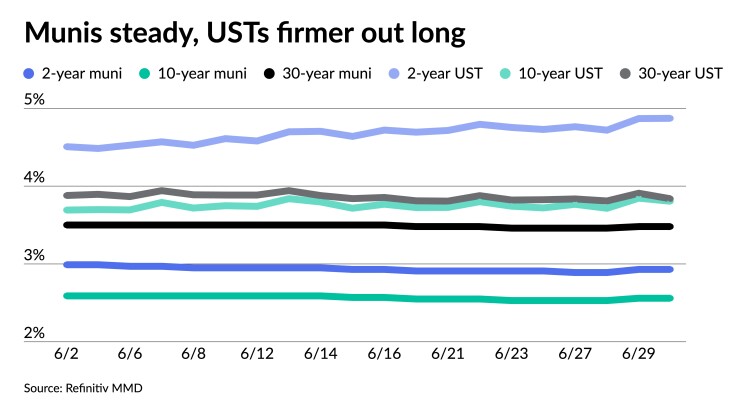

Municipals were steady to end the month and first half of the year ahead of a paltry new-issue calendar which will see next week’s volume drop to the lowest level of 2023. U.S. Treasuries were firmer out long and equities rallied.

Treasuries saw yields fall by as much as seven basis points on the long bond Friday and municipals were little changed ahead of the holiday-shortened week.

Treasuries were relatively stable until Thursday, when they sold off aggressively. While munis lost ground Thursday, they outperformed leading to lower muni-to-UST ratios.

The two-year muni-to-Treasury ratio Friday was at 60%, the three-year at 62%, the five-year at 64%, the 10-year at 67% and the 30-year at 91%, according to Refinitiv MMD’s 3 p.m. read. ICE Data Services had the two-year at 60%, the three-year at 63%, the five-year at 62%, the 10-year at 67% and the 30-year at 91% at 4 p.m.

Markets started to realize this week that the Fed is likely to hike interest rates again, according to a Barclays PLC report, noting that Fed Chair Jerome Powell warned of at least two interest-rate increases this year to lower the inflation rate. The dot plot currently has the Fed hiking rates another 50 basis points this year.

The stronger U.S. economic data — housing is showing signs of strength, unemployment claims were lower than expected, and the first quarter’s GDP has been revised upward from 1.4% to 2% — led to a spike in UST yields, which munis could not ignore.

But June has been a “solid” month for the asset class, Barclays noted.

The Bloomberg Municipal Index is at positive 1.01% for June and 2.68% year-to-date. Taxable munis are returning negative 0.58% month-to-date and 4.36% in 2023. High-yield returns are in the black at 1.78% for June and 4.44% year-to-date.

“Technicals are still very supportive,” Barclays wrote, “as issuance remains below average, fund outflows have likely stopped, and heavy summer bond redemptions are putting more money into investor hands.”

June issuance sat at $34.436 billion. This is the highest monthly volume for 2023, but issuance is still down 9% year-over-year.

Issuance for the first half of the year is $174.768 billion, down 20% year-over-year.

Calendar stands at $305M

For the coming week, investors will be greeted with a new-issue calendar estimated at $304.5 million. This marks the lowest week of issuance in 2023.

There are $249.4 million of negotiated deals on tap and $55.1 million on the competitive calendar.

The negotiated calendar is led by $110 million of PSF-insured unlimited tax schoolhouse bonds from the Dickinson Independent School District, Texas, and $100 million of single-family mortgage revenue bonds from the Mississippi Home Corp.

The Dallas Housing Finance Corp. is set to price two deals daily — $146.608 million of Fitzhugh Urban Flats social residential development revenue bonds and $120.300 million of Midtown Park residential development revenue bonds.

There are no competitive deals over $100 million. The largest deal for the week is $91 million of unlimited tax GO school bond anticipation notes from the Nauset Regional School District, Massachusetts.

1H recap

“We came into the new year with the Fed in a pivot mode,” noted BofA strategists in a mid-year report.

Market participants had “expected the Fed to complete its tightening program with two more 25bp rate hikes by March,” while “most economists expected a modest recession to begin in 2Q23,” they said.

Neither of those expectations came to fruition.

“Despite several regional bank failures in March, the Fed did three 25bp rate hikes by May and communicated only a ‘skip’ at the June FOMC meeting,” they said.

It is likely the Fed will hike rates further, possibly several times, “based on a surprisingly-resilient labor market, solid GDP growth and a slower-than-expected decline of inflation,” BofA strategists said.

The muni market rates rally in the 1H23 “turned out to be strong, but more volatile than we anticipated at the end of last year,” they said.

Nearly all of the rally was finished by January, “building on the strong momentum from the final two months of 2022,” they said.

The 10-year muni AAA rates fell “through our original yearly target of 2.20%, but could not hit our revised and more aggressive target of 2.00% for 1H23,” according to BofA strategists.

They attribute this failure to “the surprising resurgence of the Fed after successfully managing regional bank failures.”

Barclays strategists had also been cautious on the failed banks liquidating their muni portfolios and the market’s responses to it. But they noted that demand for low-coupon munis has been solid and “prices did not correct much” as a result of the influx of low-coupon debt from the Federal Deposit Insurance Corp. lists.

Low-coupon bonds “generally do not work well for retail investors due to their negative tax consequences,” Barclays noted, but they are “a relatively good fit for institutional investors.”

“When these bank portfolios are fully liquidated, some crossover investors should be able to continue finding good value in low-coupon, high-quality securities as they trade cheap enough to their high-coupon counterparts,” Barclays wrote.

