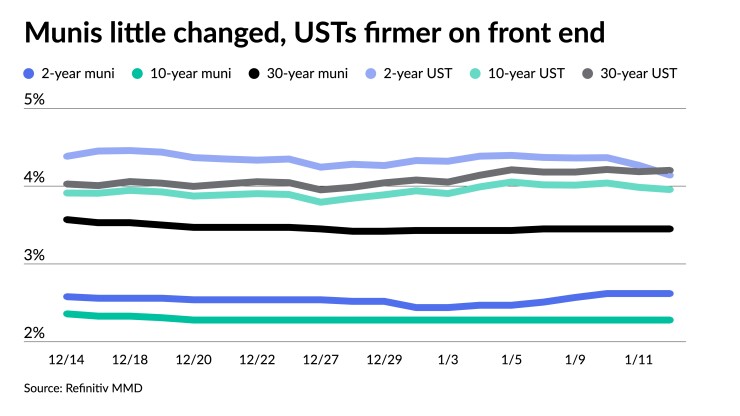

Municipals were little changed ahead of a holiday-shortened week, while U.S. Treasuries were firmer 10 years and in and equities were mixed near the close.

The muni market, as expected, has “remained in a sideways mode” so far in this year with muni-UST ratios grinding lower, said BofA Securities strategists in a weekly report.

While October economic data “showed significant deterioration from the 3Q — supporting the Fed’s dovish turn and large bond market rally in November/December 2023 — overall data since November … paint a picture of quite positive economic growth, and a stubbornly slow decline of inflation,” BofA strategists Yingchen Li and Ian Rogow wrote.

Going into this week, “the market had been eagerly awaiting the December CPI print for confirmation that the softening inflation trend has been firmly entrenched,” said Barclays PLC in a weekly report.

However, market participants are ignoring Thursday’s hotter-than-expected CPI print in favor of this Friday’s lighter-than-expected PPI report, said José Torres, senior economist at Interactive Brokers.

“The marketplace is placing its focus on yet another data point that supports a rate cut while ignoring a more significant one that bolsters a rate hold,” he said.

However, Barclays strategists Mikhail Foux, Clare Pickering and Mayur Patel said “market participants seem to be more assured that the Fed will start cutting soon.”

There is an increased probability of a 25 basis point rate cut in March, with six cuts being priced in for this year, they noted.

“The rates market did not seem too bothered by the inflation prints [Thursday], USTs sold off initially, but rallied later on the back of a strong 30-year auction,” Barclays strategists said.

For the muni market, “a recalibration has occurred only in the front end of the AAA curve so far,” BofA strategists noted.

The MMD AAA scale outside of five years barely changed this year, despite a 20-plus basis point selloff in the UST market, they said.

The muni-UST ratio curve flattened and the 10-year ratio fell to 56.6%, approaching the lower bound of 55% for 2024, BofA strategists said.

Ratios have risen slightly this week with the two-year muni-to-Treasury ratio Friday landing at 63%, the three-year at 63%, the five-year at 59%, the 10-year at 58% and the 30-year at 82%, according to Refinitiv Municipal Market Data’s 3 p.m. EST read. ICE Data Services had the two-year at 63%, the three-year at 62%, the five-year at 60%, the 10-year at 58% and the 30-year at 82% at 3:30 p.m.

Barclays strategists expect supply to be heavy in the first half of the year, “as it is typically front-loaded in presidential years.”

Furthermore, 2023’s UST rally should have also played a positive role, they said.

So far, January has “lived up to expectations as this week’s issuance was about $11 billion, with supply fairly well absorbed, and next week should also be heavy enough despite a holiday,” they said.

The new-issue muni calendar is at an estimated $6.232 million next week with $4.931 billion of negotiated deals on tap and $1.302 billion on the competitive calendar, according to Ipreo and The Bond Buyer.

The California Health Facilities Financing Authority leads the negotiated calendar with $910 million of revenue bonds in three deals, followed by the Dallas Independent School District, Texas, with $503 million of PSF-insured unlimited tax school building and refunding bonds.

