Municipals showed some strength Tuesday, U.S. Treasury yields fell and equities ended down.

Triple-A scales bumped up to five basis points, depending on the scale, while UST yields fell three to five basis points.

The two-year muni-to-Treasury ratio Tuesday was at 62%, the three-year at 65%, the five-year at 66%, the 10-year at 68% and the 30-year at 91%, according to Refinitiv MMD’s 3 p.m. read. ICE Data Services had the two-year at 63%, the three-year at 65%, the five-year at 64%, the 10-year at 68% and the 30-year at 91% at 4 p.m.

While the muni market was firmer Tuesday, last week was “once again unfazed by the macro events and interest rate volatility,” said Birch Creek strategists.

Due to the Fed-induced lighter new-issue calendar last week, and a holiday-shortened week this week, they said, “buyers had no qualms about putting cash to work.”

Despite “the rate selloff for the past two weeks, the benchmark AAA curve went nine straight days without any yield changes,” they noted.

Triple-A benchmarks between two- and 17-years were up to two basis points firmer Thursday, “bringing the streak up to 11 days for long duration bonds,” according to Birch Creek strategists.

They noted the Federal Deposit Insurance Corp. sale lists, which were around $325 million to $350 million per day Monday through Thursday were the main source of supply for the market. “Given the concentration of the portfolio’s maturities in the 10- to 18-year tenors, this has led to a surge in trade activity in the belly of the curve,” they said.

“With the Fed taking a hawkish pause on raising rates this past Wednesday, many fear that the Fed could potentially hike rates two more times this year, which left munis relatively unchanged as munis yields across the curve only bumped by an average of just 1.4 basis points,” said Jason Wong, vice president of municipals at AmeriVet Securities.

The Fed pause, he noted, “is something the muni market has been waiting for as the bumps in yields pushed June’s return to 0.72% with the year-to-date return at 2.38%.”

Before the Fed’s announcement, Wong said, “June returns were at 0.56%, with a year-to-date return of 2.23%.”

This pause, he noted, will “start to shed some light in the markets as investors will start to flock to tax-exempts.”

Before the FOMC’s announcement it would skip a rate hike at its June meeting, Birch Creek strategists said, “traders were reporting strong demand for bonds with ‘structure’ — mainly 3% coupons at discounts and longer duration bonds with two- to four-year call dates.”

After the meeting, they said, “the inquiry expanded as many buyers came off the sidelines as they felt they had a clearer picture of interest rates in the short term.”

Despite inflows two weeks ago for the first time in 16 weeks, outflows returned last week. Refinitiv Lipper reported $257 million of money was pulled from muni mutual funds after $460 million of inflows the week prior.

“Although we are slowly starting to see some stability in the muni market, it still may take some time for investors to have more confidence,” Wong said.

However, JPMorgan reported long-term funds saw inflows of $259 million for the week, bringing the total up to around $4 billion for the year.

Birch Creek strategists “expect that longer duration bonds, both treasuries and munis, should continue to perform well as the Fed remains committed to their inflation fight.”

On the muni side, they said, “while valuations are historically rich across the curve, the 30 year is the most attractive,” trading at around 91% of USTs.

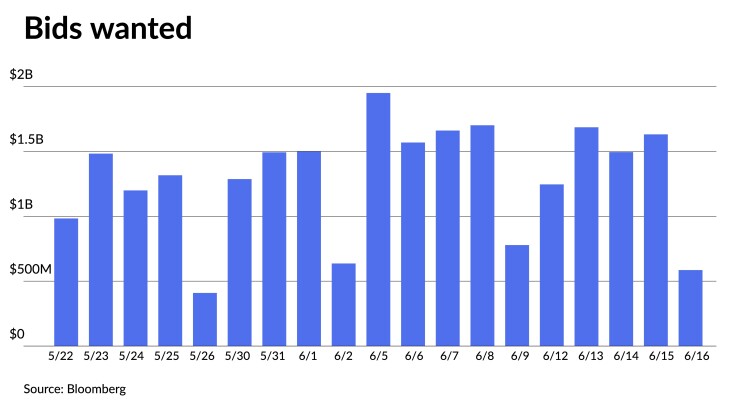

Secondary trading for the week was around “$38.9 billion with roughly 52% of trading being dealer sells and with the bulk of the trading being done on Wednesday, with Friday having the lightest trading volume,” said Wong.

Clients put up around $7.88 billion for the bid last week versus the $7.65 billion put up for bid the week prior, he said.

Secondary trading

Washington 5s of 2024 at 3.10% versus 3.14% on 6/5. Massachusetts 5s of 2024 at 3.09%-3.03%. New York City 5s of 2025 at 3.09%.

Triborough Bridge and Tunnel Authority 5s of 2028 at 2.67%-2.65%. Fairfax County Water Authority, Virginia, 5s of 2029 at 2.66%-2.63% versus 2.65% on 6/12. Georgia 5s of 2030 at 2.60% versus 2.59% on 6/7.

Wisconsin 5s of 2032 at 2.65% versus 2.66% on 6/14 and 2.69% on 6/9. Board of Regents of the University of Texas System 5s of 2034 at 2.74% versus 2.85% on 6/12 and 2.85%-2.90% original on 6/7. Los Angeles Department of Water and Power 5s of 2035 at 2.61%.

