Let’s play make-believe. Imagine you’re a youngish person working in or around British politics. You’ve got a degree in economics or something similarly impractical from a fancy university. And you’ve secured a great gig doling out advice to a minister who has no background in finance.

You project smartness, but this has its downsides. For instance, your new employer assumes you’ve got some insight into how the bond market works, and what on earth it is saying about the state of the world. No sweat. FTAV is here to help you out.

We’ll unpick the mystery of why yields drive prices (the author will die on this hill), help you read a yield curve, explain why Europe is different, work through duration, auctions, and maybe even swaps. Moreover, we’ll offer some handy hints to explain these concepts to your minister. By the time you’re done you’ll have all you need to be the life and soul of any party policy briefing. Most importantly, we’re going to try to do this without just becoming Investopedia on a pink background. Onwards!

What even is a bond?

OK, so this is probably not a question that a minister will ask out loud. But it’s best not to assume anything. So start with the super-super basics.

A bond is an IOU, issued by a thing (a government, an organisation, a firm, a special purpose vehicle) that promises to pay the holder a set of cash payments sometime in the future. After the IOU has been created it can be bought and sold between other parties.

Let’s look at an example. We’ll start simple.

The UK government borrows money every Friday in its weekly T-bill auctions. T-bills are basically super-short-term zero-coupon bonds. Prospective buyers rock up and submit bids for bills in a blind auction. They say how many bills they want to buy for a given yield. The government wants to borrow as cheaply as possible so accept bids first from those who offer to lend at the lowest yield, then from the folks offering the second lowest yield, etc. A couple of Fridays ago it borrowed £2.5bn at yields between 4.67 per cent and 4.74 per cent, with an average accepted yield of 4.725 per cent.

Yields up, prices down, yada yada yada

You’ll notice that bids are submitted for *yields* rather than prices. This is because yields are the only sensible way to think about bond valuations.

What’s a bond yield? It’s the compound annualised return that an investor will receive on their bond if they hold it until it matures (with a bunch of assumptions about reinvesting coupons that we needn’t go into because we’ve started looking at a security that doesn’t have coupons). By looking through the yield end of the price-yield telescope, investors can quickly look at a huge variety of different securities with different maturities, coupons, and prices, to help establish which one they want to buy or sell to maximise their return.

The price, in contrast, is determined by the magic of bond maths from the yield, maturity date (the point at which the bond is redeemed), current and settlement dates, as well as coupon periodicity and day count convention. It’s something that falls out the end of a bond calculator when you pop in the yield number. If it’s your job to code bond calculators, the maths is important. If it’s your job to code bond calculators, you should probably stop reading and get on with other things.

We’re starting simple, and T-bills are as simple as they come. No coupons, just a lump of money (the price) that grows (or, when negative interest rates rule, shrinks) into another lump of money (the redemption value).

The redemption value for 100 units or ‘nominal’ of UK T-bills is £100. And despite submitting bids for T-bills in the form of a yield, you do actually have to pay a price to execute the trade. What price? Let’s pop the yield into Bloomberg’s bond calculator to work this out.

As we mentioned above, one unfortunate soul had their bid filled at a yield of 4.67 per cent. This works out at a price of £97.724.

At the other end of the scale, a lucky (or savvier) punter had their 4.74 per cent bid accepted. And this turns out to be a price of £97.691.

Two important points here.

First, a lower yield means a higher price. Why? Because — working backwards from the fixed £100 redemption value — the amount of return you’re going to get by sending £97.724 now and receiving £100 back in six months will be lower than if you sent off *only* £97.691.

Second is that — despite our sniping — the gap between £97.691 and £97.724 is not very large. In fact, given that wags go wild when bond yields move by 7 basis points (aka 0.07 percentage points), it seems a pretty microscopic price difference.

The lack of meaningful price difference is largely because the T-bill matures in just six months, which is not a lot of time in bond land. The time to maturity being very low makes the price-sensitivity to yield movements very small.

