Municipals were little changed Wednesday amid another busy primary session as U.S. Treasury yields rose throughout most of the curve and equities ended up.

Despite municipal performance being in the red to start to 2023, municipal mutual funds continue to see inflows.

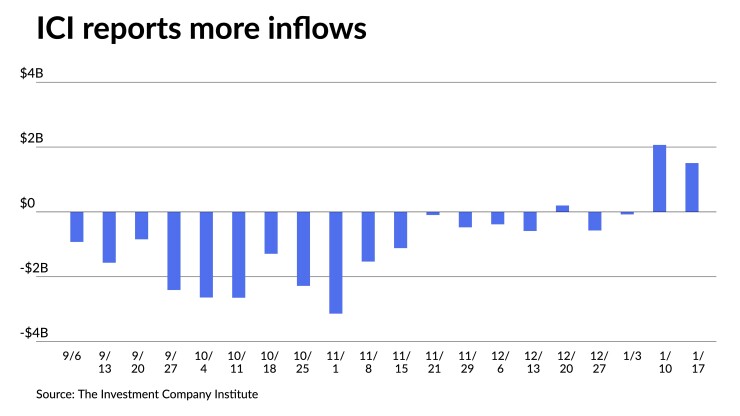

The Investment Company Institute Wednesday reported more inflows into municipal bond mutual funds for the week ending Jan. 17, with investors adding $1.506 billion to funds following

Exchange-traded funds, meanwhile, saw inflows of $293 million following $1.082 billion of outflows the week prior.

Jeff Lipton, managing director of credit research at Oppenheimer Inc., noted that “other institutional investors have yet to step in with conviction,” and he suspects that current ratios “account for part of the push-back.”

The two-year muni-to-Treasury ratio Wednesday was at 62%, the three-year at 63%, the five-year at 60%, the 10-year at 59% and the 30-year at 82%, according to Refinitiv Municipal Market Data’s 3 p.m. EST read. ICE Data Services had the two-year at 65%, the three-year at 64%, the five-year at 62%, the 10-year at 61% and the 30-year at 83% at 3:30 p.m.

“Once primary activity normalizes, with broader professional support, secondary market conditions can fall in line with spreads adjusting accordingly and more positive flow activity taking hold,” he said.

The asset class is currently seeing pressure from building primary supply, though Lipton notes “such pressure … is not the worst thing to occur given the swift and sharp run-up in muni valuations that has made any attempt of even a fly-by correction seem justified.”

Munis are currently outperforming USTs month-to-date, “as the tax-exempt asset class continues to find residual strength from the late Q4 rally that produced historic price advances and overall outperformance for 2023,” he noted.

However, Lipton said the performance gap has narrowed in recent trading sessions and could shrink even further if tax-exempt performance continues to be pressured by muni technicals.

The attainment of fair value was “generally elusive” in 2023, but “after ratios found themselves stuck in expensive ground for much of the earlier part of the year, the value play did become more compelling last year, only to find ratios growing more expensive at year-end,” according to Lipton.

This dynamic, he noted, “set the stage for the new year, with some type of correction not unexpected.”

Despite fixed-income seeing losses this month, Lipton believes “a performance sea change is nearing given the widely held expectations for an easing bias, coupled with the unique muni market technicals that often promote favorable returns for the asset class.”

In the primary market Tuesday, Jefferies priced for institutions $1.251 billion of general revenue bonds from the

The second tranche, $200.430 million of 2024 Series BT, saw 5s of 5/2026 at 2.76% (+10), noncall.

Wells Fargo Bank priced for Rock Hill, South Carolina, (A2/A+//) $162 million of combined utility system revenue bonds, Series 2024A, with 5s of 1/2027 at 2.90%, 5s of 2029 at 2.77%, 5s of 2034 at 2.86%, 5s of 2039 at 3.46%, 4s of 2044 at 4.14%, 4s of 2049 at 4.32%, 5s of 2054 at 4.23%, 4.25s of 2059 at 4.62% and 5s of 2064 at 4.43%, callable 1/1/2034.