California 5s of 2045 at 3.40% versus 3.42%-3.40% Friday and 3.43% Thursday. Texas Water Development Board 5s of 2047 at 3.65%-3.62% versus 3.68%-3.69% on 6/1. Massachusetts 5s of 2052 at 3.75% versus 3.82% on 6/13.

AAA scales

Refinitiv MMD’s scale was bumped two to four basis points: The one-year was at 3.03% (-4) and 2.91% (-2) in two years. The five-year was at 2.62% (-2), the 10-year at 2.55% (-2) and the 30-year at 3.48% (-2) at 3 p.m.

The ICE AAA yield curve was bumped up to five basis points: 3.05% (-5) in 2024 and 2.96% (-2) in 2025. The five-year was at 2.61% (-2), the 10-year was at 2.56% (-1) and the 30-year was at 3.52% (-2) at 4 p.m.

The IHS Markit municipal curve was bumped one to three basis points: 3.03% (-3) in 2024 and 2.92% (-1) in 2025. The five-year was at 2.63% (-1), the 10-year was at 2.55% (-1) and the 30-year yield was at 3.48% (-1), according to a 4 p.m. read.

Bloomberg BVAL was bumped two to three basis points: 2.99% (-3) in 2024 and 2.90% (-2) in 2025. The five-year at 2.59% (-2), the 10-year at 2.53% (-2) and the 30-year at 3.50% (-2) at 4 p.m.

Treasuries were firmer.

The two-year UST was yielding 4.692% (-3), the three-year was at 4.287% (-3), the five-year at 3.954% (-4), the 10-year at 3.724% (-4), the 20-year at 3.996% (-5) and the 30-year Treasury was yielding 3.811% (-4) at 4 p.m.

Primary to come:

The New York City Housing Development Corp. (Aa2///) is set to price Thursday $320.305 million of housing impact sustainable development bonds, consisting of $$290.725 million of tax-exempts, 2023 Series A, terms 2043, 2048, 2053, and $29.580 million of taxables, 2023 Series B, serials 2027-2033, term 2039. Jefferies.

The New York State Housing Finance Agency (Aa2///) is set to price Thursday $307.405 million of affordable housing revenue sustainability bonds, consisting of $88.890 million of Series 2023 C-1, and $218.515 million of Series C-2. Morgan Stanley.

The New York State Environmental Facilities Corp. (Aaa/AAA/AAA/) is set to price Wednesday on behalf of the New York City Municipal Water Finance Authority Projects $306.945 million of second resolution State Clean Water and Drinking Water Revolving Funds refunding revenue bonds, Series 2023 B, serials 2024-2043, terms 2048, 2053. Citigroup Global Markets.

The Highline School District No. 401, Washington, (Aaa///) is set to price Wednesday $254.435 million in unlimited tax GOs, Series 2023, insured by the Washington State School District Credit Enhancement Program. Piper Sandler & Co.

The Harris County Flood Control District, Texas, (Aaa/AAA//) is set to price Wednesday $225 million in improvement refunding sustainability bonds, Series 2023A. Mesirow Financial.

The Massachusetts Development Finance Authority (Aa3/AA-//) is set to price Wednesday $224.070 million of Boston University Issue refunding revenue bonds, consisting of $173.175 million of Series FF, serials 2024-2031, 2033, term 2048, and $50.895 million of Series GG, term 2042. BofA Securities.

The Pennsylvania State University (Aa1/AA//) is set to price Wednesday $208.735 million of Series 2023, serials 2024-2043, terms 2048, 2053. Barclays.

Lansing, Michigan, (/A+//AA-) is set to price Wednesday $163.960 million of capital improvement and refunding unlimited tax GOs, Series 2023B, serials 2024-2043, terms 2048, 2053. Ramirez & Co.

The Village Community Development District No. 15, Florida, is set to price Wednesday $155.490 million of special assessment revenue bonds, Series 2023, terms 2028, 2033, 2038, 2043, 2054. Jefferies.

The National Finance Authority, Nevada, (/AA//) is set to price Thursday $149.550 of Build America Mutual-insured lease revenue bonds, consisting of $148.950 million of Series 2023A, serials 2023-2036, terms 2037, 2038, 2039, 2040, 2041, 2042, 2043, 2048, 2053, and $600,000 of taxables, Series 2023B, serial 2024, Wells Fargo Bank.

Forsyth, Montana, (A3//A-/) is set to price Thursday on behalf of the Northwestern Corp. Constrip Project $144.660 million of pollution control revenue refunding bonds, Series 2023, serial 2028. BofA Securities.

Texas (/AAA/AAA/) is set to price Wednesday $127.935 million of general obligation water financial assistance bonds, consisting of $22.170 million of new-issue bonds, Series 2023A, serials 2024-2048, $36.470 million of refunding bonds, Series 2023B, serials 2024-2033, and $69.295 million of new-issue bonds, Series 2023C, serials 2023-2042. Siebert Williams Shank & Co.

The Kern Community College District, California, (Aa2/AA-//) is set to price Wednesday $127.365 million of Election of 2016 GOs, Series E, serials 2024-2040. Stifel, Nicolaus & Co.

Essex County is set to price Wednesday $120 million of guaranteed lease revenue project notes. Morgan Stanley.

Competitive

The Putnam County School District, Florida (A2//A+/) is set to sell $100 million of GO school bonds, Series 2023 at 11 a.m. eastern Wednesday.