Municipals were firmer in spots Friday, with pressure easing for short-end munis, ahead of a robust new-issue calendar where issuance tops $10 billion. U.S. Treasuries rallied out long, and equities ended up.

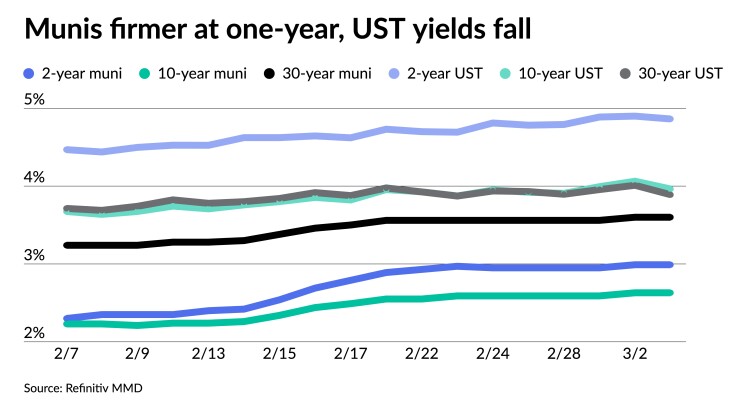

Triple-A benchmark yields were bumped three to 12 basis points, depending on the scale, at one-year, while UST yields fell four to 13, pushing the 10- and 30-year UST below 4%.

The three-year muni-UST ratio was at 61%, the five-year at 62%, the 10-year at 66% and the 30-year at 92%, according to Refinitiv MMD’s 3 p.m. ET read. ICE Data Services had the three at 62%, the five at 62%, the 10 at 65% and the 30 at 91% at 4 p.m.

Economic data “continued to put pressure on the Fed,” said Barclay strategists Mikhail Foux, Clare Pickering and Mayur Patel. “Labor costs have increased, while jobless claims remained low, and, following this week’s releases, inflation forwards have continued moving higher, getting close to the last year’s highs.”

Investors “will be watching like hawks next week’s payrolls and the [consumer price index] number the week after,” they said, noting “investors are pricing more than 20% probability of a 50bp hike in March, followed by one or two 25bp hikes.”

The macro market “continues to be under pressure as economic data and Fed rhetoric caused the futures market to raise the bet on the Fed’s terminal target rate to near 5.50%,” said BofA strategists.

“That means the market not only fully accepted three more Fed hikes but began to bet on the odds of a fourth,” they said. “The market assigns a more than 50% probability that the Fed will execute the fourth hike in July.”

UST yields are trading close to 4%. With the 10-year UST above 4%, munis may be under further pressure, the BofA strategists said. Still, they “continue to hold the view that the selloff in munis is near its end, and the market should be more constructive in March.”

“The current macro environment should subject short-end munis to more yield volatility, as economic data and Fed’s rhetoric will likely push the market around during the tax season,” the BofA strategists said. “Still, a more stable long-end Treasury yield also implies a more constructive tone for longer-term munis.”

In muniland, Barclays strategists said, “MMD-UST ratios have remained stable for most of the week although, similar to what we have seen before, when Treasury yields quickly adjusted higher mid-week, tax-exempts outperformed slightly.”

Even though the tax-exempt market is on a stable footing at the moment, they noted, “it is quite vulnerable to a correction.” It would only “need a trigger such as if rates were to continue moving higher, responding to stronger economic data, and it would happen regardless if there are fund outflows or heavier issuance,” they said.

Meanwhile, the Barclays strategists said, “outflows have resumed as expected, albeit at a relatively slow pace.”

They expect tax-exempt supply to remain relatively subdued, though “it has started to pick up, and there are a couple of large taxable deals next week.” Overall, “March is historically one of the heaviest issuance months in any given year,” and they would not be surprised “to see a pick-up in supply in the coming weeks.”

Meanwhile, they said, “the muni yield curve has also continued to flatten, the 5s10s curve is almost completely flat, and the 3s5s has already meaningfully inverted.”