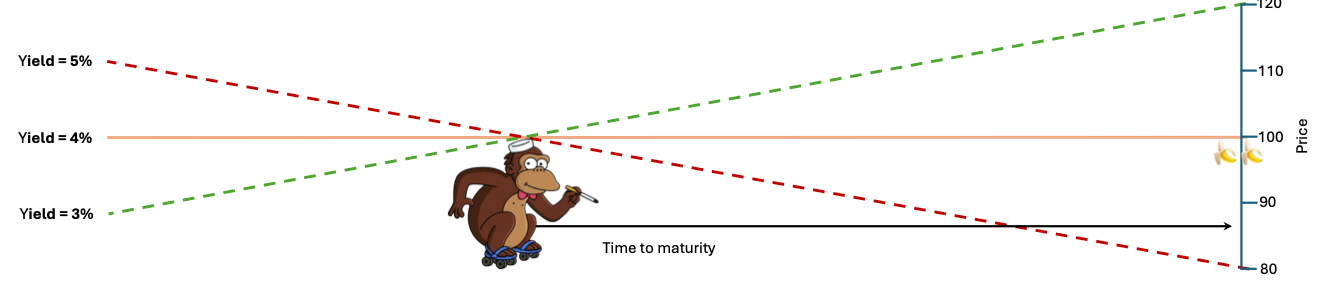

Rate chimps

This is all getting a bit dull detailed. As you relate basic bond maths to your minister you notice that they’ve drifted off to sleep. So to liven it up it’s time to wheel in Mr Teeny Bondzo the rates monkey and wake them up.

Imagine a bond is issued at par (aka, 100) with a coupon of 4 per cent. What is the price of this bond when the yield is 4 per cent? Drawing a line between left and right y-axes so that it just shaves Bondzo’s head, we can see that the answer is 100.

(High-res)

With Bondzo so far away from his bananas, a fall in the bond yield to 3 per cent would push the bond price to 120 (green dashed line). 🍾🍾🍾 And a rise in the yield to 5 per cent would push the price down to 80 (red dashed line). 😢😢😢

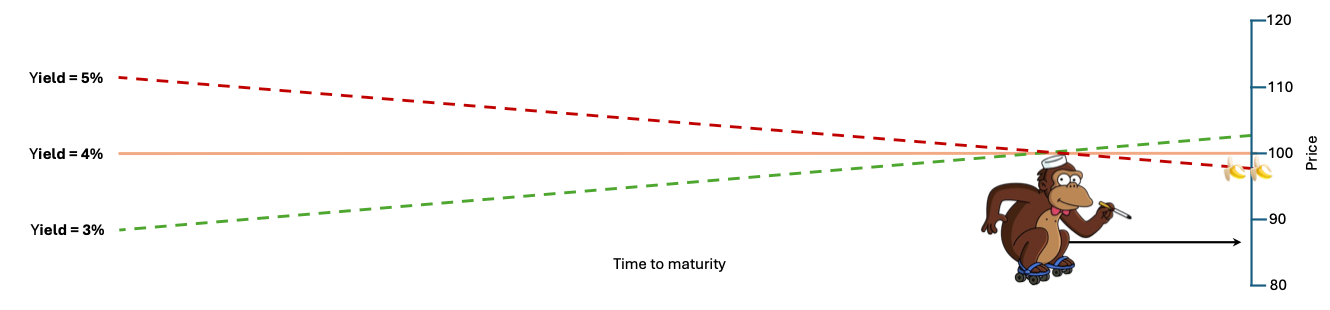

But when Bondzo is close to his bananas it’s a different story. Price and yield still move in opposite directions, but the magnitude of the price moves is meh, unless leveraged to the moon.

(High-res)

When we’re talking T-bills, Bondzo can almost taste his bananas.

Bond nerds will recognise our tale of Bondzo as a cunning ruse not only to explain the whole price-yield relationship, but also the concept of ‘duration’. If they were human they would congratulate us, but because they are pedants they will point to the omission of convexity from this elegant explainer.

Better than cash?

Right, so you’ve seen how a bill auction works, understood how prices and yields are linked, and have conveyed an idea to your minister about how the magnitude of price movements is greater when a fixed income security’s duration is higher, and also how this magnitude diminishes as time ticks forward and a bond approaches redemption through the not-at-all-patronising medium of a cartoon chimp.

