Municipals were weaker Thursday while municipal bond mutual funds reported outflows to start the year. U.S. Treasury yields rose and equities ended mixed.

Triple-A yield curves were cut up to four basis points, depending on the scale, while UST yields rose seven to nine basis points.

The two-year muni-to-Treasury ratio Thursday was at 56%, the three-year at 57%, the five-year at 57%, the 10-year at 57% and the 30-year at 83%, according to Refinitiv Municipal Market Data’s 3 p.m. EST read. ICE Data Services had the two-year at 59%, the three-year at 59%, the five-year at 57%, the 10-year at 59% and the 30-year at 84% at 4 p.m.

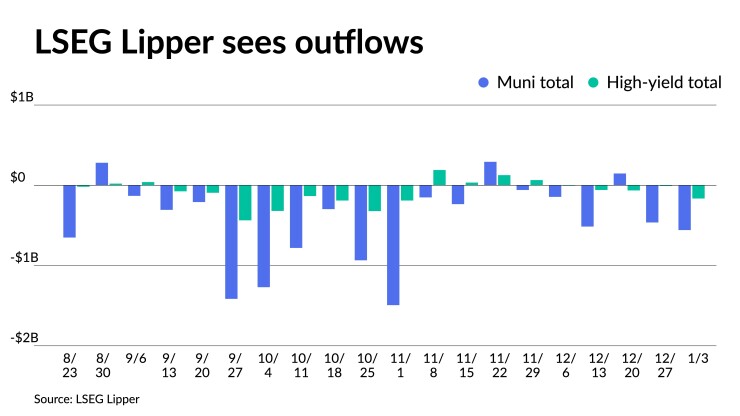

LSEG Lipper reported Thursday that investors pulled $558 million from muni mutual funds for the week ending Wednesday after outflows of $463.7 million the week prior.

High-yield saw outflows of $165 million after outflows of $8.7 million the week prior.

A slower start marked the holiday-shortened week in the municipal market — albeit demand was evident from retail investors, according to Bill Walsh, president of Hennion & Walsh Inc.

“Muni yields have come up five to 10 basis points in response to Treasury weakness the past few days, but overall the tone for municipals remains strong,” Walsh said Thursday.

Despite the uncertainty over how many times the Federal Reserve Board will raise rates this year, Walsh is optimistic about the overall tone of the municipal market, which he said will “remain strong into 2024.”

The muni market enters this year from a relative position of strength, said Jeff Lipton, managing director and head of municipal research and strategy at Oppenheimer, in a Tuesday report.

“Credit quality remains strong across the broad array of muni sectors, absolute yields and attractive cashflows provide a compelling argument to put sidelined cash to work in a tax-efficient manner, better relative value opportunities support future investment performance even after the sharp advances on fixed income asset valuations late last year, and market technicals should bolster out-performance,” he said. “Taxable equivalent yield calculations make the value proposition that much more apparent.”

Taken altogether, this “should extend the gains booked late last year and set up 2024 for positive returns, which for now we project to be in the mid-single digits,” he said.

In 2023, munis returned 6.4% while UST earned 4.05% last year.

USTs saw negative returns in 2021 and 2022, and “saw red in 2023 until green shined through, and we remain bullish on fixed income in 2024,” Lipton said.

Munis historically outperform high-grade debt instruments during periods of rising interest rates and last year “partially followed this trend with tax-exempts outperforming UST, yet underperforming corporates (8.52%) at yearend 2023,” Lipton said.

“However, until muni market technicals and perceptions take hold for the new year, munis may stay closely attached to U.S. Treasuries,” Lipton said in the interview.

“We witnessed this during today’s trading session as stronger hiring and lower than expected unemployment insurance claims questioned the seemingly accelerated path of the Fed’s 2024 pivot to an easing bias, sending the Treasury 10-year benchmark yield closer to 4%,” he said.

Munis responded with noted cuts along the short end of the curve, Lipton said, adding that he suspects that the bond market will react accordingly to Friday’s release of December’s labor market report.

“An outsized payrolls number would likely send the U.S. Treasury 10-year back above 4% with a bit of staying power,” he said.

Municipal security allocations this year “should be rewarded as the potential for total return performance is quite real given the relative likelihood of less market volatility and reasonable prospects for booking something more than ‘carry’ attribution,” according to Lipton.