The curve, they noted, “is still quite steep past the 10y point where few SMAs are able to buy bonds, and, to us, that steep part of the curve still offers pretty good value and an attractive rolldown.” However, “even the long end is finally performing, and the yield curve has started to flatten,” they said.

Moreover, the downward correction “in the SIFMA levels (by 62bp this week and by 118bp in the past two weeks) should relieve some pressure off TOBs and, as a result, off the long end,” according to the Barclays strategists.

Calendar stands at $10.3B

Investors will be greeted Monday with a new-issue calendar estimated at $10.277 billion.

There are $9.055 billion of negotiated deals on tap and $1.222 billion on the competitive calendar.

The negotiated calendar is led by $3.5 billion of taxable customer rate relief bonds from the Texas Natural Gas Securitization Finance Corp., followed by $1.8 billion of taxable various purpose GOs from the state of California and $1.2 billion of water and sewer system second general resolution revenue bonds from the New York City Municipal Water Finance Authority.

Baltimore County, Maryland leads the competitive calendar with the sale of $225 million of GOs, followed by $100 million of lease revenue bonds from the Nebo School District Local Building Authority, Utah.

The “week’s substantial primary market calendar of $10-plus billion will be a big test for where market demand stands,” Tom Kozlik, head of public policy and municipal strategy at HilltopSecurities Inc., said.

“We have not seen a calendar like this all year,” he added.

Demand for the deals could depend on how investors view the municipal market in terms of overall volume, flows, and uncertainty, Kozlik said.

Municipal benchmark yields are continuing to lag Treasury securities’ yields, he noted.

“The market is finally realizing that volume trends are going to be down this year because January and February issuance lagged 2022 so much,” he explained. “Lower issuance does not surprise me,” he continued, noting, he expects to see lower issuance for the remainder of 2023 and into 2024.

In addition, lower demand could mean continued outflows from mutual funds, Kozlik added.

“The potential for municipal investment flows to sour is rising,” he said. “I was more optimistic about the direction of flows in recent weeks, and I thought demand was going to continue to come back, but I am more skeptical now.”

Besides the market technicals, uncertainty surrounding the actions of the Federal Reserve Board are “creeping into investors’ minds again,” he said.

“Many are wondering if the Fed slowed too soon,” he said, adding, many are wondering if the Fed will raise rates 25 or 50 basis points at their upcoming meeting on March 22.

“There is a market realization that interest rates may be higher for longer, compared to where thinking began the year,” Kozlik continued.

He said there is an aura developing among some market watchers who are thinking: “why buy today what I can get at a better price tomorrow?”

Secondary trading

Maryland 5s of 2024 at 2.96%-2.92%. Washington 5s of 2024 at 2.99% versus 3.02% Thursday. NYC 5s of 2025 at 3.06%-3.02%.

Massachusetts 5s of 2029 at 2.68% versus 2.68% Thursday. California 5s of 2029 at 2.72%. NY Dorm PIT 5s of 2.82%-2.79%.

Metropolitan Water District of Southern California 5s of 2036 at 2.87%. Los Angeles Unified School District 5s of 2037 at 3.24%-3.20%. King County SD No. 403, Washington, 5s of 3.63% versus 3.58% Wednesday and 3.63% original on 2/23.

Massachusetts Transportation Fund 5s of 2052 at 4.02% versus 4.00%-3.93% on 2/23 and 4.00%-3.94% on 2/17. Massachusetts 5s of 2052 at 4.07%-4.05% versus 3.98% Tuesday and 3.70%-3.69% on 2/8.

AAA scales

Refinitiv MMD’s scale was bumped three basis points at one-year. The one-year was at 3.00% (-3) and 2.99% (unch) in two years. The five-year was at 2.68% (unch), the 10-year at 2.63% (unch) and the 30-year at 3.60% (unch) at 3 p.m.

The ICE AAA yield curve was firmer on the short end: 2.97% (-5) in 2024 and 2.96% (-3) in 2025. The five-year was at 2.70% (flat), the 10-year was at 2.65% (flat) and the 30-year yield was at 3.64% (flat) at 4 p.m.

