Municipals were steady in secondary trading Tuesday as several large deals in the primary market took focus, including the retail pricing for the

Other large deals in the negotiated market included Wisconsin with $491.290 million of GO refunding bonds and the Texas Transportation Commission with $346.820 million of State Highway Fund first-tier revenue refunding bonds.

The California Infrastructure and Economic Development Bank led the competitive calendar with $272.95 million of green Clean Water and Drinking Water State Revolving Fund revenue bonds sold to Morgan Stanley.

The increase in supply this week should “be priced to sell as dealers want to keep inventory moving,” said Anders S. Persson, Nuveen’s chief investment officer for global fixed income, and Daniel J. Close, Nuveen’s head of municipals. It should be well received, they added.

Despite the increase in issuance this week, “there is not enough supply to satisfy demand,” Persson and Close said.

Over the last three months, “outsized investment money” has come into the market, and investors are “scrambling to get cash invested,” they said.

While new-issue supply has started to increase, it is not “keeping pace” with demand, they said.

Munis should remain “well bid” until issuance picks up “dramatically,” Persson and Close said.

Several large deals on tap for the next few weeks should help.

Harvard University is coming to market with as much as $1.65 billion of fixed-rate bonds: $750 million of taxables next week and up to $900 million of tax-exempts in April.

The New York City Municipal Water Finance Authority (Aa1/AA+/AA+/) is set to price Tuesday $757.655 million of water and sewer system second general resolution revenue bonds.

Beyond this, the Dormitory Authority of the State of New York (Aa1/AA+//) is set to price the week of March 11 $3.5 billion of state personal income tax revenue bonds.

The Metropolitan Transportation Authority is set to price the week of March 25 $1 billion of revenue refunding bonds.

Contributing to the increase in supply is

So far, six issuers with $6.4 billion of BABs outstanding have announced financing considerations to ERP call this debt, J.P. Morgan strategists noted.

This is a “marked increase” from 2018-2022 when the average amount of calls was $120 million.

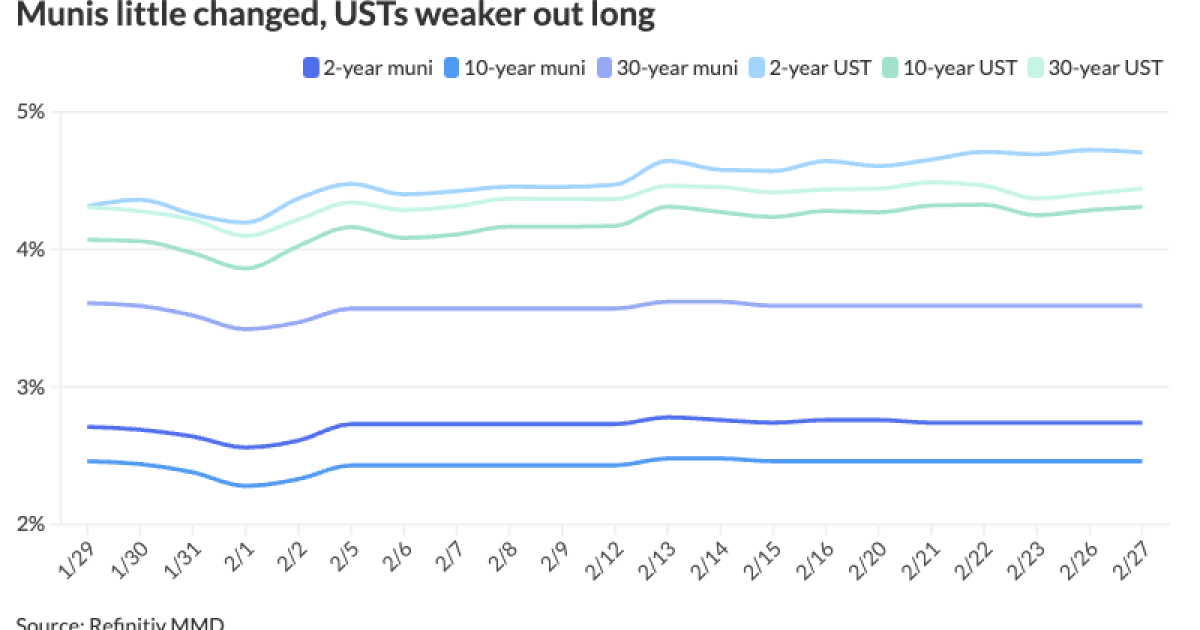

Meanwhile, tax-exempts are “extremely rich” versus USTs, Fabian said.