The competitive calendar is led by

“Issuance should remain robust, as the 30-day visible supply pipeline remains robust, but only for tax-exempts,” Barclays strategists said. Bond Buyer 30-day visible supply sits at $11.3 billion.

High-grade muni valuations are currently “extremely rich” and the tax-exempt market could see pressure due to “heavy issuance, anemic flows, and rate volatility,” they said.

The 10-year sector has been a “sweet spot” for separately managed accounts, which continue to drive demand, according to Barclays strategists.

“Hence, it is not surprising that the 3s5s, 5s10s and 3s10s yield curves have inverted again for the first time since August 2023,” they said.

Muni CUSIP requests rise

Municipal CUSIP request volume fell sharply in December on a year-over-year basis, following an increase in November, according to CUSIP Global Services.

For muni bonds specifically, there was a decline of 37.3% month-over-month and a 6.7% decrease year-over-year.

The aggregate total of identifier requests for new municipal securities, including municipal bonds, long-term and short-term notes, and commercial paper, fell 33% versus November totals. On a year-over-year basis, overall municipal volumes were down 5.6%. CUSIP requests are an indicator of future issuance.

Secondary trading

DC 5s of 2025 at 2.95% versus 2.81% Tuesday. NYC TFA 5s of 2026 at 2.75%-2.73% versus 2.56% Tuesday. Minnesota 5s of 2027 at 2.54%.

NYC 5s of 2029 at 2.39% versus 2.48% Thursday. Triborough Bridge and Tunnel Authority 5s of 2029 at 2.29% versus 2.40% Thursday. LA DWP 5s of 2030 at 2.08%.

Tennessee 5s of 2033 at 2.30%. University of California 5s of 2034 at 2.12%-2.13%. Iowa Finance Authority 5s of 2035 at 2.42% versus 2.45% Thursday.

NY State Urban Development Corp. 5s of 2050 at 3.68%. Judson ISD, Texas, 4s of 2053 at 4.18%-4.16% versus 4.18%-4.19% Thursday and 4.19% original on Wednesday.

AAA scales

Refinitiv MMD’s scale was unchanged: The one-year was at 2.90% and 2.62% in two years. The five-year was at 2.25%, the 10-year at 2.28% and the 30-year at 3.45% at 3 p.m.

The ICE AAA yield curve was bumped up to two basis points: 2.91% (unch) in 2025 and 2.69% (unch) in 2026. The five-year was at 2.34% (-1), the 10-year was at 2.29% (-1) and the 30-year was at 3.42% (-1) at 3:30 p.m.

The S&P Global Market Intelligence municipal curve was unchanged: The one-year was at 2.89% in 2025 and 2.66% in 2026. The five-year was at 2.29%, the 10-year was at 2.32% and the 30-year yield was at 3.42%, according to a 3 p.m. read.

Bloomberg BVAL was unchanged: 2.79% in 2025 and 2.64% in 2026. The five-year at 2.29%, the 10-year at 2.33% and the 30-year at 3.43% at 3:30 p.m.

Treasuries were firmer 10 years and in.

The two-year UST was yielding 4.145% (-12), the three-year was at 3.932% (-9), the five-year at 3.841% (-6), the 10-year at 3.957% (-3), the 20-year at 4.313% (flat) and the 30-year Treasury was yielding 4.204% (+2) near the close.

N.Y. issuers plan $4.4B sales in Q1

New York State, New York City and their major public authorities plan to issue $4.36 billion of bonds in the first quarter, state Comptroller Thomas DiNapoli announced Friday.

The planned sales include $3.11 billion of new money and $1.25 billion of refundings and reofferings. In January, $1.4 billion is scheduled with $600 million for new-money purposes and $800 million for refundings while in February $2.96 billion is planned to be sold, $2.51 billion of which is new-money and $450 million for refunding and reofferings.

The anticipated first quarter sales compare to past planned sales of $9.11 billion in the fourth quarter of 2023 and $1.76 billion in the first quarter of 2023.

The calendar includes sales by NYC, the Nassau County Interim Finance Authority, the NYC Transitional Finance Authority, the NYS Housing Finance Agency, the NYS Thruway Authority, the State of New York Mortgage Agency and the Triborough Bridge and Tunnel Authority.