But we haven’t yet touched on why a bond’s yield might be 3 per cent or 5 per cent. Why did I even bid 4.7 per cent for my 6 month IOU, aka Treasury Bill? And having bought it, at what price can I sell it if I don’t want to hold it to maturity?

Your minister thinks they know — they read something about a Moron Premium. Calm them. To answer these questions, we really need to chat yield curves.

Rather than announce that you’re going to chat yield curves and risk your minister being called away for an urgent meeting (again), you pose a very simple question: why hold (short-dated) bonds or bills over cash?

If you’re a bank in the UK, you can earn Bank Rate on your excess reserves. Bank Rate is set by the Bank of England’s Monetary Policy Committee who raise it or lower it in the belief that doing so impacts the economy. Although contested, most people reckon that raising Bank Rate slows the economy, pushing inflation down, and cutting Bank Rate boosts spending, pushing inflation higher.

Let’s imagine a bank, Southern Stone, that reckons the MPC will slash rates from 5 per cent to zero in six months’ time. Southern Stone has access to Bank Rate and a lump of money that it is *completely* happy to tie up for the next year. Should it:

a) Receive Bank Rate for the next twelve months (paying 5 per cent for six months and 0 per cent for six months);

b) Lock in the option to receive 4.7 per cent for 12 months?

The answer is b). In fact, it’s so obviously b) that we can infer that Southern Stone’s view that the MPC will slash rates to zero is wildly non-consensus. What is the consensus? We can unpick it from the yields available in the market.

There are a bunch of complex mathematical models built by quants to answer the question as to what exactly is implied about the forward path of rates from current market prices. But minister, we can get most of the way there by using a bit of common sense.

But here’s a chart showing the set of rates you could essentially lock in by extending the term of your ‘deposit’ at a particular point in time (using Monday’s values). We’re showing the SONIA OIS – the Sterling Overnight Index Average Overnight Index Swap rate – curve that is referenced by over £90 trillion of transactions each year, and described by the Bank of England as the risk-free rate. It basically tracks Bank Rate, but is a few basis points lower for reasons. We’re going to pretend that its relationship to Bank Rate is fixed, and it’s a perfect proxy for rate expectations. Bond nerds can shout at us for doing so in the comments.

Click through the charts below and you’ll see that knowing the value of one-month and two-month SONIA rates tells you where the value of one-month SONIA rate is expected to be in one month’s time – the so-called 1mth1mth forward OIS. And we can bootstrap a series of one-month SONIA rates forward over the next year.

The Bank of England MPC only meets on certain dates, and if we assume that rates are unchanged between meetings, we can interpolate the market’s expectation as to where rate decisions will come out.

With these few lines sketched on a graph the dark magic can begin. Stronger employment data and better economic growth? Maybe the economy doesn’t need so many interest rate cuts: yields up! Services inflation comes in weaker than expected? Yields down as faster cuts are priced in. The Bank comes out with a surprisingly hawkish statement that is in complete contrast to any sensible reading of the economic data? Maybe short-term yields higher, and longer-term yields lower to price a hike and recantation? You sense the bond market flowing through your minister’s veins now. Their spirit animal has been awakened.

Gilts, finally

It has taken us a long time to get here. And your minister is ready to drink it in. Behold… the gilt curve! (Musical suggestion.)

The gilt curve stretches out a full fifty years. To be fair, so does the SONIA curve. Confusingly, gilts have been trading at a positive spread to SONIA OIS for a few years, but let’s brush past that now and hope that they don’t get you to go through this longish explainer we wrote a while back.

While people get hot and bothered about the extent to which longer-term gilts have much to do with expectations around monetary policy, they are certainly linked. The yields of two-year bonds can overwhelmingly be understood as derived from folks’ guesses around the course of future central bank policy. Here’s a chart of the two-year benchmark gilt and Bank Rate to prove it.

It’s almost always the case that when the two-year yield is above Base Rate the expectation in markets is for the BoE to be raising rates, and when it’s below it’s almost always the case that the expectation priced into markets is for cuts to come.