BofA Securities priced for Warren County, Kentucky, (/AA-/AA-/) $142.310 million of Bowling Green-Warren County Community Hospital Corp. hospital revenue bonds, Series 2024, with 5s of 4/2033 at 3.00%, 5s of 2034 at 3.00%, 5s of 2039 at 3.54%, 5s of 2044 at 3.87%, 5.25s of 2049 at 4.10% and 5.25s of 2054 at 4.19%, callable 4/1/2034.

Piper Sandler priced for the Salado Independent School District, Texas, (/AAA//) $105.230 million of PSF-insured unlimited tax school building bonds, Series 2024, with 5s of 2/2025 at 3.20%, 5s of 2029 at 2.72%, 5s of 2034 at 2.76%, 5s of 2039 at 3.29%, 5s of 2044 at 3.66%, 4s of 2049 at 4.17% and 4.25s of 2054 at 4.32%, callable 2/15/2033.

In the competitive market, Fairfax County, Virginia, (Aaa/AAA/AAA/) sold $323.315 million of public improvement bonds, Series 2024A, to BofA Securities, with 5s of 10/2024 at 3.00%, 5s of 2029 at 2.45%, 4s of 2034 at 2.55%, 4s of 2039 at 3.46% and 4s of 2043 at 3.84%, callable 4/1/2033.

Money market funds see outflows

Tax-exempt municipal money market funds saw outflows as $5.05 billion was pulled the week ending Jan. 22, bringing the total assets to $117.62 billion, according to the Money Fund Report, a weekly publication of EPFR.

The average seven-day simple yield for all tax-free and municipal money-market funds rose to 2.26%.

Taxable money-fund assets saw $20.53 billion added to end the reporting week.

The average seven-day simple yield for all taxable reporting funds remained at 5.03%.

Secondary trading

Washington 5s of 2025 at 3.02% versus 3.03% Tuesday. NYC 5s of 2026 at 2.80%-2.78% versus 2.60% on 1/9. Maryland 5s of 2027 at 2.64%-2.62%.

Georgia 4s of 2028 at 2.57% versus 2.55% on 1/17. California 5s of 2028 at 2.62%-2.59% versus 2.50% on 1/17. Denton County, Texas, 5s of 2029 at 2.67%.

DASNY 5s of 2032 at 2.62%. Florida DOT 5s of 2033 at 2.50% versus 2.54% Tuesday. Washington 5s of 2034 at 2.71%.

Massachusetts 5s of 2053 at 4.01%-4.00% versus 4.01% Tuesday. Triborough Bridge and Tunnel Authority 5s of 2054 at 3.96% versus 3.88% Monday and 3.88% original on Thursday.

AAA scales

Refinitiv MMD’s scale was unchanged: The one-year was at 3.01% and 2.73% in two years. The five-year was at 2.45%, the 10-year at 2.46% and the 30-year at 3.61% at 3 p.m.

The ICE AAA yield curve was little changed: 2.98% (-1) in 2025 and 2.82% (unch) in 2026. The five-year was at 2.52% (unch), the 10-year was at 2.50% (+1) and the 30-year was at 3.61% (+1) at 3:30 p.m.

The S&P Global Market Intelligence municipal curve was unchanged: The one-year was at 3.01% in 2025 and 2.77% in 2026. The five-year was at 2.45%, the 10-year was at 2.47% and the 30-year yield was at 3.60%, according to a 3 p.m. read.

Bloomberg BVAL was unchanged: 2.97% in 2025 and 2.83% in 2026. The five-year at 2.48%, the 10-year at 2.54% and the 30-year at 3.63% at 3:30 p.m.

Treasuries lost ground.

The two-year UST was yielding 4.375% (-1), the three-year was at 4.182% (+3), the five-year at 4.084% (+4), the 10-year at 4.175% (+4), the 20-year at 4.519% (+3) and the 30-year Treasury was yielding 4.406% (+3) at 3:45 p.m.