Muni credit spreads were reasonably wide at the start of the year “as the market traded on recession expectations for 2Q23, BofA strategists said.

Spreads narrowed thanks to the strong January rates rally, but they said, “when the regional bank problem came to the fore, muni credit spreads widened significantly.”

By now, they said, “almost all of that widening retraced, and all index credit spreads are narrower now than at the beginning of the year.”

BofA strategists predicted “credit spreads would end the year more-or-less unchanged,” and they do not plan to revise their forecast.

“The risk of much narrower spreads would come from inflation falling faster in 2H23, the Fed ending its tightening program and the economy avoiding a recession,” they said. “The risk of much wider credit spreads would come from the economy entering a recession earlier than what the market currently prices in.”

Secondary trading

Massachusetts 5s of 2024 at 3.06% versus 3.04% Wednesday. LA County Metropolitan Transportation Authority 5s of 2025 at 2.86%. Maryland 5s of 2026 at 2.86%-2.82%.

Georgia 5s of 2028 at 2.62%. West Virginia 5s of 2028 at 2.71%. Maine 5s of 2030 at 2.66%-2.61%.

Wisconsin 5s of 2032 at 2.62% versus 2.64% Thursday and 2.65% on 6/20. California 5s of 2034 at 2.73% versus 2.67% on 6/22. Charleston waters, South Carolina, 5s of 2036 at 2.87%-2.88% versus 2.90% Thursday.

Massachusetts 5s of 2052 at 3.84% versus 3.67%-3.55% on 6/23 and 3.75% on 6/21. Indiana Finance Authority 5s of 2053 at 4.06% versus 4.09% Thursday and 4.05% on 6/21.

AAA scales

Refinitiv MMD’s scale was unchanged: The one-year was at 3.05% and 2.93% in two years. The five-year was at 2.62%, the 10-year at 2.56% and the 30-year at 3.49% at 3 p.m.

The ICE AAA yield curve was mixed: 3.02% (+2) in 2024 and 2.96% (+1) in 2025. The five-year was at 2.61% (+1), the 10-year was at 2.57% (-1) and the 30-year was at 3.54% (-1) at 4 p.m.

The IHS Markit municipal curve was unchanged: 3.05% in 2024 and 2.93% in 2025. The five-year was at 2.62%, the 10-year was at 2.56% and the 30-year yield was at 3.49%, according to a 3 p.m. read.

Bloomberg BVAL was little changed: 2.99% (unch) in 2024 and 2.90% (unch) in 2025. The five-year at 2.59% (unch), the 10-year at 2.53% (unch) and the 30-year at 3.50% (unch) at 4 p.m.

Treasuries were firmer out long.

The two-year UST was yielding 4.870% (flat), the three-year was at 4.497% (flat), the five-year at 4.120% (-1), the 10-year at 3.805% (-4), the 20-year at 4.050% (-6) and the 30-year Treasury was yielding 3.837% (-7) near the close.

Primary to come:

The Dallas Housing Finance Corp. is set to price daily $146.608 million of Fitzhugh Urban Flats social residential development revenue bonds, consisting of $71.985 million of senior lien bonds, Series 2023-A1; serial 2063, $55.115 of senior lien bonds, Series 2023-A2, serial 2063; and $19.508 million of convertible capital appreciation mezzanine lien bonds, Series 2023B, serial 2063. Citigroup Global Markets.

The corporation is also set to price daily $120.300 million of Midtown Park residential development revenue bonds, consisting of $89 million of Series 2023A and $31.300 million of Series 2023B. Goldman Sachs.

The Dickinson Independent School District, Texas (Aaa/AAA//), is set to price Thursday $110.005 million of PSF-insured unlimited tax schoolhouse bonds, Series 2023, serials 2025-2053. Wells Fargo Bank.

The Mississippi Home Corp. (Aaa///) is set to price Thursday $99.850 million of single-family mortgage revenue bonds, consisting of $70 million of non-AMT bonds, Series 2023C, serials 2028-2035, terms 2038. 2043, 2048; and $29.850 million of taxables, Series 2023D, serials 2024-2028, term 2053. Raymond James & Associates.

The Montana Board of Housing (Aa1/AA+//) is set to price Thursday $32 million of non-AMT single-family mortgage bonds, 2023 Series A, serials 2024-2035, terms 2038, 2043, 2048, 2053, 2053. RBC Capital Markets.

Competitive

The Nauset Regional School District, Massachusetts, is set to sell $91 million of unlimited tax GO school bond anticipation notes at 11 a.m. eastern Thursday.

The Fairport Central School District, New York, is set to sell $48.165 million of GO bond anticipation notes, Series 2023, at 11:15 a.m. Thursday.

Jersey City, New Jersey, is set to sell $45.926 million of taxable COVID-19 special emergency notes, Series 2023B, at 11:15 a.m. Thursday.

East Brunswick Township, New Jersey, is set to sell $45.360 million of bond anticipation notes, consisting of $26.760 million of bond anticipation notes and $18.600 water utility bond anticipation notes, at 11:30 a.m. Thursday.

Somerset County, New Jersey, is set to sell $38.962 of GOs, consisting of $35 million of general improvement bonds, Series 2023A; $1.966 million of county college bonds, Series 2023B; and $1.966 county college bonds, Series 2023C, at 11 a.m. Thursday.

The Guilderland Central School District, New York, is set to sell $29.499 million of bond anticipation notes at 10:30 a.m. Thursday.