Yields beyond the two-year tenor? Adding on the five-year and ten-year yields to the chart shows that – sure, the policy rate is sort of important – but also that it’s by far the be-all and end-all of bond valuation:

While the short-end of the curve is anchored by expectations around monetary policy, the longer part of the curve is more about vibes (and market segmentation, which is a fancy way of saying that some people just want or need to buy bonds at different parts of the curve).

After the vaguely mathsy stuff, vibes sound more fun. The minister might even stay awake for the next part without the need for a roller-skating monkey.

R-star as lodestar

Prince among vibes is the fabled R-star, aka the natural rate of interest, aka the neutral rate. In Robin’s words, R-star is:

the “neutral” level of interest rates that neither stimulates or contracts the economy, and thus keeps both unemployment and inflation in equilibrium.

So it’s a reasonable guess as to where interest rates will be after everything we know about the current economic cycle has washed out.

Unfortunately, R-star is unobservable. Central bankers love to quote economist John Williams, who in 1931 invoked James 2:17-20 to describe R-star as “an abstraction; like faith, it is seen by its works”. Maybe because he makes it sound mysterious, cerebral, a bit poetic, and not at all like an unfalsifiable conjecture that has fallen out of a textbook.

But the questions of what the right level for R-star might be, what shapes it, and whether it is even real, are something about which central bankers, economists and bond types can spend a fair chunk of their lives. Central bankers because it’s sort of their job. Economists, because it’s nerdy. But bond types? Because maybe having an idea as to the level around which central bankers will wiggle interest rates to prod the economy stronger or weaker over the next thirty years could help with their question as to whether thirty-year bond yields are too high or too low.

In the US, Federal Reserve rate-setters’ expectations for their longer-term neutral rate is part of their quarterly communications by dataviz — the long-term dot of the so-called dot plot. We can compare the median Fed voter’s expectation for long-term rates to the 30 year Treasury yield (with all the caveats about USTs not being the same as SOFR swap rates etc), and you can see that they haven’t actually been that closely related. Although they’re sort of in the same ballpark.

What about creditworthiness?

“This is all very well, and probably of interest to City-types,” complains the minister. “But if there’s one thing I know it’s that gilt yields are now far higher than Bund yields. And that means that we’d better slash spending or risk a Greek meltdown.”

No, no, no.

Greece defaulted after racking up more government debt than they were willing to service. And when investors started worrying about Italy following Greece down the road towards default they absolutely did freak out, dumping bonds – pushing their yields up and their prices down. Lacking control of the European Central Bank, the Greek government could — and did — run out of euros. Creditworthiness in Europe is key.

Today, it’s not at all a silly idea to compare the yields of BTPs (Italian sovereign bonds) and Bunds (German sovereign bonds), taking the ‘spread’ as a measure of the market’s estimation of Italian creditworthiness. A larger gap between Italian and German bond yields suggested greater concern on the part of bondholders that Italy won’t be good for their debts.

Moreover, bond spreads are a pretty good way to assess the relative concerns that bond markets have about creditworthiness across private borrowers.

So given the ever-higher mountains of government debt accrued by UK and US governments, why can’t we compare UK or US bond yields to German bond yields to get a sense of UK or US government creditworthiness in the same way?

Intuitive as this sounds, doing so would be very silly.

Italian and German government bonds are both issued in euros, and as such there is some connection between their yields and the short-term interest rate anchor set by the European Central Bank. Just like the SONIA curve we built out and linked to Bank of England rate expectations, there’s a curve in the Eurozone linked to ECB rate expectations, and a curve in the US linked to expectations around the Fed’s future moves. Interrogating bond yields across different currency regimes for information pertaining to creditworthiness gets very complicated very quickly. You really just can’t compare a gilt to a Bund and hope to come up with a sensible inference about creditworthiness.

But this isn’t to say that yield shifts in other bond markets are unimportant. As this next chart shows, ten-year bond yields tend to move together across major developed markets — maybe linked by some global R-star vibe, or synchronicity in the developments of interconnected economies. Or, perhaps, just linked by being part of a common palette of investments for bondholders.

Are rising yields bad?

“Let’s get down to brass tacks” says your minister. “Are rising bond yields good or bad?”