The two-year muni-to-Treasury ratio Tuesday was at 58%, the three-year at 57%, the five-year at 56%, the 10-year at 57% and the 30-year at 81%, according to Refinitiv Municipal Market Data’s 3 p.m. EST read. ICE Data Services had the two-year at 59%, the three-year at 58%, the five-year at 57%, the 10-year at 58% and the 30-year at 81% at 3:30 p.m.

Muni-UST ratios 10 years and in are below 60%, making it difficult for crossover buyers, such as insurance companies, to be buyers, he said.

Mutual fund returns “have also been mixed at best,” he said. Recent NAV gains, especially in high-yield, haven’t “retraced losses” since Feb. 1.

While the Investment Company Institute has reported inflows for six consecutive weeks, LSEG Lipper has reported three straight weeks of outflows, “perhaps reflecting account liquidations of [exchange-traded fund] shares for reinvestment in active funds or bonds or for other opportunities (e.g., stocks),” Fabian said.

However, “even where there are inflows there are caveats,” he said.

The ETF HYMB “disclosed $140 million of net creations last week (most for any ETF) but that total exactly offsets the ETF’s net redemptions in January,” he said.

As far as retail, he said “it is highly likely that, while Fed restraint on rate cuts has encouraged cash to linger for longer in money funds, CDs, and enhanced savings accounts, the tremendous rally in tech stocks will be pulling free cash away from tax-exempt products.”

And banks, facing new commercial real estate exposure headline risks, do not seem to be buying munis so far this year, Fabian said.

Secondary trading

Massachusetts 5s of 2025 at 2.97%. NYC 5s of 2025 at 2.90% versus 2.96% Monday. Charlotte waters, North Carolina, 5s of 2026 at 2.72%.

Florida BOE 5s of 2028 at 2.51%. Georgia 5s of 2028 at 2.49%. Ohio 5s of 2029 at 2.54%.

Collin County, Texas, 5s of 2033 at 2.58%. NYC TFA 5s of 2036 at 2.76% versus 2.75%-2.74% Monday and 2.82%-2.81% on 2/15. University of California 5s of 2037 at 2.55% versus 2.59% Monday and 2.59%-2.58% Friday.

NYC TFA 5s of 2049 at 3.90%-3.88% versus 3.91% Monday and 3.84%-3.86% Friday. LA DWP 5s of 2054 at 3.52%-3.38% versus 3.56% Monday.

AAA scales

Refinitiv MMD’s scale was little changed: The one-year was at 2.98% (+2) and 2.74% (unch) in two years. The five-year was at 2.44% (unch), the 10-year at 2.46% (unch) and the 30-year at 3.59% (unch) at 3 p.m.

The ICE AAA yield curve was unchanged: 2.98% in 2025 and 2.77% in 2026. The five-year was at 2.45%, the 10-year was at 2.48% and the 30-year was at 3.56% at 3:30 p.m.

The S&P Global Market Intelligence municipal curve was little changed: The one-year was at 2.96% (+1) in 2025 and 2.74% (unch) in 2026. The five-year was at 2.44% (unch), the 10-year was at 2.47% (unch) and the 30-year yield was at 3.57% (unch), according to a 3 p.m. read.

Bloomberg BVAL was unchanged: 2.95% in 2025 and 2.81% in 2026. The five-year at 2.46%, the 10-year at 2.53% and the 30-year at 3.65% at 3:30 p.m.

Treasuries were weaker out long.

The two-year UST was yielding 4.703% (-2), the three-year was at 4.493% (flat), the five-year at 4.316% (flat), the 10-year at 4.310% (+2), the 20-year at 4.571% (+3) and the 30-year at 4.439% (+3) at 3:45 p.m.

