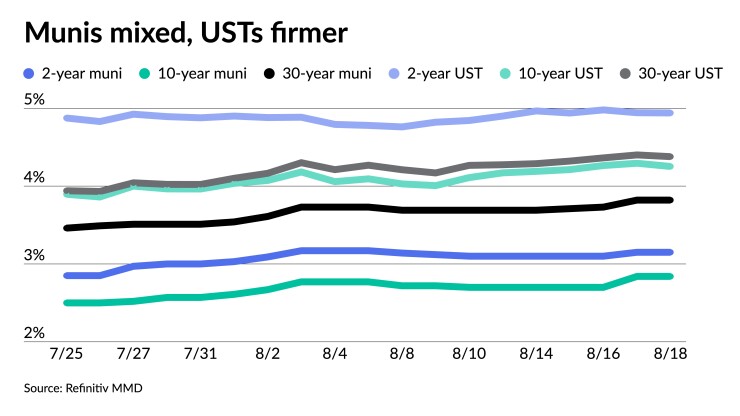

Municipals were mixed Friday while U.S. Treasuries made gains on global concerns over higher interest rates and the hopes for a soft landing fading. Equities sold off.

“For those hoping things will be quiet on the [Federal Open Market Committee], or Fed front they can think again,” said Tom Kozlik, head of public policy and municipal strategy at Hilltop Securities Inc., adding that the Jackson Hole Symposium kicks off on Thursday and the market will be “reading the tea leaves and interested in anything said or even implied there.”

Triple-A yields were cut up to three basis points Friday, depending on the scale, while UST yields fell up to four basis points.

The two-year muni-to-Treasury ratio Friday was at 64%, the three-year at 64%, the five-year at 65%, the 10-year at 67% and the 30-year at 87%, according to Refinitiv MMD’s 3 p.m. read. ICE Data Services had the two-year at 64%, the three-year at 65%, the five-year at 64%, the 10-year at 65% and the 30-year at 87% at 4 p.m.

Despite tight municipal ratios, investor demand is still evident in the current market environment, Kozlik said.

“The force of that demand is better than last year at this time, but still delicate,” he said Friday.

Fed fears are tainting the market activity to an extent, he said.

“Volatilities of both rates and risk assets are on the rise,” BofA Global Research said in a Friday report. “Bearish Treasury moves have kept some pressure on the muni market and prevented an attempt to rally during the summer season when large redemptions trump issuance.”

At this point, low muni/Treasury ratios and stable muni rate volatilities “have kept muni price declines much more muted than Treasuries, but for the next several weeks given the bearish outlook of Treasuries and a hawkish Fed, we believe muni investors should employ some hedging here as the risk of significantly higher Treasury yields are quite real.”

Also, they said, the accelerated economy “suggests a steeper Treasury yield curve to come, so hedging with longer maturity Treasuries should be employed.”

While munis have been moving in sync with the rise in Treasury yields, “they finally started to underperform on Thursday,” Barclays PLC strategists wrote in a Friday report. “From a total return perspective, all fixed income asset classes have performed pretty poorly this month, but tax-exempts have actually done better than most other fixed income assets, although they were not immune from the rate selloff.”

Barclays said they remain cautious for August and early September.

“Supply will remain surprisingly resilient at the end of the month and, in the current poor liquidity environment this may put more pressure on the secondary market,” they said. “In the near term, we believe that tax-exempts might underperform Treasuries, even though outright municipal yields are becoming extremely attractive, which should drum up interest from direct retail and other investor groups.”

For munis, this August “will likely end up in the red, making it the fourth year in a row when investors lose money in the month,” they added.

The Bloomberg Municipal Index has seen negative returns of 1.40% in August, bringing year-to-date returns to positive 1.63%. High-yield returns are negative 1.79% so far this month and year-to-date positive 3.24% while taxable municipals have lost 2.25% in August and but gained 1.94% in 2023.

New-issue calendar

The calendar is estimated at $7.304 billion next week with $5.896 billion of negotiated deals on tap and $1.407 billion on the competitive calendar.

The largest two deals of the week, $1.182 billion of Michigan State Trunk Line Fund Rebuilding Michigan Program bonds and $1 billion of future tax-secured subordinate bonds for the New York City Transitional Finance Authority, are liquid names and should provide some price discovery.

The competitive calendar is led by much smaller deals from Hennepin County, Minnesota, and Rosemount-Apple Valley ISD, Minnesota, along with a courthouse bond deal from Smith County, Texas.

Secondary trading

North Carolina 5s of 2024 at 3.28% versus 3.30% Thursday. NYC 5s of 2024 at 3.22%-3.20%. California 5s of 2024 at 2.98%-2.97% versus 3.00% Wednesday and 3.01%-2.98% Monday.

Cambridge, Massachusetts, 5s of 2028 at 2.75%-2.74%. Connecticut 5s of 2028 at 2.97% versus 2.86% on 8/8. NYC 5s of 2030 at 3.16% versus 2.87% on 8/10.

Washington 5s of 2032 at 2.93% versus 2.81%-2.78% Monday. Massachusetts 5s of 2034 at 2.97%. Connecticut 5s of 2035 at 3.20%.

LA DWP 5s of 2049 at 3.90% versus 3.85%-3.73% Thursday and 3.85%-3.84% Wednesday. California 5s of 2052 at 3.93%. Massachusetts 5s of 2053 at 4.15%-4.18% versus 4.11% Wednesday and 4.02%-4.00% on 8/10.

