Municipals were a basis point or two weaker out long Wednesday as U.S. Treasuries were mixed and equities sold off.

The muni market is “well positioned” to start the third quarter, said Daniel J. Close, head of municipals at Nuveen.

Supply “increased meaningfully” in the second as issuers came to market with long-delayed deals “due to execution uncertainty and sought to get ahead of volatility that may accompany the U.S. election,” he said.

“Despite the lumpier issuance calendar, meaningful coupon payments and bond maturities provided a natural buyer for the elevated supply,” Close said.

Supply has been elevated for most weeks in Q3, with this week marking the third straight week of issuance clocking in at around $10 billion, said J.P. Morgan strategists led by Peter DeGroot.

Due to this, technicals will be “challenged.” Other issue include mid-July reinvestment capital likely spent, dealer inventories remain elevated and hedge funds expect to sell as secondary demand materializes, they said.

“While supply has been outsized over the last several weeks, the market has also seen

“We are now in the midst of the season when a tidal wave of cash from coupons and maturities needs to be reinvested back into the market,” said AllianceBernstein strategists. “That number this year is anticipated to be $46 billion.”

This dynamic has helped munis outperform so far this summer, they said.

The two-year muni-to-Treasury ratio Wednesday was at 65%, the three-year at 66%, the five-year at 66%, the 10-year at 65% and the 30-year at 81%, according to Refinitiv Municipal Market Data’s 3 p.m. EST read. ICE Data Services had the two-year at 64%, the three-year at 65%, the five-year at 66%, the 10-year at 66% and the 30-year at 82% at 3:30 p.m.

Meanwhile, muni-UST ratios are likely to “go lower” in the near term but may “bound around” based on the supply/demand dynamics, said Matthew Norton, chief investment officer of municipal bonds at AllianceBernstein.

However, he thinks that as cash flows out of money markets and back into the muni market, ratios will fall as market participants attempt to lock in higher yields once the Federal Reserve starts cutting rates.

Reinvestment cash will also play a role in lower ratios, according to Norton.

Muni mutual funds have had a “bit of a wild ride” over the past several years, he noted.

There were large outflows in 2022, followed by more outflows — albeit smaller — in 2023.

This year, fund flows have started to reverse and turn positive, Norton said.

