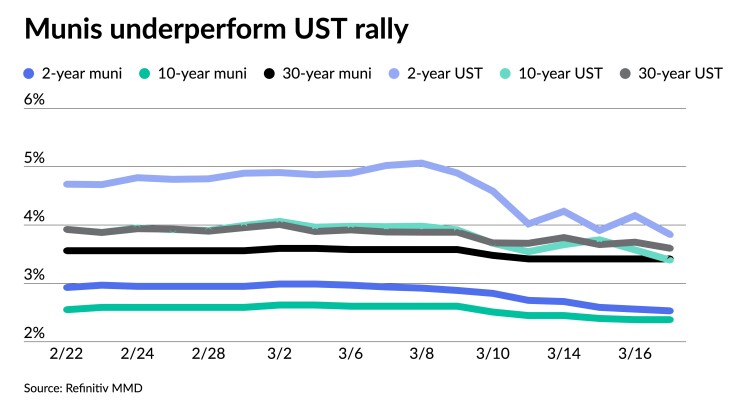

Municipals were firmer in spots to end a chaotic week that saw triple-A benchmarks both follow U.S. Treasuries in a flight to quality and ignore UST movements — as munis did on Friday for the most part — as the banking sector crisis continued. USTs rallied and equities sold off Friday.

Triple-A benchmarks were bumped up to four basis points, depending on the scale, while UST yields fell eight to 32 basis points.

The two-year muni-UST ratio was at 65%, the three-year at 65%, the five-year at 68%, the 10-year at 70% and the 30-year at 95%, according to Refinitiv MMD’s 3 p.m. ET read. ICE Data Services had the two at 60%, three at 1%, the five at 62%, the 10 at 67% and the 30 at 93% at 4 p.m.

U.S. stocks “are weakening on fears that this week’s banking turmoil will lead to tighter lending standards that will cripple small businesses and eventually send this economy into a recession,” said Edward Moya, senior market analyst for the Americas at OANDA.

The Fed’s rate hiking cycle “was already feeling restrictive, so now that we have rising risks of more bank bailouts and even tighter credit standards, the growth outlook for the economy is rather bleak,” he said.

Next week, he said, “will be huge as markets are unsure if the Fed will continue to tighten or given this week’s banking turmoil decide to hold.”

“Wall Street wants to know if the risk of a Fed policy mistake is growing and next week’s rate hiking decision and forecasts should signal if that risk is growing,” according to Moya.

“March has often not been kind to investors, and to muni investors in particular,” said Barclays strategists Mikhail Foux, Clare Pickering and Mayur Patel.

In the last four years, “there was the COVID sell-off in 2020, rates-driven volatility in 2022, and this year, a banking crisis,” they said. However, they noted, they don’t “feel that the magnitude of the current crisis is the same as the other ones, especially for our asset class.”

“This is a crisis of confidence, not asset quality, and hence easier to resolve,” the Barclays strategists said.

With economic and inflation data “printing slightly below investor expectations this week, the focus is shifting” to next week’s Federal Open Market Committee meeting, they said.

Market participants are currently “less concerned about the U.S. economy, and much more focused on the stability of banking systems in the U.S. and abroad,” according to the Barclays strategists.

Meanwhile, “investors’ rate hike outlook has been changing rather dramatically almost every day and most market participants expect the Fed to be much less aggressive going forward,” they said.

For next week, they said, “a 25 bp rate increase seems to be the most likely outcome, unless there is another bout of volatility over the weekend.”

Admittedly, they noted, “munis have withstood volatility extremely well.” Despite a significant rally in USTs, “MMD-UST ratios have barely widened, high-grade credit spreads have remained tight, and if anything, the AAA-AA spread differential has actually decreased slightly, while HY and BBBs have underperformed (even though the underperformance of BBBs is partially related to the upgrade of Illinois GOs and related Illinois credits to single-A),” they said.

Aside from lower-rated credits, Barclays strategists said, “some segments of the muni market also have come under pressure, including pre-pay gas and taxable, but mostly in sympathy with corporates, rather than due to muni-specific reasons.”

Meanwhile, they said, “the front end of the high-grade curve has caught a bid, and the yield curve has finally steepened (the 3s-long yield differential has increased by about 15 bp in just a week).”

The question remains where the market goes from here, with Barclays strategists saying, “munis and the market in general are not out of the woods as of yet.”

“However, we are getting more encouraged by the central bank and large U.S. bank response, allowing them to shore up weaker banking institutions in the U.S., while also instilling investor confidence,” they said.

They noted, “rates will likely remain volatile for now, and we also need to see proof that the U.S. economy is softening enough for the Fed to take its foot off the gas — hence, there are a lot of uncertainties ahead, and the market environment will likely remain quite challenging.”

Some parts of the muni market are “already getting cheaper, but might become even more attractive in the coming weeks,” they said. In their view, “opportunities will likely present themselves for municipal investors in the near future.”

Calendar stands at $4.1B

Investors will be greeted Monday with a new-issue calendar estimated at $4.064 billion.