Pretty much everyone involved gets a bit stressed by rising bond yields — both bondholders and bond issuers. How can rising yields be bad for both? It’s a jam today versus jam tomorrow thing.

If you own bonds and yields are rising, the prices of your bonds are falling. So if owning bonds is your way to make a quick buck, rising yields are a bad thing. But if you don’t yet own bonds, rising yields offer the chance to lock in better future returns.

If you have issued bonds and their yields rise/ prices fall on secondary markets, you may not care — especially if you don’t intend to repay the old bonds with new bonds. But for everyone else who needs to issue fresh bonds to repay maturing ones (like the, erm, UK government), rising bond yields will translate into higher coupons being set on the new debt. From this perspective, rising yields look like a bad thing.

“Well, you could’ve saved a lot of time by saying rising yields are bad,” the minister complains.

Hmm. While there are all sorts of downsides to rising yields, we’ve got to remember that bond market investors are making judgments about the temperature of the economy. If yields are rising because the market is pricing out a previous expectation that the world is doomed to be trapped in a disinflationary or deflationary slump, is that really bad?

More sellers than buyers

“So rising bond yields are actually a good thing — the market giving a big thumbs-up to our plans for growth? Maybe we’ve all been too hard on Liz Truss after all?”

Let’s not get carried away.

Signalling that she would increase the DMO’s remit by £72.4bn to debt-fund the largest package of unfunded tax cuts in half a century, Liz Truss’s ‘mini-Budget’ was not bondholder friendly. It probably wasn’t so much the additional supply that pushed yields higher. Launching a major fiscal expansion during a period of double-digit inflation that central banks everywhere were still increasing policy rates to fight raised the prospect of the Treasury forcing the Bank to increase short-term policy rates still higher than they were otherwise heading.

You can see how the market repriced the path for short rates higher by hitting the play button on the animated chart below. The 12mth rate rose around 90 basis points between the day before the mini-Budget and the day before the Bank of England intervened as the market moved to price in aggressive hikes to offset the boost that would be given by the new deficit-spend to inflation. Bank Rate was only 2.25% at the time.

Yields on longer-dated bonds rose also. Remember, price movements on longer-dated bonds move much much more for a given yield movement. And with pension funds levered into longer-dated bonds, the rise in longer-date yields triggered margin calls among pension funds, forcing them to sell, pushing up yields, forcing others to sell etc. This spiralled out of control.

Did notions of R-star enter anyone’s head during the mayhem? Probably not.

Is it safe?

Time for the trillion pound question: is the market primed to flip out when the chancellor gives her Budget on 30 October? How febrile is it? Or, in ministerial terms, “Will I still have a job next month?”

Short answer, it’s almost certainly going to be fine. Slightly less flippant short answer, call a bond strategist. This little explainer has hopefully equipped you with some basics but we haven’t really gotten into too much nuance.

We will, however, leave you with a way to keep an eye on the health or otherwise of UK government bond auctions, both impressing your minister, and sating your newfound need for fixed income.

Remember way back at the beginning of this post when we covered last Friday’s Treasury Bill auction? The average yield accepted was 4.724634 per cent, but some fortunate punter had their bid of 4.74 per cent accepted? The difference between the average accepted yield and the highest accepted yield is called the “yield tail”, and in this case it was 0.01537 per cent, aka 1.537 basis points.

We can chart the length of the yield tails on DMO auctions over time. In the week after the Bank intervened to stop LDImageddon there was a sloppy auction of 0.5 per cent 2061 gilts with a 4 basis point tail. Click through the slides below and you’ll see that this pales in comparison to the kind of market febrility seen in the darkest days of the global financial crisis.

Where does this leave us today? Tails are between 1-2 basis points, which is 1-2 basis points longer than the DMO would ideally like, but not in scary territory.

So there we have it. If not quite everything you and your minister need to know to work out what the bond market is thinking, enough to ask some of the right questions, parry the tough ones and know when you can ignore the sound and fury of the gilt market. Good luck!

* * * S T O P P R E S S * * *

Update, please disregard everything you’ve read. FTAV has worked out how to generate an animation of our roller-skating rates monkey. This should answer all possible questions. Ends/

{kind=link}

{kind=link}