“This should come given our expectations for a cyclical shift to positive fund flows, likely with accompanying spread compression, as demand for product by a more active (led by mutual funds), and perhaps expanded (more foreign buyer interest), buyer base accelerates in 2024, and as monetary policy mayhem dissipates in a meaningful way,” he said. “This outlook should pave the way for more normalized bid-wanted activity.”

Secondary trading

Virginia 5s of 2025 at 2.68%. Minnesota 5s of 2025 at 2.68%. Washington 4s of 2026 at 2.56%-2.55% versus 2.54%-2.55% Wednesday.

Massachusetts Bay Transportation Authority 5s of 2028 at 2.36%-2.35%. Triborough Bridge and Tunnel Authority 5s of 2028 at 2.36%-2.26%. NY State Urban Development Corp. 5s of 2030 at 2.36% versus 2.33% Wednesday.

Ohio 5s of 2033 at 2.37%. DC 5s of 2034 at 2.31%-2.29%. Connecticut 5s of 2035 at 2/49%-2.47% versus 2.44% on 12/27.

Baltimore County, Maryland, 5s of 2046 at 3.32% versus 3.39% Wednesday. Garland ISD, Texas, 5s of 2048 at 3.53%-3.52% versus 3.53%-3.52% Wednesday and 3.50% on 12/29.

New deals on tap

The new-issue calendar is growing with more large deals from bellwether issuers coming in. Bond Buyer 30-day visible supply grows to $13.04 billion.

Massachusetts (Aa1/AA+/AA+/) is set to price $1.39 billion of GOs, consisting of $850 million of new-issue Consolidated Loan of 2024 bonds, 2024 Series A, and $540 million of refunding bonds, 2024 Series A. Retail order on Wednesday. Institutional pricing on Thursday.

The Southeast Alabama Gas Supply District is set to price $747.250 million of Project No. 1 gas supply revenue refunding bonds, Series 2024A.

The Minnesota Agricultural and Economic Development Board (A2/A//) is set to price $500 million of HealthPartners Obligated Group health care facilities revenue bonds, Series 2024.

The Los Angeles Department of Water and Power (Aa2/AA+//AA+/) is set to price $345 million of water system revenue bonds, 2024 Series A. Retail order on Jan. 17. Institutional pricing on Jan. 18.

AAA scales

Refinitiv MMD’s scale saw cuts on the front of the curve: The one-year was at 2.69% (+4) and 2.47% (+3) in two years. The five-year was at 2.25% (unch), the 10-year at 2.28% (unch) and the 30-year at 3.43% (unch) at 3 p.m.

The ICE AAA yield curve was cut up to two basis points: 2.73% (+2) in 2025 and 2.57% (+2) in 2026. The five-year was at 2.26% (+1), the 10-year was at 2.31% (+1) and the 30-year was at 3.42% (unch) at 4 p.m.

The S&P Global Market Intelligence municipal curve was cut on the front end of the curve: The one-year was at 2.68% (+2) in 2025 and 2.55% (+2) in 2026. The five-year was at 2.27% (unch), the 10-year was at 2.30% (unch) and the 30-year yield was at 3.39% (unch), according to a 3 p.m. read.

Bloomberg BVAL was cut one to three basis points: 2.61% (+2) in 2025 and 2.52% (+2) in 2026. The five-year at 2.23% (+2), the 10-year at 2.29% (+2) and the 30-year at 3.39% (+2) at 4 p.m.

Treasuries were weaker.

The two-year UST was yielding 4.384% (+7), the three-year was at 4.148% (+7), the five-year at 3.972% (+8), the 10-year at 3.990% (+9), the 20-year at 4.296% (+9) and the 30-year Treasury was yielding 4.139% (+9) near the close.

FOMC minute redux

Federal Open Market Committee members “made it pretty clear that they think there’s going to be no more hikes,” but failed to offer any clues on when cuts might start, noted D.A. Davidson Director of Wealth Management Research James Ragan.

Still his major takeaway from the minutes of the December FOMC meeting was: “trends are moving in the right direction,” as the economy and inflation are slowing.”

The markets still may be expecting more cuts in 2024 than the Fed will provide, Ragan said, with 100 basis points a possibility, unless the economy falls into recession.

“I think if the Fed ends up having to go more or does go more than 100 basis points, it’ll be because they have to because things are slowing and so that creates its own challenges,” he said.

The market will be focusing on the 10-year yield, Ragan said.

As for the December employment report, Ragan expects a “decent number,” that’s “not too hot, not too cold,” and “plays right into the way the Fed’s looking at things.”

Christine Albano and Gary Siegel contributed to this story.