There are $3.653 billion of negotiated deals on tap and $412 million on the competitive calendar.

The negotiated calendar is led by $1.5 million of taxable system restoration bonds from the Louisiana Local Government Environmental Facilities and Community Development Authority, followed by $847 million of energy supply revenue bonds from Energy Southeast.

Three River Community Schools leads the competitive calendar with $35 million of GOs.

Secondary trading

Minnesota 5s of 2024 at 2.53%-2.50%. Triborough Bridge and Tunnel Authority 5s of 2025 at 2.62%-2.59%. LA DWP 5s of 2026 at 2.40% versus 2.44% Thursday.

Maryland 5s of 2028 at 2.35% versus 2.37% Thursday. Seattle 5s of 2029 at 2.36%-2.35% versus 2.51% Tuesday. NY State Urban Development Corp. 5s of 2031 at 2.47%-2.42% versus 2.54%-2.53% Thursday and 2.54% on 3/13.

NYC Municipal Water Finance Authority 5s of 2033 at 2.57%-2.55% versus 2.85%-2.90% original on 3/9. Weber School District, Utah, 5s of 2034 at 2.58%.

NYC Municipal Water Finance Authority 5s of 2046 at 3.85% versus 3.83% Thursday and 4.02%-4.01% original on 3/9. San Jose Financing Authority 5s of 2052 at 3.53% versus 3.52%-3.51% Wednesday and 3.57% Tuesday.

AAA scales

Refinitiv MMD’s scale was bumped up to three basis points. The one-year was at 2.53% (-3) and 2.53% (-3) in two years. The five-year was at 2.35% (unch), the 10-year at 2.38% (unch) and the 30-year at 3.42% (unch) at 3 p.m.

The ICE AAA yield curve was bumped one to four basis points: 2.54% (-4) in 2024 and 2.54% (-4) in 2025. The five-year was at 2.34% (-4), the 10-year was at 2.39% (-4) and the 30-year yield was at 3.45% (-1) at 4 p.m.

The IHS Markit municipal curve was bumped up to three basis points: 2.55% (-3) in 2024 and 2.53% (-3) in 2025. The five-year was at 2.34% (-3), the 10-year was at 2.38% (unch) and the 30-year yield was at 3.40% (unch) at a 4 p.m. read.

Bloomberg BVAL was bumped up to two basis points: 2.58% (-2) in 2024 and 2.51% (-2) in 2025. The five-year at 2.33% (-2), the 10-year at 2.38% (-1) and the 30-year at 3.39% (-1).

Treasuries rallied.

The two-year UST was yielding 3.842% (-32), the three-year was at 3.712% (-28), the five-year at 3.479% (-29), the seven-year at 3.490% (-19), the 10-year at 3.426% (-15), the 20-year at 3.790% (-10) and the 30-year Treasury was yielding 3.626% (-8) at 4 p.m.

Primary to come:

The negotiated calendar is led by a $1.491 billion sale from the Louisiana Local Government Environmental Facilities and Community and Development Authority. The deal, which is rated triple-A by both Moody’s Investors Service and S&P Global Ratings, consists of system restoration bonds for the Louisiana Utilities Restoration Corp. Project/ELL. The Series 2023 taxable deal is being senior managed by J.P. Morgan Securities.

Energy Southeast, Alabama, will sell $846.880 million of energy supply revenue bonds in a two-pronged financing that is slated for pricing by Morgan Stanley & Co. Series 2023 A-1 fixed rate bonds totals $746.880 million, while Series 2023 A-2 Secured Overnight Financing Rate index bonds totals $100 million. Both series are rated A1 by Moody’s and A-plus by Fitch Ratings.

A $502.7 million sale of affordable housing revenue bonds is on tap on Tuesday from the New York State Housing Finance Agency. The Wells Fargo Bank-managed negotiated deal consists of four series of 2023 bonds rated Aa2 by Moody’s.

Series A-1 $111.200 million of climate bond certified/sustainability bonds, while Series B-1 consists of sustainability bonds totaling $34.874 million — both series maturing serially from 2024 to 2035 with terms in 2038, 2043, 2048, 2053, 2058. Series A-1 also has a 2063 term bond.

Series A-2 is $230.915 million of climate bond certified/sustainability bonds and Series B-2 consists of $125.725 million of sustainability bonds — both maturing in 2062.

A $250 million sale of solid waste disposal and sewage facilities revenue bonds is being sold by Cascade County, Montana, on Tuesday. The bonds, which are rated B-minus by S&P, are green bonds for the Montana Renewables LLC project and are being senior managed by Citigroup Global Markets.

Birmingham Public Schools in Oakland County, Michigan, plan to sell $117.5 million sale of school building and site and refunding bonds backed by unlimited tax general obligation bonds.

The refunding is rated AA-plus by S&P and will be structured as serial bonds maturing from 2024 to 2043. The bonds will be priced by bookrunner Stifel, Nicolaus & Co.

There are no competitive sales of $100 million or larger planned for the week.