Municipals were little changed Tuesday as U.S. Treasuries were firmer and equities were mixed toward the end of the session.

Muni yields remain near levels seen at the start of summer last year, said Tom Kozlik, managing director and head of public policy and municipal strategy at HilltopSecurities.

Yields may move lower after the Federal Reserve “communicates its goals to

Munis also “show spreading good news, noting recently stronger mutual fund inflows, persistently solid SMA demand, and falling yields despite the strong pace of tax-exempt issuance,” said Matt Fabian, a partner at Municipal Market Analytics.

Issuance is at $277.228 billion year-to-date, up 3.13% year-over-year, according to LSEG.

As August approaches, issuance will slow as market participants enjoy summer vacation, said Chris Brigati, senior vice president and director of strategic planning and fixed-income research at SWBC.

This, and lighter supply because of the November election, will mean muni paper won’t see “significant cheapening,” he said.

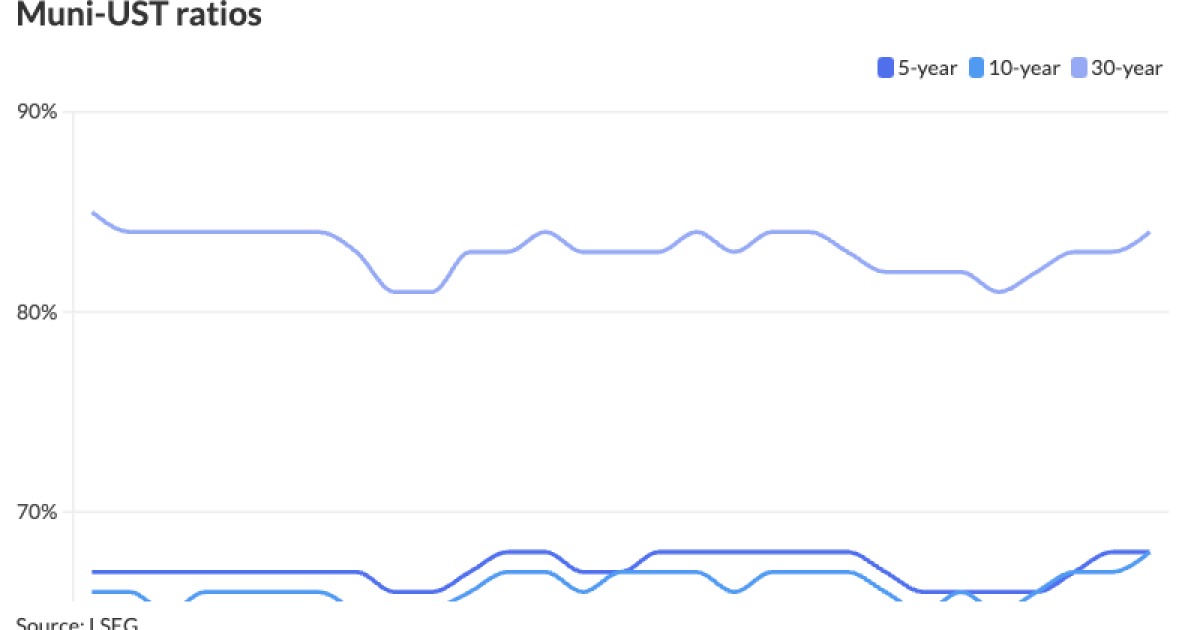

The two-year muni-to-Treasury ratio Tuesday was at 65%, the three-year at 67%, the five-year at 68%, the 10-year at 68% and the 30-year at 84%, according to Refinitiv Municipal Market Data’s 3 p.m. EST read. ICE Data Services had the two-year at 64%, the three-year at 66%, the five-year at 68%, the 10-year at 68% and the 30-year at 83% at 3:30 p.m.

Muni ratios “remain tethered to levels that fail to inspire attractive buying opportunities,” Brigati said.

The “strongest demand” for munis has been in the form of flows into institutional muni funds, though this is still not “deep, consistent demand” from 2021, Kozlik said.

“The next demand-phase could be an acceleration of demand as rate easing expectations grow,” he said. “The way the 2024 supply and demand dynamic is shaping up and the potential path lower for interest rates both further strengthen the argument for tax-exempt municipals.”

Along with recent inflows, demand remains robust due to the “steady” reinvestment monies for SMA portfolios, Brigati said.

Over the last three weeks, inflows into muni mutual funds and exchange-traded funds, according to LSEG Lipper, show “gains by long and high yield strategies, helping boost NAV performance in the latter,” Fabian said.

“These are the reasonable areas of opportunity left by otherwise pervasive [separately managed account] buying”: last week’s trade counts were greater than 250,000, Fabian said.

July is the 12th consecutive month with more than one million total trades, he said.

Recent “rough equity price volatility” should benefit retail muni allocations, Fabian said.

Another positive is the beginning of August, which will see the last “major surge” of reinvestment dollars in 2024, he said.

“Our sector’s challenge will be keeping SMA buyer interest if yields and available income begin to shrink via fund inflows or any rally coming out of this week’s Fed meeting and/or jobs data,” he said.