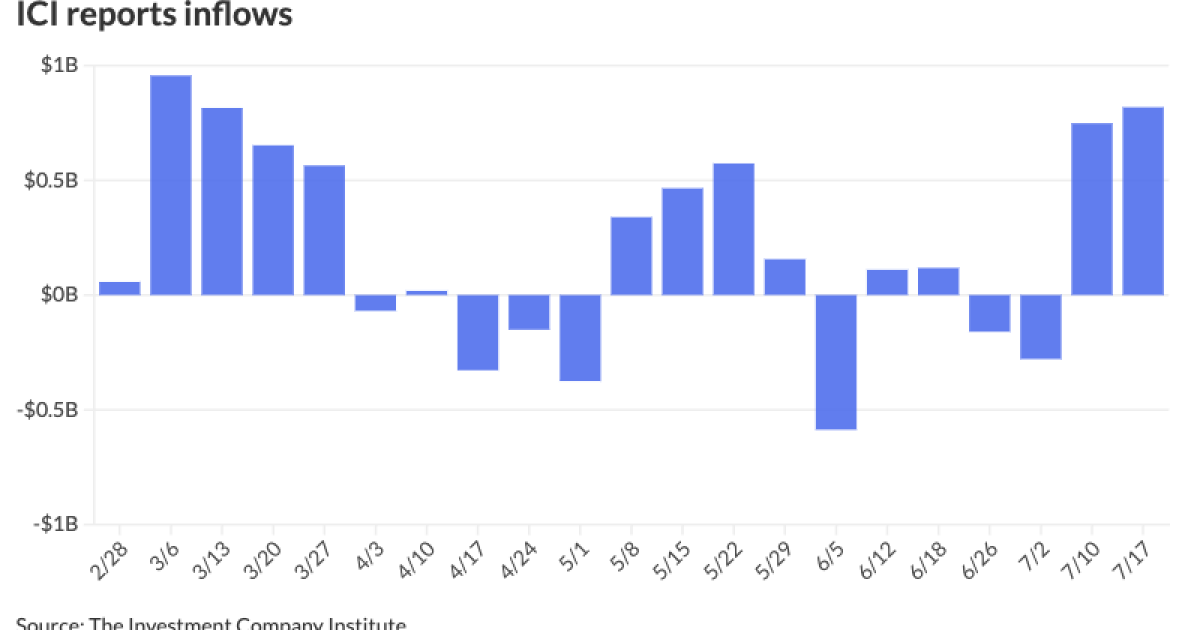

The Investment Company Institute reported Wednesday $818 million of inflows to municipal bond mutual funds for the week ending July 17 following

Exchange-traded funds saw inflows of $814 million, following inflows of $1.251 billion the week prior.

Issuance on Wednesday

In the primary market Wednesday, Wells Fargo priced and repriced for the Minneapolis-St. Paul Metropolitan Airports Commission (/A+/A+/) $671.15 million of subordinate airport revenue bonds, with yields bumped up to eight basis points from the preliminary pricing. The first tranche, $206.02 million of governmental/non-AMT bonds, Series 2024A, saw 5s of 1/2052 at 4.08% (-3) and 5s of 2054 at 4.28% (-8), callable 1/1/2034.

The second tranche, $465.125 million of private activity/AMT bonds, saw 5s of 1/2026 at 3.55% (unch), 5s of 2029 at 3.57% (-3), 5s of 2034 at 3.73% (unch), 5s of 2039 at 3.92% (unch), 5.25s of 2044 at 4.16% (-2), and 5.25s of 2049 at 4.29% (-4), callable 1/1/2034.

BofA Securities priced and repriced for King County, Washington, (Aa1/AA+//) $394.575 million of sewer revenue refunding bonds, 2024 Series A, with 5s of 1/2025 at 2.95% (-2), 5s of 2029 at 2.85% (-5), 5s of 2034 at 3.02% (+2), 5s of 2039 at 3.25% (-2), 5s of 2044 at 3.58% (-5), 5s of 2049 at 3.85% (unch) and 5.25s of 2055 at 3.91% (+2), callable 7/1/2034.

BofA priced for the Pennsylvania Housing Finance Authority (Aa1/AA+//) $339.3 million of non-AMT social single-family mortgage revenue bonds, Series 2024-146A, with 3.875s of 10/2034 at par, 4.125s of 10/2039 at 4.17%, 4.5s of 10/2044 at 4.56%, 4.75s of 4/2053 at par and 6.25s of 10/2054 at 3.90%, callable 10/1/2033.

Wells Fargo priced for the National Finance Authority, New Hampshire, (A2///) $266.112 million of social municipal certificates, Series 2024-3, Class A, with 4.163s of 10/2041 at 4.588%.

Ramirez priced for the State of New York Mortgage Agency (Aa1///) $140 million of social homeowner mortgage revenue bonds. The first tranche, $89.975 million of non-AMT bonds, Series 261, saw all bonds price at par: 4s of 10/2039, 4.4s of 2044, 4.55s of 2049 and 4.65s of 2054, callable 10/1/2033.

The second tranche, $30.025 million of AMT bonds, Series 262, saw all bonds price at par: 3.65s of 4/2025, 4.05s of 4/2029, 4.1s of 10/2029, 4.4s of 4/2034, 4.4s of 10/2034 and 4.45s of 10/2036, callable 10/1/2033.

The third tranche, $20 million of taxables, Series 263, saw 6.25s of 10/2054 at 5.263%, callable 10/1/2033.