Primary market on Tuesday

BofA Securities held a one-day retail offer for $1.509 billion of GOs from New York City. The first tranche was $1.2 billion of Fiscal Series 2024-C.

| Maturity | Coupon | Yield |

| 3/2026 | 5% | 2.83% |

| 3/2029 | 5% | 2.59% |

| 3/2034 | 5% | 2.71% |

| 3/2054 | 4.25% | 4.37%. |

The second tranche was $85.030 million of Fiscal 2006 Series J, Subseries J-A.

| Maturity | Coupon | Yield |

| 6/2032 | 5% | 2.67% |

| 6/2034 | 5% | 2.72% |

| 6/2036 | 5% | 2.93% |

The third tranche is $36.855 million of Fiscal 2008 Series A, Subseries A-4.

| Maturity | Coupon | Yield |

| 8/2024 | 5% | 3.00% |

| 8/2026 | 5% | 2.79% |

The fourth tranche is $93.625 million of Fiscal 2008 Series C, Subseries C-4.

| Maturity | Coupon | Yield |

| 10/2026 | 5% | 2.77% |

| 10/2027 | 5% | 2.64% |

The fifth tranche is $93.850 million of Fiscal 2009 Series B, Subseries B-3,

| Maturity | Coupon | Yield |

| 9/2026 | 5% | 2.78% |

| 9/2027 | 5% | 2.64% |

BofA Securities priced for Wisconsin (Aa1/AA+//AAA/) $491.290 million of GO refunding bonds. The first tranche was $401.765 million of bonds of 2024, Series 1.

| Maturity | Coupon | Yield |

| 5/2025 | 5% | 2.95% |

| 5/2029 | 5% | 2.52% |

| 5/2034 | 5% | 2.59% |

| 5/2038 | 5% | 2.94% |

The second tranche was $89.525 million of forward-delivery bonds of 2025, Series 1.

| Maturity | Coupon | Yield |

| 5/2033 | 5% | 2.99% |

| 5/2034 | 5% | 3.01% |

| 5/2036 | 5% | 3.15% |

Ramirez & Co. priced for the Texas Transportation Commission (Aaa/AAA//) $346.595 million of State Highway Fund first-tier revenue refunding bonds, Series 2024.

| Maturity | Coupon | Yield |

| 4/2025 | 5% | 2.97% |

| 10/2030 | 5% | 2.49% |

| 10/2033 | 5% | 2.64% |

Stifel, Nicolaus & Co. priced for the Phoenix Union High School District No. 210, Arizona, (Aa1/AA/AAA/) $143.960 million of Project of 2023 school improvement bonds, Series 2024A.

| Maturity | Coupon | Yield |

| 7/2024 | 5% | 3.06% |

| 7/2029 | 5% | 2.51% |

| 7/2034 | 5% | 2.62% |

| 7/2039 | 5% | 3.02% |

BofA Securities priced for the Regents of the University of Minnesota (Aa1/AA//) $107.7 million of GO refunding bonds, Series 2024A.

| Maturity | Coupon | Yield |

| 1/2025 | 5% | 2.99% |

| 1/2029 | 5% | 2.50% |

| 1/2034 | 5% | 2.57% |

| 1/2044 | 5% | 3.42% |

Morgan Stanley priced for the Dormitory Authority of the State of New York (Baa2/BBB//) $100 million of New York Institute of Technology revenue bonds, Series 2024.

| Maturity | Coupon | Yield |

| 7/2027 | 5% | 2.87% |

| 7/2029 | 5% | 2.89% |

| 7/2034 | 5% | 3.18% |

| 7/2054 | 5.25% | 4.24% |

Competitive on Tuesday

The California Infrastructure and Economic Development Bank (Aaa/AAA/AAA/) sold $272.950 million of green Clean Water and Drinking Water State Revolving Fund revenue bonds, to Morgan Stanley.

| Maturity | Coupon | Yield |

| 10/2024 | 5% | 3.00% |

| 10/2029 | 5% | 2.22% |

| 10/2034 | 5% | 2.30% |

| 10/2045 | 4% | 3.55% |

Oyster Bay, New York, sold $165.857 million of water district notes, Series 2024, to Wells Fargo.

| Maturity | Coupon | Yield |

| 3/2025 | 4% | 3.10% |