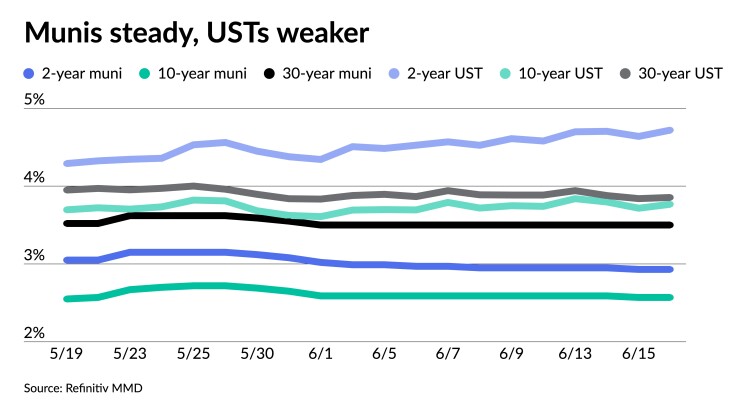

Municipals were steady to end the week, continuing their outperformance of U.S. Treasuries. Equities were down near the close.

Triple-A scales were little changed, while UST yields rose eight to nine basis points on the short end.

The two-year muni-Treasury ratio Friday was at 62%, the three-year at 65%, the five-year at 66%, the 10-year at 68% and the 30-year at 91%, according to Refinitiv MMD’s 3 p.m. read. ICE Data Services had the two-year at 64%, the three-year at 66%, the five-year at 66%, the 10-year at 69% and the 30-year at 92% at 3:45 p.m.

Lower issuance this month is keeping things steady but not allowing for much price discovery. Bond Buyer 30-day visible supply sits at $9.56 billion.

The primary again is on the lighter side led by New York issuers with two sustainable affordable housing deals from the city and the state as well as a New York City water deal via the State Environmental Facilities Corp. The competitive calendar has only one deal at $100 million or more.

Economic indicators and the Fed’s pause on rates hikes this week led to a mixed U.S. Treasury market. Tuesday’s consumer price index “was largely in line with investor expectations (with the exception of the upside surprise for used car prices, although they will likely decline in the near future), and it came as little surprise that the Fed decided not to hike rates this month,” said Barclays strategists Mikhail Foux, Clare Pickering and Mayur Patel.

However, they noted the Fed is not likely done hiking rates, and Wednesday’s announcement ”could be described as a hawkish pause, after the FOMC reinforced its determination to continue to raise rates if needed.”

Currently, fed fund futures project “just one rate hike in July or September, while the median dot plot implies two 25bp rate increases this year, which would bring the target rate to 5.5%-5.75%,” they said.

This would mean “a 50bp increase of target rate policymaker expectations compared with March,” according to Barclays strategists.

In the aftermath of the FOMC meeting, Barclays strategists continue to expect the Fed to hike rates 25 basis points in July and another 25 basis points in September. They expect policymakers to pause after that through the second quarter of 2024.

For next year, they “revised the rate path slightly to reflect cuts starting in June, as opposed to May.”

As the market had already priced in the Fed’s pause, there was not much of a “reaction in the Treasury market (with the exception of the front- end of the curve),” they said. Long-dated yields were slightly lower on the week, they noted.

“Munis continue to perform well in June, as expected: [Refinitiv] MMD ratios have declined 1-3pp across the curve, and index returns this month have continued to inch higher,” Barclays strategists said.

Market technicals are still supportive, “as issuance is still very slow (we actually downgraded our 2023 supply forecast); fund cash balances are sizable; dealers are not overly heavy (although their 5-10y bond balances are higher than earlier this year) and large outflows have stopped, especially for long-dated bonds, where we still see the most value,” according to Barclays.

The 10s30s index yield curve, which is at its flattest point this year, “is still about 15bp steeper than the recent lows reached in October,” they said. However, they think it might flatten further.

Barclays strategists expect lower-rated high-grade munis ”to continue to gain ground this summer after underperforming the IG index by 20bp for single As and by 55bp for BBBs since the start of the hiking cycle.”

So far this year, “spreads of these rating buckets are 4-6bp tighter versus the index, but are still quite cheap in a historical context,” they said.

However, due to elevated rates, they said “lower-rated credit spreads represent a smaller share of the total yield.”

This would mean “that spreads are unlikely to get to their pre-sell-off levels unless yields adjust much lower,” but Barclays strategists still “see enough value in lower-rated high-grade sectors, which should support them in the near term.”

Calendar stands at $5B

For the coming week, investors will be greeted with a new-issue calendar estimated at $5.031 billion.

There are $3.912 billion of negotiated deals on tap and $1.119 billion on the competitive calendar.

The negotiated calendar is led by $320 million of sustainable development housing impact bonds from the New York City Housing Development Corp., followed by $307.4 million of sustainable affordable housing revenue bonds from the New York State Housing Finance Authority and $306.9 million of State Clean Water and Drinking Water Revolving Funds revenue bonds from the New York State Environmental Facilities Corp.

The competitive calendar is light with only Putman County School District, Florida, with $100 million of GOs selling Wednesday.

Secondary trading

Tempe, Arizona, 5s of 2024 at 3.13%-3.16%. DC 5s of 2025 at 2.97% versus 3.04% on 6/6. Maryland 5s of 2026 at 2.80% versus 2.84% on 6/12 and 2.83% 0n 6/5.

Maryland 5s of 2028 at 2.68% versus 2.70% Wednesday. Connecticut 5s of 2028 at 2.80%-2.78%. DASNY 5s of 2029 at 2.71% versus 2.75% on 6/7.