The IHS Markit municipal curve was bumped at one-year: 3.01% (-3) in 2024 and 2.99% (unch) in 2025. The five-year was at 2.66% (unch), the 10-year was at 2.62% (unch) and the 30-year yield was at 3.62% (unch) at a 4 p.m. read.

Bloomberg BVAL was bumped 12 basis points at one-year: 3.05% (-12) in 2024 and 2.95% (-1) in 2025. The five-year at 2.66% (-1), the 10-year at 2.66% (-1) and the 30-year at 3.64% (-1).

Treasuries were firmer.

The two-year UST was yielding 4.855% (-4), the three-year was at 4.596% (-5), the five-year at 4.248% (-7), the seven-year at 4.140% (-10), the 10-year at 3.955% (-11), the 20-year at 4.105% (-13) and the 30-year Treasury was yielding 3.879% (-11) at 4 p.m.

Primary to come:

The week will kick off with a $3.5 billion sale of Series 2023 taxable customer rate relief bonds from the Texas National Gas Securitization Finance Corp. The sale, planned for Thursday by Jefferies LLC, will consist of $1.76 billion of Series A1 term bonds in 2035 and $1.76 billion of Series A2 term bonds in 2041.

That deal will be followed in size by a $1.8 billion sale of taxable various purpose general obligation bonds from California. The Wednesday sale will be senior-managed by Wells Fargo Bank Municipal Finance Group and is rated Aa2 by Moody’s Investors Service, AA-minus by S&P Global Ratings, and AA by Fitch Ratings.

The New York City Municipal Water Finance Authority, meanwhile, is slated to sell $1.24 billion of water and sewer system second general resolution revenue bonds on Wednesday. The Fiscal 2023 Series DD bonds are rated Aa1 by Moody’s and AA-plus by S&P and Fitch and are underwritten by book-runner Goldman, Sachs & Co.

The District of Columbia is planning a $826.3 million sale of GO refunding bonds on Thursday. The sale consists of $587 million in Series 1 and $239 million of Series 2 and will be senior managed by Morgan Stanley & Co. The bonds are rated Aaa by Moody’s and AA-plus by S&P and Fitch.

A $375 million sale of permanent university funds bonds is on tap from the University of Texas Board of Regents on Tuesday. The Series 2023A refunding bonds are triple-A-rated by all three major rating agencies and will be senior-managed by book-runner RBC Capital Markets.

Louisiana will bring to market $200 million of revenue refunding bonds from the Parish of St. John the Baptist on Thursday in a remarketing led by PNC Capital Markets LLC. The deal, which is rated Baa3 by Moody’s and BBB-minus by S&P and Fitch, is a remarketing of Series 2017 on behalf of the Marathon Oil Corp. project. The financing consists of sub-series 2017 A non-AMT paper which contains a term bond in 2037.

Connecticut Housing Finance Authority will market $168 million of mortgage finance program bonds in a Wednesday sale by BofA Securities. The deal — which is rated triple-A by both Moody’s and S&P — consists of Series A social bonds maturing serially from 2023 to 2035 and term bonds in 2038, 2043, 2048, and 2053.

A $153.7 million sale of auxiliary facilities system refunding revenue bonds will come to market from the Board of Trustees of the University of Illinois on Thursday. The Series 2023 bonds, which are rated Aa3 by Moody’s and AA-minus by S&P, are being senior-managed by JPMorgan Securities.

The Metropolitan Atlanta Rapid Transit Authority is scheduled to bring $150 million of sales tax revenue refunding bonds to market on Wednesday. The Series 2023 green bonds are being senior managed by Goldman, Sachs and are rated Aa2 by Moody’s and AA-plus by Standard & Poor’s and Fitch.

Competitive:

Baltimore County, Maryland, will sell $225 million triple-A-rated GO bonds Wednesday, Nebo, S.D., Local Building Authority will sell $100 million slease revenue bonds.

The Baltimore deal matures serially from 2024 to 2053, while the South Dakota deal matures serially 2024 to 2038 and is rated Aa3 by Moody’s and AA-plus by Fitch.