J.P. Morgan priced for Lakeland, Florida, (A2///) $137.865 million of fixed-mode Lakeland Regional Health System hospital revenue refunding bonds, Series 2024, with 5s of 11/2036 at 3.51%, 5s of 2039 at 3.62%, 5s of 2044 at 3.99% and 5s of 2045 at 4.02%, callable 11/15/2034.

Jefferies priced for the Metropolitan Pier and Park Authority (/A/BBB+/AA-/) $101.105 million of 4s of 12/2026 at 3.16%, 5s of 12/2030 at 3.33%, 5s of 12/2034 at 3.42%, 5s of 12/2038 at 3.64% and 5s of 6/2053 at 4.24%, callable 6/15/2034.

In the competitive market, Richmond, Virginia, (Aa1/AA+/AAA/) sold $129.725 million of GO public improvement bonds, Series 2024C, to Truist Securities, with 3/2030 at 2.84%, 5s of 2034 at 2.88%, 5s of 2039 at 3.16%, 4s of 2044 at 3.93%, 3.5s of 2049 at 4.10%, 4s of 2054 at 4.10% and 4s of 2057 at 4.18%, callable 3/1/2034.

Muni CUSIP requests rise

Municipal CUSIP request volume rose in June on a year-over-year basis, following an increase in May, according to CUSIP Global Services.

For municipal bonds specifically, there was a decrease of 5.0% month-over-month, but a 8.5% increase year-over-year.

For the specific category of municipal bond identifier requests, there was a decrease of 14.7% month-over-month and requests are up 7.4% on a year-over-year basis.

New York led state-level municipal request volume with a total of 217 new CUSIP requests in June, followed by Texas (133) and California (96).

AAA scales

Refinitiv MMD’s scale was cut up to two basis points: The one-year was at 2.88% (unch) and 2.85% (unch) in two years. The five-year was at 2.75% (unch), the 10-year at 2.80% (+2) and the 30-year at 3.68% (+2) at 3 p.m.

The ICE AAA yield curve was little changed: 2.90% (unch) in 2025 and 2.86% (-2) in 2026. The five-year was at 2.76% (unch), the 10-year was at 2.81% (unch) and the 30-year was at 3.67% (+1) at 3:30 p.m.

The S&P Global Market Intelligence municipal curve was narrowly mixed: The one-year was at 2.90% (-1) in 2025 and 2.88% (unch) in 2026. The five-year was at 2.77% (-1), the 10-year was at 2.82% (+2) and the 30-year yield was at 3.67% (+3) at 3 p.m.

Bloomberg BVAL was cut one basis point out long: 2.94% (unch) in 2025 and 2.89% (unch) in 2026. The five-year at 2.80% (unch), the 10-year at 2.79% (unch) and the 30-year at 3.68% (+1) at 3:30 p.m.

Treasuries were mixed.

The two-year UST was yielding 4.416% (-7), the three-year was at 4.246% (-2), the five-year at 4.153% (flat), the 10-year at 4.275% (+3), the 20-year at 4.623% (+6) and the 30-year at 4.534% (+6) at 3:30 p.m.

Primary to come

The Black Belt Energy Gas District is set to price $600 million of gas project revenue bonds, 2024 Series C. Goldman Sachs.

Galveston, Texas, (/A/A-/) is set to price Thursday $160 million of Wharves and Terminal first lien revenue bonds, consisting of $111.525 million of Series 2024A, and $48.475 million of Series 2024B. Piper Sandler & Co.

The South Carolina Jobs Economic Development Authority (/AA/AA-/) is set to price Thursday $141.13 million of McLeod Health Project healthcare revenue refunding bonds, Series 2024. J.P. Morgan.

The Wisconsin Public Finance Authority (Aa3///) is set to price Thursday $120 million of tax-exempt pooled securities, Series 2024-2, Class A certificates. J.P. Morgan.