NYC 5s of 2032 at 2.80% versus 2.84% Wednesday and 2.86%-2.85% Tuesday. Raleigh Combined Enterprise System, North Carolina, 5s of 2034 at 2.72%-2.70% versus 2.73% on 6/6 and 2.80% original on 6/2. DC 5s of 2035 at 2.73%.

California 5s of 2045 at 3.42%-3.40% versus 3.43% Thursday. Indiana Finance Authority 5s of 2053 at 4.07% versus 4.10%-4.09% Thursday and 4.14% Wednesday.

AAA scales

Refinitiv MMD’s scale was unchanged: The one-year was at 3.07% and 2.93% in two years. The five-year was at 2.64%, the 10-year at 2.57% and the 30-year at 3.50% at 3 p.m.

The ICE AAA yield curve was flat: 3.10% in 2024 and 2.98% in 2025. The five-year was at 2.62%, the 10-year was at 2.57% and the 30-year was at 3.54% at 3:45 p.m.

The IHS Markit municipal curve was unchanged: 3.06% in 2024 and 2.93% in 2025. The five-year was at 2.64%, the 10-year was at 2.56% and the 30-year yield was at 3.49%, according to a 3 p.m. read.

Bloomberg BVAL was little changed: 3.02% (unch) in 2024 and 2.92% (unch) in 2025. The five-year at 2.61% (unch), the 10-year at 2.55% (unch) and the 30-year at 3.53% (unch) at 3:45 p.m.

Treasuries were weaker.

The two-year UST was yielding 4.717% (+8), the three-year was at 4.321% (+9), the five-year at 3.989% (+8), the 10-year at 3.765% (+5), the 20-year at 4.044% (+3) and the 30-year Treasury was yielding 3.853% (+2) at 3:45 p.m.

Primary to come:

The New York City Housing Development Corp. (Aa2///) is set to price Thursday $320.305 million of housing impact sustainable development bonds, consisting of $$290.725 million of tax-exempts, 2023 Series A, terms 2043, 2048, 2053, and $29.580 million of taxables, 2023 Series B, serials 2027-2033, term 2039. Jefferies.

The New York State Housing Finance Agency (Aa2///) is set to price Thursday $307.405 million of affordable housing revenue sustainability bonds, consisting of $88.890 million of Series 2023 C-1, and $218.515 million of Series C-2. Morgan Stanley.

The New York State Environmental Facilities Corp. (Aaa/AAA/AAA/) is set to price Wednesday on behalf of the New York City Municipal Water Finance Authority Projects $306.945 million of second resolution State Clean Water and Drinking Water Revolving Funds refunding revenue bonds, Series 2023 B, serials 2024-2043, terms 2048, 2053. Citigroup Global Markets.

The Highline School District No. 401, Washington, (Aaa///) is set to price Wednesday $254.435 million in unlimited tax GOs, Series 2023, insured by the Washington State School District Credit Enhancement Program. Piper Sandler & Co.

The Harris County Flood Control District, Texas, (Aaa/AAA//) is set to price Wednesday $225 million in improvement refunding sustainability bonds, Series 2023A. Mesirow Financial.

The Massachusetts Development Finance Authority (Aa3/AA-//) is set to price Wednesday $224.070 million of Boston University Issue refunding revenue bonds, consisting of $173.175 million of Series FF, serials 2024-2031, 2033, term 2048, and $50.895 million of Series GG, term 2042. BofA Securities.

The Pennsylvania State University (Aa1/AA//) is set to price Wednesday $208.735 million of Series 2023, serials 2024-2043, terms 2048, 2053. Barclays.

Lansing, Michigan, (/A+//AA-) is set to price Wednesday $163.960 million of capital improvement and refunding unlimited tax GOs, Series 2023B, serials 2024-2043, terms 2048, 2053. Ramirez & Co.

The Village Community Development District No. 15, Florida, is set to price Wednesday $155.490 million of special assessment revenue bonds, Series 2023, terms 2028, 2033, 2038, 2043, 2054. Jefferies.

The National Finance Authority, Nevada, (/AA//) is set to price Thursday $149.550 of Build America Mutual-insured lease revenue bonds, consisting of $148.950 million of Series 2023A, serials 2023-2036, terms 2037, 2038, 2039, 2040, 2041, 2042, 2043, 2048, 2053, and $600,000 of taxables, Series 2023B, serial 2024, Wells Fargo Bank.

Forsyth, Montana, ( A3//A-/) is set to price Thursday on behalf of the Northwestern Corp. Conlstrip Project $144.660 million of pollution control revenue refunding bonds, Series 2023, serial 2028. BofA Securities.

Texas (/AAA/AAA/) is set to price Wednesday $127.935 million of general obligation water financial assistance bonds, consisting of $22.170 million of new-issue bonds, Series 2023A, serials 2024-2048, $36.470 million of refunding bonds, Series 2023B, serials 2024-2033, and $69.295 million of new-issue bonds, Series 2023C, serials 2023-2042. Siebert Williams Shank & Co.

The Kern Community College District, California, (Aa2/AA-//) is set to price Wednesday $127.365 million of Election of 2016 GOs, Series E, serials 2024-2040. Stifel, Nicolaus & Co.

Essex County is set to price Wednesday $120 million of guaranteed lease revenue project notes. Morgan Stanley.

Competitive

The Putnam County School District, Florida (A2//A+/) is set to sell $100 million of GO school bonds, Series 2023 at 11 a.m. eastern Wednesday.