In the primary market Tuesday, Wells Fargo priced for institutions

The second tranche, $24.275 million of Fiscal Series 2025 B, saw 5s of 8/2025 at 3.00% (-1) and 5s of 2029 at 2.99% (-2), make whole call.

BofA Securities priced for the Port of Portland (/AA-/AA-/) $589.6 million of AMT Portland International Airport revenue bonds. The first tranche, $518.425 million of green bonds, Series 2024A, saw 5s of 7/2029 at 3.49%, 5s of 2034 at 3.74%, 5s of 2039 at 3.88%, 5.25s of 2044 at 4.13%, 5.25s of 2049 at 4.29% and 5.25s of 2054 at 4.35%, callable 7/1/2034.

The second tranche, $71.195 million of Series 2024B, saw 5s of 7/2025 at 3.49%, 5s of 2029 at 3.49%, 5s of 2034 at 3.74%, 5s of 2039 at 3.88% and 5.25s of 2044 at 4.13%, callable 7/1/2034.

J.P. Morgan priced for the Industrial Development Authority of Fairfax County, Virginia, (Aa2/AA+//) $368.245 million of Inova Health System Project healthcare revenue, Series 2024, with 5s of 5/2032 at 3.12%, 5s of 2051 at 4.06% and 4.125s of 2054 at 4.31%, callable 5/15/2034.

J.P. Morgan priced for the Central Florida Expressway Authority (A1/AA-//) $366.515 million of Assured Guaranty-insured senior lien revenue bonds. The first tranche, $148.185 million of Series 2024A, saw 5s of 7/2025 at 2.98%, 5s of 2029 at 2.95%, 5s of 2034 at 3.18%, 5s of 2039 at 3.33%, 5s of 2044 at 3.71%, 5s of 2049 at 3.95% and 5s of 2054 at 4.06%, callable 7/1/2034.

The second tranche, $218.33 million of Series 2024B, saw 5s of 7/2029 at 2.95%, 5s of 2034 at 3.18% and 5s of 2035 at 3.21%, callable 7/1/2034.

BofA Securities priced for the Illinois Housing Development Authority (Aaa///) $324.335 million of taxable social revenue bonds, Series 2024F, with all bonds pricing at par — 4.806s of 10/2025, 4.613s of 10/2029, 5.139s of 4/2034, 5.219s of 10/2034, 5.439s of 10/239 and 5.903s of 10/2054 — except for 6.25s of 10/2054 at 5.223%.

In the competitive market, Miami-Dade County, Florida, (Aa2/AA//) sold $234.96 million of capital asset acquisition special obligation bonds, Series 2024A, with 5s of 4/2027 at 2.97%, 5s of 2029 at 2.95%, 5s of 2034 at 3.12%, 5s of 2039 at 3.41%, 5s of 2044 at 3.80%, 5s of 2048 at 3.96% and 5s of 2054 at 4.10%, callable 4/1/2033.

AAA scales

Refinitiv MMD’s scale was unchanged: The one-year was at 2.86% and 2.85% in two years. The five-year was at 2.75%, the 10-year at 2.82% and the 30-year at 3.68% at 3 p.m.

The ICE AAA yield curve was narrowly mixed: 2.89% (-1) in 2025 and 2.84% (-2) in 2026. The five-year was at 2.76% (-1), the 10-year was at 2.81% (unch) and the 30-year was at 3.66% (+2. at 3:30 p.m.

The S&P Global Market Intelligence municipal curve was little changed: The one-year was at 2.89% (unch) in 2025 and 2.87% (unch) in 2026. The five-year was at 2.77% (unch), the 10-year was at 2.81% (unch) and the 30-year yield was at 3.64% (-1) at 3 p.m.

Bloomberg BVAL was unchanged: 2.88% in 2025 and 2.83% in 2026. The five-year at 2.74%, the 10-year at 2.76% and the 30-year at 3.65% at 3:30 p.m.

Treasuries were firmer.

The two-year UST was yielding 4.357% (-3), the three-year was at 4.172% (-2), the five-year at 4.036% (-2), the 10-year at 4.142% (-2), the 20-year at 4.494% (-2) and the 30-year at 4.399% (-2) at 3:30 p.m.

Primary to come

The Port of Seattle (A1/AA-/AA-/) is set to price Thursday $822.225 million of intermediate lien revenue refunding bonds, consisting of $170.825 million of non-AMT bonds, Series 2024A, serials 2025-2044, and $651.4 million of AMT bonds, Series 2024B, serials 2025-2044, term 2049. BofA Securities.

Tallahassee, Florida, (Aa3/AA//) is set to price Thursday $201.295 million of energy system refunding revenue bonds, Series 2024, serials 2025-2042. Raymond James.

The Fayette County Development Authority, Georgia, (//BBB/) is set to price Thursday

The Detroit Regional Convention Facility Authority (/A+/AA-/) is set to price Thursday $107.98 million of convention facility special tax revenue refunding bonds, Series 2024C. J.P. Morgan.

Competitive

New Orleans is set to sell $183 million of public improvement bonds, Issue of 2024A, at 10:30 a.m. Eastern Wednesday.

Glendale, California, is set to sell $166.88 million of electric revenue bonds, 2024 Second Series, at 11 a.m. Eastern Thursday.