AAA scales

Refinitiv MMD’s scale was unchanged: The one-year was at 3.25% and 3.15% in two years. The five-year was at 2.84%, the 10-year at 2.84% and the 30-year at 3.82% at 3 p.m.

The ICE AAA yield curve was cut one to three basis points: 3.25% (+1) in 2024 and 3.17% (+1) in 2025. The five-year was at 2.84% (+1), the 10-year was at 2.80% (+2) and the 30-year was at 3.84% (+3) at 4 p.m.

The S&P Global Market Intelligence (formerly IHS Markit) municipal curve was unchanged: 3.26% in 2024 and 3.15% in 2025. The five-year was at 2.85%, the 10-year was at 2.85% and the 30-year yield was at 3.81%, according to a 4 p.m. read.

Bloomberg BVAL was cut up to one basis point: 3.24% (unch) in 2024 and 3.14% (unch) in 2025. The five-year at 2.83% (unch), the 10-year at 2.81% (+1) and the 30-year at 3.81% (+1) at 4 p.m.

Treasuries were firmer.

The two-year UST was yielding 4.939% (flat), the three-year was at 4.643% (-3), the five-year at 4.383% (-4), the 10-year at 4.252% (-4), the 20-year at 4.560% (-2) and the 30-year Treasury was yielding 4.378% (-2) at the close.

Primary to come:

Michigan (Aa2/AA+//) is set to price $1.182 billion of Michigan State Trunk Line Fund Rebuilding Michigan Program bonds Tuesday. Wells Fargo Bank.

The New York City Transitional Finance Authority (Aa1/AAA/AAA/) is set to price Wednesday $1 billion of future tax-secured subordinate bonds, Fiscal 2024 Series B, serials 2025-2048, term 2053. Wells Fargo Bank.

San Antonio, Texas, (Aaa/AAA/AA+/) is set to price Tuesday $529.78 million in several series: $159.51 million of general improvement bonds, Series 2023, serials 2024-2043; $46.605 million of combination tax and revenue certificates of obligation, Series 2023, serials 2024-2033; $23.085 million of general improvement bonds, taxable Series 2023, serial 2024; $30.535 million of tax notes, Series 2023, serials 2024-2025; and $270.045 million of tax notes, taxable Series 2023, serial 2026. Ramirez & Co.

The Pennsylvania Turnpike Commission (Aa3/AA-/AA-/AA-) is set to price Tuesday $400 million of turnpike revenue refunding bonds, Series A of 2023, serials 2024, 2027-2053. PNC Capital Markets LLC.

The Sacramento Transportation Authority (/AAA/AAA/) is set to price Tuesday $308.19 million of limited tax sales tax revenue refunding bonds, serials 2028-2038. BofA Securities.

The Texas Department of Housing and Community Affairs (Aaa/AA+//) is set to price Tuesday $200 million of non-AMT residential mortgage revenue bonds, serials 2025-2035, terms 2038, 2043, 2048, 2053, 2054. Jefferies LLC.

The Wisconsin Housing and Economic Development Authority (Aa2/AA+//) is set to price $185 million of non-AMT home ownership revenue social bonds, serials 2024-2035, terms 2038, 2043, 2049, 2054. RBC Capital Markets.

The Ohio Housing Finance Agency (Aaa///) is set to price Thursday $145 million of non-AMT mortgage-backed securities program residential mortgage revenue social bonds, Series 2023 B, serials 2025-2035, terms 2038, 2043, 2048, 2054, 2055. Citigroup Global Markets Inc.

The South Carolina Jobs-Economic Development Authority (/A+/AA-/) is set to price Tuesday $126.065 million of Anmed Health hospital revenue bonds, serials 2040-2043, terms 2048, 2053. Citigroup Global Markets Inc.

The California Infrastructure and Economic Development Bank (Aa2///) is set to price Thursday $113.215 million of Academy of Motion Pictures Arts and Sciences Obligated Group revenue refunding bonds, Series 2023A, serials 2024-2030, 2033-2041. Wells Fargo Bank.

The Dormitory Authority of the State of New York (Aa3//A+/) is set to price Wednesday $111.355 million of State University of New York Dormitory Facilities Revenue Bonds, Series 2023, Series 2023A (Sustainability Bonds) and Series 2023B (Tender). Serials 2024-2043, terms, 2048, 2053. Siebert Williams Shank & Co.

Celina Independent School District, Texas, (Aaa/AAA//) is set to price Tuesday $100 million of unlimited tax school building bonds, Series 2023, PSF guarantee. Piper Sandler & Co, Minneapolis

The Indiana Finance Authority (Aaa/AAA/AAA/) is set to price Thursday $100 million of state revolving fund program green bonds, Series 2023B, serials 2030-2044. RBC Capital Markets.

Competitive:

Hennepin County, Minnesota, (//AAA/) is set to sell $100 million of general obligation bonds at 10:45 a.m. eastern.

Rosemount-Apple Valley ISD, Minnesota, is set to sell $300 million of general obligation facilities maintenance and school building bonds, Series 2023A, Minnesota School District Credit Enhancement Program) at 10:30 a.m. eastern Tuesday.

Smith County, Texas, (/AA+//) is set to sell $160 million of limited tax courthouse bonds at 2:30 p.m. Tuesday.

Christine Albano contributed to this report.