Municipals were lightly traded and little changed Friday ahead of a smaller new-issue calendar amid the Federal Open Market Committee meeting while U.S. Treasuries were weaker. Equities were mixed to close the session.

Rates have continued creeping higher and muni yields have been following, as the “positive effect of the year-end technicals has finally started to wane,” Barclays PLC said in a report.

Preliminary economic data for January reported over the past two weeks supports a soft landing scenario, causing the Treasury yield curve to bear steepen, noted BofA Global Research in a weekly report.

“Good PMI data for services and manufacturing for January are not supporting any meaningful weakening in the labor market, which may extend the current Treasury yield backup process to mid-February when the next CPI report is delivered,” BofA strategists Yingchen Li and Ian Rogow wrote. ”Surely, as the Fed shifted the focus to the timing of the first rate cut, and the short end of the curves are more-or-less anchored to the Fed dot plot, the yield backup process should remain controlled with a steepening bias.”

Unlike Treasuries, they note the 1s10s tax-exempt muni curve bear flattened while the 10s30s AAA curve remained steep, they said.

“The 1s10s curve inverted back below -50bp, supporting our view that the 1s10s curve may remain inverted for all of 2024,” Li and Rogow wrote.

The story for exempt AAA to taxable muni AAA ratios is similar, they said. “They range from a low of 52.0% at the 10 year, according to MMD data, to a high of 65.6% at the 29 and 30 year,” they said.

“Even at the 29 year and 30 year, those ratios are just below the 22nd percentile of their last 12-month range,” BofA said. “In fact, only ratios 11 years and in are above the 25th percentile, and only above the 50th percentile 3 years and in. This data all goes to show the compressed relative value in exempts currently.”

The two-year muni-to-Treasury ratio Friday was at 63%, the three-year at 63%, the five-year at 61%, the 10-year at 60% and the 30-year at 83%, according to Refinitiv Municipal Market Data’s 3 p.m. EST read. ICE Data Services had the two-year at 64%, the three-year at 64%, the five-year at 62%, the 10-year at 61% and the 30-year at 82% at 3:30 p.m.

Barclays strategists Mikhail Foux, Clare Pickering and Mayur Patel said they expect heavier supply in the first quarter, even with the light week due to the FOMC.

The new-issue calendar comes in at $3.38 billion the week of Jan. 29, down from total sales of $8.225 billion the week of Jan. 22, per Ipreo and Bond Buyer data.

There are $3.006 billion of municipal bond sales scheduled for negotiated sale and $374 million on the competitive slate. There are only seven deals above $100 million.

Leading the calendar is the New York State Thruway Authority (A1/A+//), set to price Tuesday $1.030 billion of general revenue bonds, Series P, with senior manager J.P. Morgan Securities.

The Massachusetts Development Finance Agency (Aa2/AA//) is set to price Tuesday $442.355 million of Children’s Hospital Issue revenue bonds, Series 2024 T, also led by J.P. Morgan.

Bond Buyer 30-day visible supply sits at $6.8 billion.

“January’s supply will likely be heavier than in previous years, and the pipeline next month should also be sizable,” Barclays said. “However, historically March is when muni technicals typically start to turn negative, due to the negative effect of tax selling coupled with higher net issuance (the average net supply over the past three years has been nearly $17 billion).”

BofA expects yields to continue to move up and credit spreads narrow “in a slow and gentle fashion” in February.

A few weeks ago, BofA suggested that if the 10-year AAA yield rises 30+bp, “good entry points should be near.” Year-to-date, the 10-year AAA has risen 18bp.

“We expect $27 billion of new issuance in February, $33 billion of principal redemption and $16 billion of coupon payments,” they said. “Demand will again overwhelm supply.”

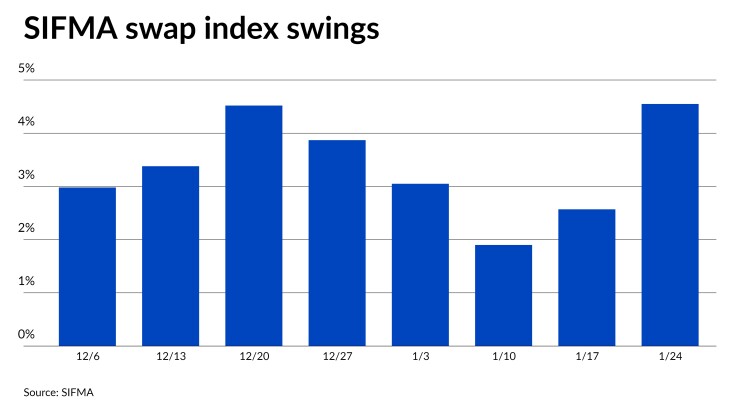

Floating rate volatility

Barclays noted that volatility in short-term muni floating rates has increased. The SIFMA index jumped from 2.57% to 4.55% — “one of the largest weekly increases of all time,” they said.

