Municipals were weaker Tuesday as short-end munis continued to sell off, U.S. Treasuries were weaker 10 years and in and equities were mixed.

Triple-A muni yields rose nine to 12 basis points in one-year, further inverting the curve on the short end. Heavy secondary trading on the short end moved one-year triple-A yields as much as nine basis points higher than the two- and five-year maturities, depending on the scale.

The one- to five-year inversion of five basis points has only happened 10 times during the past 41 years, noted Refinitiv MMD.

“The muni story of the moment is the now firmly implanted inversion and flattening in the first five years of the curve — with volatility usually reserved for equity markets,” said Kim Olsan, senior vice president of municipal bond trading at FHN Financial.

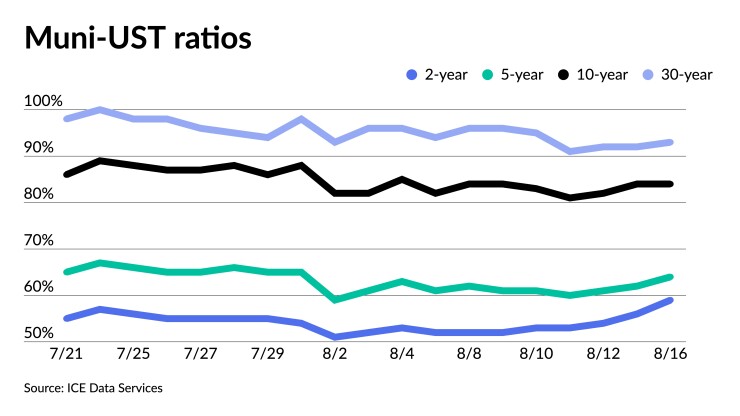

Short muni-UST ratios rose with the two- and three-year ratios, reaching near 60%. The five-year was at 64%, the 10-year at 81% and the 30-year at 96%, according to Refinitiv MMD’s 3 p.m. read. ICE Data Services had the five at 64%, the 10 at 84% and the 30 at 93% at a 3:30 p.m. read.

Olsan noted that “ultra-heavy selling combined with a ratio- and yield-adjusting theme in 2023 and 2024 has set up an unusual dynamic for the market.”

The UST curve has been inverted for much of the summer leading to ultra rich short muni to UST ratios.

Inversions haven’t happened that often in recent history, but she said “given ratios that fell below 50% there was some expectation of a correction.”

“A byproduct of the short yield spike is the re-emergence of short paper moving behind 2% again — more of a psychological than material aspect in that this yield range still is only about parity on a TEY basis with short USTs,” she added.

Trade data has shown one- to three-year volume rose 68% from prior sessions as a result of heavy bid list activity.

“High-quality commitments appear to be the preferred option, with rate volatility alone not needing to be complicated by credit concerns,” she said.

“Single-A and AMT-subject bonds are being discounted by a larger margin — Philadelphia Airport bonds due in 2023 (A2/A- and subject to AMT) were bought +63/AAA MMD after seeing compressed pricing early in the year closer to +40/AAA MMD,” Olsan said.

Several issuers are selling longer-dated debt into residual reinvestment demand while the market navigates an evolving curve slope, she said, pointing to Miami-Dade County, Florida’s AA-rated transit bonds (due 2043-2052), Long Island, New York’s A-rated electric bonds (maximum maturity 2044), and New York City’s GOs with a 2046 final maturity schedule.

“There is currently an implied extension opportunity into 25 years from the intermediate range, with a yield pickup of about 60 basis points,” according to Olsan.

“An aversion to front-end risks is reasonable, with the Fed continuing to message the likelihood of more hikes incoming,” said Matt Fabian, a partner at Municipal Market Analytics.

SIFMA is around 60% of 30-year nominal triple-A tax-exempt. Since the start of the pandemic, SIFMA has averaged 16% of the 30-year.

“It’s no wonder that the market has seen an uptick in floating-rate issuance attached to fixed payor swaps for non-governmental issuers (& banks are still paying just 0.13% to savings depositors),” he said. “Which, for the fixed-rate market, offsets a bit of longer-maturity issuance and helps keep long yields lower.”

This, he said, is in addition to “the trend MMA showed last week of the most (+$9.2B) net direct lending by banks to muni issuers” in a decade in the second quarter of the year.

“In other words, bank demand is robust and further flattening a curve that is already facing excess demand from scarcity, wavering inflation indicators, and still-strong credit performance,” Fabian said.

If fund flows turn more positive, “things could become even more extreme; this fact is likely steering automatic and model-based allocators away from tax-exempts,” he said.

“But where, in prior markets, this would have precipitated some gains taking, the opposite has been true — selling volumes last week fell to their lowest non-holiday total since February,” Fabian noted.

In the primary market Tuesday, Jefferies held a one-day retail order for New York City’s $950 million of tax-exempt general obligation bonds, Fiscal 2023 Series A, Sub-series A-1, with 5s of 9/2024 at 1.9%, 5s of 2027 at 2.03%, 5s of 2033 at 2.80%, 5s of 2037 at 3.21%, 5s of 2042 at 3.55%, and 4s of 2046 at 4.07%, callable 9/1/2032.