Primary to come

The California Health Facilities Financing Authority (/AA-/AA/) is set to price Thursday $532.415 million of Scripps Health revenue bonds, Series 2024A. Morgan Stanley.

The authority is also set to price Thursday $270.030 million of Scripps Health revenue bonds, Series 2024B, consisting of $135.015 million of Series 2024B-1 and $135.015 million of Series 2024B-2. Morgan Stanley.

Additionally, the authority (//A-/) is set to price Wednesday $107.740 million of Episcopal Communities & Services revenue bonds, consisting of $30 million of Series 2024A, serial 2027; and $77.740 million of Series 2024B, serials 2028-2033, terms 2043, 2048, 2053, 2058. KeyBanc Capital Markets.

The Dallas Independent School District, Texas, (Aaa/AAA/AAA/) is set to price Thursday $502.965 million of PSF-insured unlimited tax school building and refunding bonds, Series 2024, serials 2025-2054. Siebert Williams Shank & Co.

The Pennsylvania Turnpike Commission (Aa3/AA-/AA-/AA-/) is set to price Thursday $435.120 million of turnpike revenue bonds, Series A of 2024. Goldman Sachs.

The North Carolina Turnpike Authority (/AA/BBB+/) is set to price Wednesday $348.943 million of Assured Guaranty-insured Triangle Expressway System senior lien turnpike revenue bonds, Series 2024, consisting of $277.120 million of bonds, Series A, serials 2055-2058, and $71.823 million of capital appreciation bonds, Series B, serials 2041-2055. BofA Securities.

The Los Angeles Department of Water and Power (Aa2/AA+//AA+/) is set to price Thursday $345 million of water system revenue bonds, 2024 Series A, serials 2029-2044, terms 2049, 2054. Wells Fargo Bank.

The Massachusetts Development Finance Agency (Aa3/AA-//) is set to price Wednesday $309.130 million of Mass General Brigham Issue revenue refunding bonds, Series 2024D, serials 2030-2038, 2042-2043, 2047, 2054. RBC Capital Markets.

The Connecticut Health and Educational Facilities Authority is set to price Wednesday $275 million, consisting of $125 million of Series X-2 and $150 million of Series A-3. J.P. Morgan Securities.

The San Juan Unified School District, California, (Aa2///) is set to price Thursday $231.490 million of GOs, consisting of $125 million of Election of 2016 bonds, serials 2025-2027, 2030-2049, and $106.490 million of refunding bonds, serials 2024-2031. Raymond James & Associates.

The Health, Educational and Housing Facility Board of the County of Knox, Tennessee, (/AA//) is set to price Wednesday $220.810 million of BAM-insured University of Tennessee Project student housing revenue bonds, consisting of $218.290 million of tax-exempts, Series 2024A-1, serials 2031-2044, terms 2049, 2054, 2059, 2064; and $2.520 million of taxables, Series 2024A-2, term 2031. RBC Capital Markets.

Riverside, California, (/AA-/AA-/) is set to price Wednesday $214.610 million of electric revenue bonds, Issue of 2024A. J.P. Morgan Securities.

The Harris County Cultural Education Facilities Finance Corp., Texas, (/A//) is set to price Wednesday $100 million of Baylor College of Medicine medical facilities mortgage revenue bonds, Series 2024A, serial 2029. Barclays.

Competitive

Illinois is set to sell $300 million

The Mankato Independent School District No. 77, Minnesota, (A1///) is set to sell $105 million of GO school building bonds, at 11 a.m. Wednesday.

The Triborough Bridge and Tunnel Authority is set to sell $294.855 million of MTA bridges and tunnels climate bond certified payroll mobility tax senior lien green bonds, Series 2024A, at 10:15 a.m. Thursday.

The South Washington County Independent School District No. 833, Minnesota, is set to sell $133.115 million of GO school building, facilities maintenance and refunding bonds, Series 2024A, at 11 a.m. Thursday.

Chip Barnett contributed to this story.