March 2020 market dislocation.”

“Even for the short end of the curve, where new purchase activities have concentrated, index total returns matched those in the first quarter of 2020,” according to BofA strategists.

These milestones, they said, could “indicate an important shift in the market for the remainder of the year; that is, from rates-driven to largely credit spread-driven moves.”

“More specifically, rates moves may have peaked while credit spread widening becomes the main risk for the remainder of the year,” Li and Rogow said. “As such, investors should stay with high-grade munis in our view.”

Despite these challenges, “timing is everything and there has not been a better time to buy municipal bonds in almost a decade,” said Jeff Timlin, managing partner and head of munis at Sage Advisory Services.

For one, he noted, “yields are at or near decade highs, and muni yields are attractive compared to other fixed-income markets.”

Additionally, muni valuations are attractive. “The worst drawdowns in munis over the last 20 years have been short-lived and painful, with an average drawdown of 8%; however, these periods have consistently been followed by strong rebounds of nearly 9%,” he said.

“A strong seasonal technical environment is setting up munis for high demand,” Timlin said. May and June, which can be weaker months, provide a good entry point to what is usually the strongest period for munis. June and July is a “heavy period of maturing bonds and coupon payments,” leading “to strong flows and favorable technical into late summer,” he said.

Li and Rogow noted, muni market buying has been concentrated in the front end of the curve.

It makes sense, given very high muni-UST ratios, “the ability to capture more of the curve’s yield shorter down the curve (an investor can capture 70% of the curve’s max yield at the three-year currently … but also given its relative attractiveness to other parts of the curve when interest rate risk is taken into account),” they said.

All the same, “it is important to note that even the short end of the curve’s total returns for the year-to-date are negative,” they added.

“While March 2020 returns had its rationale in a liquidity crisis as the economy fell off a cliff,” they said, “today’s high ratio in very short maturities seems to have liquidity and credit implication as well.”

“These implications are hard to justify, since by and large the Fed approach to rate hikes is still gradual in nature despite multiple 50 basis point hikes,” they said. “The Fed would have enough time and room to adjust its posture.”

Secondary trading

Maryland 5s of 2023 at 1.99%-1.93%. Maryland 5s of 2024 at 2.31% versus 2.35% Thursday.

New York Dorm NYU 5s of 2027 at 2.58%. New York City 5s of 2028 at 3.02%.

Gilbert, Arizona, green 5s of 2031 at 2.96% versus 3.23% original. Maryland 5s of 2031 at 2.93%-2.90%.

Washington 5s of 2034 at 3.28%-3.23%. Prince George’s County 5s of 2034 at 3.17% versus 3.30% original. Connecticut 5s of 2035 at 3.49%-3.48%. Anne Arundel County 5s of 2037 at 3.23%-3.18% versus 3.28%-3.27% Thursday. Prince George’s County 5s of 2038 at 3.28%-3.27% versus 3.43% original.

Gilbert, Arizona, green 5s of 2038 at 3.45% versus 3.56%-3.47% Thursday and 3.61% original.

Washington 5s of 2046 at 3.54%-3.51%. New York City TFA 5s of 2047 at 4.00%-3.92% versus 4.04% Thursday and 4.37%-4.35% Tuesday.

Triborough Bridge and Tunnel 5s of 2051at 4.15% versus 4.30% Thursday.

Los Angeles DWP 5s of 2052 at 3.80%-3.79%.

AAA scales

Refinitiv MMD’s scale was bumped four to six basis points at the 3 p.m. read: the one-year at 1.93% (-4) and 2.25% (-4) in two years. The five-year at 2.53% (-4), the 10-year at 2.93% (-6) and the 30-year at 3.29% (-5).

The ICE municipal yield bumped three to five basis points: 1.94% (-4) in 2023 and 2.30% (-4) in 2024. The five-year at 2.54% (-3), the 10-year was at 2.87% (-3) and the 30-year yield was at 3.32% (-5) at a 4 p.m. read.

The IHS Markit municipal curve saw bumps: 1.95 (-5) in 2023 and 2.25% (-5) in 2024. The five-year at 2.56% (-5), the 10-year was at 3.96% (-5) and the 30-year yield was at 3.30% (-5) at 4 p.m.

Bloomberg BVAL saw three to four basis point bumps: 1.96% (-3) in 2023 and 2.24% (-3) in 2024. The five-year at 2.59% (-3), the 10-year at 2.89% (-4) and the 30-year at 3.25% (-4) at a 4 p.m. read.

Treasuries were better.

The two-year UST was yielding 2.584% (-2), the three-year was at 2.735% (-3), five-year at 2.807% (-3), the seven-year 2.824% (-5), the 10-year yielding 2.788% (-5), the 20-year at 3.178% (-6) and the 30-year Treasury was yielding 2.987% (-8) just before the close.

Primary to come:

Connecticut is set to price Wednesday $1.075 billion of GOs, consisting of $150 million of general obligation bonds, 2022 Series C, serials 2023-2042; $575 million of general obligation refunding bonds, 2022 Series D, serials 2022-2028 and 2030-2032; $350 million of taxable general obligation bonds, 2022 Series A, serials 2023-2032. Ramirez & Co.

The Katy Independent School District, Texas, (Aaa/AAA//) is set to price Tuesday $268.035 million of unlimited tax school building Bonds, Series 2022, serials 2023-2042, terms 2047 and 2052, Permanent School Fund Guarantee Program. Siebert Williams Shank & Co

Tarrant County, Texas, (Aaa/AAA//) is set to price Monday $225 million of limited tax bonds, Series 2022, serials 2023-2042, term 2047. Siebert Williams Shank & Co.

The Metropolitan Washington Airports Authority, District of Columbia, (Aa3//AA-/) is set to price Wednesday $209.410 million of AMT airport system revenue refunding bonds, Series 2022A. J.P. Morgan Securities.

Midland, Texas, (Aa1//AAA/) is set to price Wednesday $173.705 million of taxable general obligation refunding bonds, Series 2022A, serials 2022 and 2030-2050. Raymond James & Associates.

The Tennessee Housing Development Agency (Aa1/AA+//) is set to price Thursday $149.990 million of non-AMT social residential finance program bonds, serials 2023-2034, terms 2037, 2042, 2048 and 2053. RBC Capital Markets.

Allentown Neighborhood Improvement Zone Development Authority, Pennsylvania, is set to price Tuesday $116 million of City Center Project subordinate tax revenue bonds, Series 2022, term 2042. Citigroup Global Markets.

Long Beach, California, (A3//A-/) is set to price Tuesday $111.875 million of senior airport revenue bonds, consisting of $48.175 million of governmental/non-AMT senior airport revenue refunding bonds, Series 2022A; $33.275 million of private activity/non-AMT senior airport revenue refunding bonds, Series 2022B; and $30.425 million of private activity/non-AMT senior airport revenue bonds, Series 2022C. Morgan Stanley & Co.

Competitive:

Loudoun County, Virginia, (Aaa/AAA/AAA/) is set to sell $165.685 million of general obligation public improvement bonds, Series 2022A, at 11 a.m. eastern Tuesday.

Fort Worth, Texas, (Aa1//AA/) is set to sell $150 million of water and sewer system revenue bonds, Series 2022, at 10:30 a.m. Tuesday.