BofA Securities priced for the Long Island Power Authority, New York, (A2/A/A/) $331.095 million of general system revenue bonds. The first tranche, $131.095 million, Series 2022A, saw 5s of 9/2023 at 1.95%, 5s of 2027 at 2.06%, 5s of 2032 at 2.60%, 5s of 2037 at 3.19%, 5s of 2042 at 3.50% and 5s of 2044 at 3.58%, callable in 9/1/2032. The second tranche, $100 million of fixed-rate mandatory tender bonds, Series 2022B, saw 5s of 9/2052 at 2.24%, callable 3/1/2027. The third tranche, $100 million of SIFMA floating rate mandatory tender bonds, Series 2022C saw 9/2038 at +45 basis points SIFMA, callable 3/1/2025.

BofA Securities priced for the Arkansas Development Finance Authority (/BB-/BB/) $290 million of green AMT United States Steel Corp. Project environmental improvement revenue bonds, Series 2022, with 5.45s of 9/2052 at par, make whole call at MMD before 9/1/2025.

In the competitive market, Miami-Dade County, Florida, (/AA/AA/) sold $491.535 million of transit system sales surtax revenue bonds, Series 2022, to Goldman Sachs & Co, with 5s of 7/2043 at 3.77%, 5s of 2047 at 3.88% and 5s of 2052 at 4.02%, callable 7/1/2032.

Mecklenburg County, North Carolina, (Aaa/AAA/AAA/) sold $451.335 million of general obligation school bonds, Series 2022, to BofA Securities, with 5s of 9/2023 at 1.90%, 5s of 2027 at 1.85%, 5s of 2032 at 2.32%, 5s of 2037 at 3.31% and 5s of 2042 at 3.34%, callable 9/1/2032.

Secondary trading

North Carolina 5 of 2023 at 1.92% versus 1.82%-1.78% Friday. Prince George’s County, Maryland, 5s of 2023 at 2.02% versus 1.80% Friday. Maryland 5s of 2023 at 1.95%.

North Carolina 5 of 2024 at 1.93%-1.90% versus 1.72% Thursday. California 5s of 2024 at 1.81% versus 1.74% Monday and 1.65% on 8/3. DC 5s of 2024 at 1.91% versus 1.90% Monday.

California 5s of 2028 at 1.99%. Massachusetts 5s of 2029 at 2.10%-2.09%. Georgia 5s of 2031 at 2.29%-2.28%.

Prince George’s County, Maryland, 5s of 2038 at 2.81%-2.79% versus 2.72%-2.73% on 8/8. Columbus, Ohio, 5s of 2039 at 2.95%.

AAA scales

Refinitiv MMD’s scale was cut five to 10 basis points 3 p.m. read: the one-year at 1.97% (+10) and 1.91% (+10) in two years. The five-year at 1.90% (+8), the 10-year at 2.29% (+5) and the 30-year at 2.98% (+5).

The ICE AAA yield curve was cut two to 11 basis points: 1.99% (+9) in 2023 and 1.90% (+11) in 2024. The five-year at 1.91% (+7), the 10-year was at 2.33% (+4) and the 30-year yield was at 2.92% (+2) at 4 p.m.

The IHS Markit municipal curve was cut four to 12 basis points: 1.95% (+12) in 2023 and 1.88% (+4) in 2024. The five-year was at 1.89% (+6), the 10-year was at 2.28% (+4) and the 30-year yield was at 2.97% (+4) at a 3 p.m. read.

Bloomberg BVAL was cut four to 11 basis points: 1.92% (+11) in 2023 and 1.90% (+9) in 2024. The five-year at 1.90% (+6), the 10-year at 2.29% (+4) and the 30-year at 2.99% (+4) at 4 p.m.

Treasuries were weaker 10 years and in.

The two-year UST was yielding 3.249 (+6), the three-year was at 3.192% (+8), the five-year at 2.956% (+6), the seven-year 2.898% (+4), the 10-year yielding 2.814% (+2), the 20-year at 3.304% (-1) and the 30-year Treasury was yielding 3.094% (-1) near the close.

Primary to come:

The Oklahoma Development Finance Authority (Aaa//AAA/) is set to price Thursday $1.354 billion of taxable ratepayer-backed Oklahoma Natural Gas Company bonds. J.P. Morgan Securities LLC.

The Regents of the University of California (Aa2/AA/AA/) is set to price on Wednesday $1.25 billion of general revenue bonds $713.23 million of exempt general revenue bonds, Series BK, $65.24 million of Series BL taxable, and $318.625 million of Series BM forward-delivery bonds. Goldman Sachs & Co. LLC

The Equitable School Revolving Fund (/A//) is set to price on Wednesday $164.455 million of national charter school revolving loan fund social revenue bonds via the Arizona Industrial Development Authority, serials 2027-2042, terms 2047, 2052. RBC Capital Markets.

Dallas County, Texas, (/AAA//) is set to price on Wednesday $150 million of certificates of obligation, serials 2023-2042. Ramirez & Co., Inc.

The Fort Worth Independent School District (Aaa///) is set to price on Wednesday $135.185 million of unlimited tax school building bonds, PSF guaranteed, serials 2023-2042, term 2047. Siebert Williams Shank & Co., LLC.

The Community Facilities District No. 2021-1 of Orange County, California, is set to price on Wednesday $118.720 million of Series A of 2022 special tax bonds. Piper Sandler & Co.

Competitive:

Minneapolis, Minnesota, (//AA+/) is set to sell $123.635 million of general obligation bonds at 11 a.m. Wednesday.

New York City (Aa2/AA/AA-/AA+) is set to sell $125 million of taxable general obligation bonds at 11:15 a.m. Wednesday.