Barclays noted that at the end of 2023, there was a flood of cash into tax-exempt money market funds due to attractive rates and heavy re-investments, “which pushed yields down and immediately caused fund outflows, and higher SIFMA rates.”

“This volatility in short-term markets has been extreme; however, we believe that for investors looking to just roll their VRDN exposure on a weekly basis, realized average returns have still been quite attractive — and actually quite stable despite weekly price jumps in reset levels (3.5% over the past 3 months, and 3.6% over the past 6 months,” they said. “We continue to like this strategy in the early part of 2024, as yield volatility will likely remain elevated, and this a good way to wait it out while still parking money in tax-exempt investments.”

Looking ahead, Barclays said they “remain cautious, but still see a number of relative value opportunities … especially if investors trade down in credit quality, as a stronger-than-expected economy bodes well for lower-rated credits.”

AAA scales

Refinitiv MMD’s scale was unchanged: The one-year was at 2.99% and 2.71% in two years. The five-year was at 2.43%, the 10-year at 2.46% and the 30-year at 3.61% at 3 p.m.

The ICE AAA yield curve was little changed: 2.97% (unch) in 2025 and 2.81% (unch) in 2026. The five-year was at 2.50% (unch), the 10-year was at 2.49% (-1) and the 30-year was at 3.60% (unch) at 3:30 p.m.

The S&P Global Market Intelligence municipal curve was unchanged: The one-year was at 2.99% in 2025 and 2.77% in 2026. The five-year was at 2.45%, the 10-year was at 2.47% and the 30-year yield was at 3.60%, according to a 3 p.m. read.

Bloomberg BVAL was unchanged: 2.96% in 2025 and 2.82% in 2026. The five-year at 2.48%, the 10-year at 2.53% and the 30-year at 3.63% at 3:30 p.m.

Treasuries were weaker.

The two-year UST was yielding 4.355% (+4), the three-year was at 4.139% (+3), the five-year at 4.04% (+2), the 10-year at 4.14% (+1), the 20-year at 4.486% (flat) and the 30-year Treasury was yielding 4.375% (flat) at the close.

Primary to come

The New York State Thruway Authority (A1/A+//) is set to price Tuesday $1.030 billion of general revenue bonds, Series P. J.P. Morgan.

The Massachusetts Development Finance Agency (Aa2/AA//) is set to price Tuesday $442.355 million of Children’s Hospital Issue revenue bonds, Series 2024 T. J.P. Morgan.

The Rhode Island Health and Educational Building Corp. (/BBB+/BBB+/) is set to price Thursday $300 million of Lifespan Obligated Group Issue hospital financing revenue bonds, Series 2024. Morgan Stanley.

Tacoma, Washington, (/AA/AA-/) is set to price Tuesday $188.510 million of electric system revenue bonds, consisting of $94.370 million of new-issue green bonds, Series 2024A, and $94.140 million of refunding bonds, Series 2024B. J.P. Morgan.

The Indiana Housing and Community Development Authority (Aaa//AA+/) is set to price Tuesday $134.510 million of social single family mortgage revenue bonds, consisting of $101.250 million of non-AMT bonds, 2024 Series A-1, serials 2034-2036, terms 2039, 2044, 2049, 2054; and $33.260 million of taxables, 2024 Series A-2, serials 2024-2031, term 204. RBC Capital Markets.

The Nassau County Interim Finance Authority, New York, (/AAA//) is set to price $127.830 million of sales tax secured bonds, Series 2024A, serials 2024-2030. BofA Securities.

The Alvin Independent School District, Texas, is set to price Thursday $102.455 million of unlimited tax schoolhouse and refunding bonds, Series 2024. Piper Sandler.

Competitive

The Spartanburg County School District No. 5, South Carolina, (Aa1/AA//) is set to sell $95 million of GOs at noon Tuesday.