Munis largely ignored a U.S. Treasury sell-off as reports that some troubled banks were getting new funding helped calm investors’ concerns about a global banking crisis. Equities rallied on the news.

Triple-A benchmarks were bumped up to five basis points, depending on the scale, while UST yields rose 10 to 25 basis points 10 years and in.

The three-year muni-UST ratio was at 62%, the five-year at 63%, the 10-year at 67% and the 30-year at 93%, according to Refinitiv MMD’s 3 p.m. ET read. ICE Data Services had the three at 65%, the five at 66%, the 10 at 70% and the 30 at 94% at 4 p.m.

“Munis are holding up pretty well” in the face of the banking sector crisis, said Alice Cheng, a municipal credit analyst at Janney.

Credit is going to be the focus with the flight-to-quality situation as it will play a bigger role in investing, she said.

“At the end of the day, if I were a risk manager, I do not want to hold anything that is slightly less comforting in terms of their credit quality going down the rating scale,” Cheng said.

With the expectation the Fed may further slow of the pace of rate hikes, she said, bonds already are pricing in that expectation.

“Therefore, investors probably are going to look for credits with higher quality to avoid any unexpected debacles across any sector,” Cheng said.

Next week’s Federal Open Market Committee meeting, she said, will provide a better sense of what munis will look like in the near-term.

“When bonds are priced with the embedded interest rate in there, investors will see a turnaround with the year-to-date return going back up and it will continue to be attractive to investors,” Cheng said.

Issuance remains light as the FOMC meeting approaches and will continue to be so for the remainder of the month, she said, “until we have the solid understanding of the banks’ failures and inflation.”

“The magnitude of the rate moves in a week’s time speaks to challenged muni supply conditions as well as the push into fixed-income sectors,” said Kim Olsan, senior vice president on municipal bond trading at FHN Financial.

Although munis have “responded to the risk-off trade, the depth of the rally in the 10-year range pales” in comparison to USTs between March 8 and March 15, she said.

“The 10-year MMD yield fell 21 basis points against a 54-basis point rally in the UST (from 3.99% to 3.45%),” Olsan said.

Longer muni rates “more closely mirror their taxable counterparts, with the 30-year MMD spot falling 16 basis points against the long bond’s 25 basis point move,” she said.

Olsan noted the “10-year’s underperformance has mostly to do with ratios that opened the month in the low-60% range — about 15 percentage points through the last year’s average level.”

“The quandary of the new inquiry,” she said, “is to wait out the current rally (and risk rates falling even further if the Fed reduces or pauses the tightening cycle) or take advantage of what supply is available.”

Secondary flows suggest “a modest uptick in volume is occurring, as Wednesday’s figure surpassed $9 billion,” according to Olsan.

Specific structures “have performed better than others — short calls are still struggling for performance (Texas PSF-backed school 4s due 2033/callable 2024 traded close to 3.50% or +100/MMD) but solid demand is occurring for call-protected bonds (Washington GO 4s due 2033/callable 2031 traded at +18/MMD),” she said.

Broadly, volatility is expected to remain high into next week’s Federal Open Market Committee “meeting and as quarter-end approaches,” she said.

Current levels are still around 30 basis points away from 2023’s lows that were reached early in February.

Among the supply that priced were two high-grade state GOs.

“Sales of Maryland and Oregon state GOs defined buyer interest for large-scale issuers,” Olsan said.

“Maryland’s Aaa/AAA issue sold via a competitive bid process netted a 10-year yield [nine] basis points through the MMD spot and Oregon’s Aa1/AA+ 10-year maturity came in a negotiated pricing with the 10-year spread +14/MMD,” she said. “The 15-year maturity in the Maryland pricing was spread 19 basis points through the state’s June 2022 issue of the same maturity.”

However, Olsan noted, “the largest state issuers are not immune to the decline in the supply over the last year.”

“California’s statewide outstanding debt is $633 billion and as of February, its net issuance was barely positive at $660 million,” according to Bloomberg data.

“New York’s debt outstanding is $440 billion, but the state’s net issuance stood at negative $3.6 billion in February,” she said.

The net supply figures for both states have “led to many in-state credits commanding ultra-firm spreads. Texas — which leads all states in issuance this year by a margin of $5 billion over California — has a total of $421 billion debt outstanding across the state,” according to Olsan. The state’s “net issuance fell to negative $4.5 billion last month — a condition that is fueling a strong bid for state and local names playing into general-market inquiry,” she said.

In the primary market Thursday, Ramirez & Co. priced for institutions $309.685 million of power system revenue bonds, 2023 Series A, for the Los Angeles Department of Water and Power (Aa2//AA-/AA/), with one to four basis point bumps from Wednesday’s retail offering: 5s of 7/2023 at 2.56% (-1), 5s of 2028 at 2.37% (-1) and 5s of 2032 at 2.43% (-4), noncall.

Citigroup Global Markets priced for the State of New York Mortgage Agency (Aa1///) $150 million of social homeowner mortgage revenue bonds. The first tranche, $115.855 million of with non-AMT bonds, Series 2050, saw all bonds pricing at par: 4.3s of 10/2038, 4.65s of 2043, 4.8s of 2048 and 4.9s of 2053, callable 4/1/2032.

The second tranche, $34.145 million of AMT bonds, Series 251, saw all bonds pricing at par: 3.35s of 10/2023, 4.1s of 4/2028, 4.15s of 10/2028, 4.55s of 4/2033, 4.55s of 10/2033 and 4.7s of 4/2036, callable 4/1/2032.

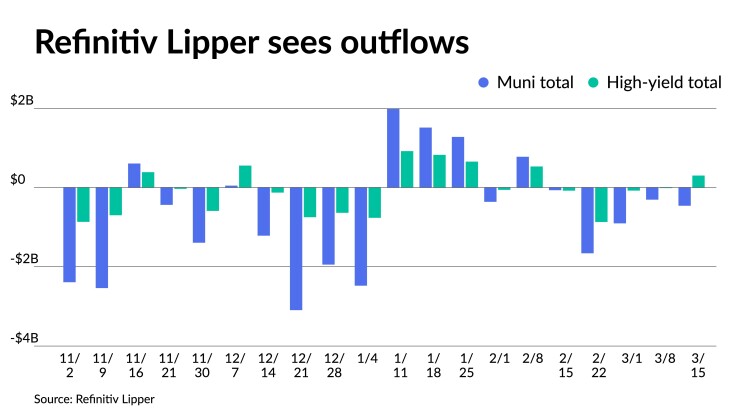

Outflows continued as Refinitiv Lipper reported $461.123 million was pulled from municipal bond mutual funds in the week that ended Wednesday after $307.815 million of outflows the week prior.

High-yield saw $300.729 million of inflows after $14.749 million of outflows the week prior, while ETFs saw outflows of $83.364 million after $50.068 million of inflows the previous week.

Secondary trading

Delaware 5s of 2024 at 2.56%-2.54%. Connecticut 5s of 2024 at 2.59%-2.58%. Triborough Bridge and Tunnel Authority 5s of 2025 at 2.69%-2.64%.

Maryland 5s of 2028 at 2.37%. Dallas County, Texas, 5s of 2029 at 2.51% versus 2.58% Wednesday. NYC TFA 5s of 2029 at 2.46%.

NY State Urban Development Corp. 5s of 2031 at 2.54%-2.53% versus 2.54% Monday. NYC Municipal Water Finance Authority 5s of 2034 at 2.64% versus 2.64% Wednesday and 2.99% original on 3/9.

University of California 5s of 2052 at 3.40%-3.64% versus 3.69%-3.68% Wednesday and 3.89% on 3/3. LA DWP 5s of 2052 at 3.68% versus 3.74%-3.73% Monday and 3.77% on 3/10.

AAA scales

Refinitiv MMD’s scale was bumped up to four basis points. The one-year was at 2.56% (-4) and 2.56% (-3) in two years. The five-year was at 2.35% (-2), the 10-year at 2.38% (-2) and the 30-year at 3.42% (unch) at 3 p.m.

The ICE AAA yield curve was bumped up to one basis point: 2.58% (-1) in 2024 and 2.58% (-1) in 2025. The five-year was at 2.37% (-1), the 10-year was at 2.43% (-1) and the 30-year yield was at 3.45% (-1) at 4 p.m.

The IHS Markit municipal curve was bumped up to five basis points: 2.58% (-5) in 2024 and 2.56% (-5) in 2025. The five-year was at 2.37% (unch), the 10-year was at 2.38% (-3) and the 30-year yield was at 3.40% (unch) at a 4 p.m. read.

Bloomberg BVAL was bumped up to two basis points: 2.63% (-2) in 2024 and 2.56% (-1) in 2025. The five-year at 2.35% (-1), the 10-year at 2.39% (unch) and the 30-year at 3.40% (unch).

Treasuries sold off.

The two-year UST was yielding 4.161% (+25), the three-year was at 3.992% (+19), the five-year at 3.772% (+16), the seven-year at 3.678% (+13), the 10-year at 3.574% (+10), the 20-year at 3.866% (+7) and the 30-year Treasury was yielding 3.706% (+4) at 4 p.m.

Mutual fund details

Refinitiv Lipper reported $461.123 million of municipal bond mutual fund outflows for the week that ended Wednesday following $307.815 million of outflows the previous week.

Exchange-traded muni funds reported outflows of $83.364 million after inflows of $50.068 million in the previous week. Ex-ETFs, muni funds saw outflows of $377.759 million after outflows of $357.883 million in the prior week.

Long-term muni bond funds had inflows of $162.139 million in the latest week after inflows of $206.540 million in the previous week. Intermediate-term funds had outflows of $171.955 million after outflows of $105.304 million in the prior week.

National funds had outflows of $440.843 million after outflows of $260.229 million the previous week while high-yield muni funds reported inflows of $300.729 million after outflows of $14.749 million the week prior.