Municipal bonds were little changed to slightly firmer on the short end Friday after a week in which the longer end of the yield curve brought yields back to early July levels, with pressure from more supply and a weaker U.S. Treasury market.

UST yields reversed their negative course with the 10-year falling seven basis points and the 30-year five but munis were mostly flat as participants sat on the sidelines. Municipal to UST ratios were at 71% in 10-years and 76% in 30.

The short end of the muni market saw heavier trading with larger blocks at or below benchmarks. Massachusetts 5s of 2022 traded at 0.06%. Georgia 5s of 2022 at 0.04%. Texas 5s of 2022 at 0.05%. Louisiana 5s of 2022 at 0.07%. Maryland DOT 5s of 2022 at 0.06%. North Carolina 5s of 2022 at 0.06%. New York Urban Development Corp. 5s of 2022 at 0.06%. New York City 5s of 2022 at 0.06%.

Investors await the increase of supply, which New York issuers lead the calendar, pegged at $9.76 billion. The New York Liberty Development Corp. (/A/A-/) set to price $1.225 billion of 4 World Trade Center Project tax-exempt liberty revenue refunding green bonds and New York City (Aa2/AA/AA-/AA+) comes with $1.289 billion of exempt and taxable general obligation bonds.

Fitch Ratings moved the city to stable from negative on Friday afternoon ahead of its sale.

“We reiterate our market underperform on New York City’s General Obligation bonds (Aa2/AA/AA-) because current tight spreads are not sufficient compensation for risks to the city’s economic recovery,” according to a report from CreditSights. “The city’s finances are in better shape than expected, despite the pandemic, due to extraordinary federal aid and above-budgeted revenue performance.”

Miami-Dade County, Florida brings the largest ever deal for the Port of Miami with $1.24 billion of seaport revenue and refunding bonds. New Orleans (/A+//) leads the competitive slate with $300 million of exempt and taxable public improvement bonds on Wednesday.

While there was some pressure on yields this week, BofA Securities sees “no sign, or reason, that credit spreads should widen.”

“We see room for more compression to come for the rest of 2021,” strategists Yingchen Li and Ian Rogow wrote in a weekly report. “Macro conditions remain supportive of credit strengthening, and muni market supply/demand conditions provide no room for widening as the pressure is still on the tightening direction.”

“The flatness of A-rated and BBB-rated spreads only indicates that muni investors are probably searching for spread with their new money in other corners of the market, such as high-yield or investment-grade low-coupon bonds,” they said.

Muni CUSIP requests see first drop since January

Monthly municipal CUSIP request volume decreased in July, the first monthly decline since January of this year. The aggregate total of all municipal securities — including municipal bonds, long-term and short-term notes, and commercial paper — fell 18.7% versus June totals. On an annualized basis, municipal CUSIP identifier request volumes were up 4.2% through July. For muni bonds specifically, there was a decrease in request volumes of 18.2% month-over-month, but they are still up 9.9% on a year-over-year basis

“Municipalities have been busy with new debt issuance this year, and while the volume of new requests has slowed this month, it’s important to note that seasonality could be playing a role in the trend,” said Gerard Faulkner, direct of operations for CUSIP Global Services. “June is peak short-term notes season, so it stands to reason that we’d see a tough comparison in July. With interest rates still holding at historic lows and state governments very much in need of cash flow, we expect issuance volume to stay healthy for the near term.”

CUSIP identifier requests for the broad category of U.S. and Canadian corporate equity and debt edged higher in July versus June totals. The monthly increase was driven largely by medium-term note and Canadian corporate issuance. On a year-over-year basis, corporate CUSIP request volume was down 1.3%.

Benchmark yield curves

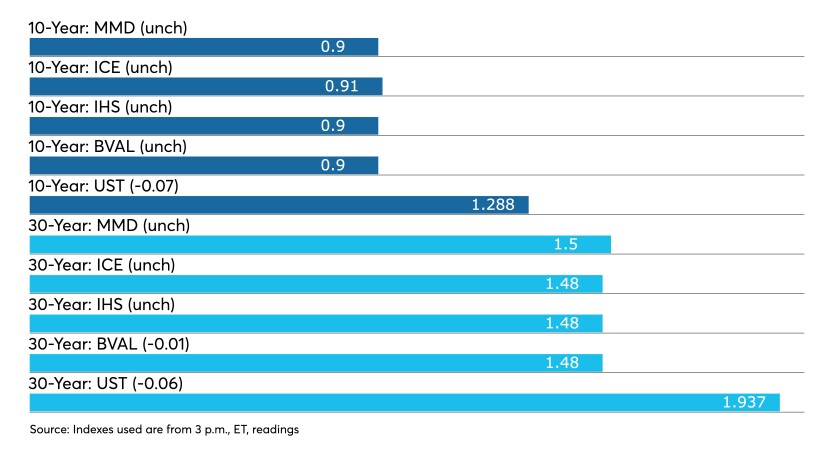

Refinitiv MMD saw levels steady at 0.06% in 2022 and at 0.08% in 2023. The yield on the 10-year steady at 0.88% while the yield on the 30-year sat at 1.50%.

ICE municipal yield curve saw steady at 0.06% in 2022 and at 0.08% in 2023. The 10-year maturity was at 0.91% and the 30-year yield sat at 1.48%.

The IHS Markit municipal analytics curve saw the one-year steady at 0.07% and the two-year at 0.08%, with the 10-year steady at 0.90%, and the 30-year yield at 1.48%.

Bloomberg BVAL saw levels at 0.06% in 2022 and 0.06% in 2023, while the 10-year stayed at 0.90% and the 30-year at 1.48%.

Treasuries fell while equities were mixed. The 10-year Treasury was yielding 1.295% and the 30-year Treasury was yielding 1.945% in late trading. The Dow Jones Industrial Average lost 20 points or 0.06%, the S&P 500 rose 0.06% while the Nasdaq lost 0.03% near the close.

Economic Indicators

The University of Michigan’s preliminary August consumer sentiment index dropped to 70.2 from the final read of July at 81.2.

The preliminary current economic conditions fell to 77.9 from July’s final read of 84.5 and the preliminary expectations index decreased to 65.2 from the final read in July of 79.0.

This marks the lowest reading for current conditions since 2011.

“After the second highest increase in consumer spending since the 1950s in the second quarter, the surge in COVID cases and concomitant sudden deterioration in consumer sentiment to its lowest level since 2011 threatens to slow what was on track to be the best year of economic growth in decades. Our sense is that while activity is moderating, this one-off report overstates the downside risk,” according to Tim Quinlan, senior economist and Sara Cotsakis, economic analysts at Wells Fargo Securities.

Economists polled by IFR Markets estimated a reading of 81.2 for sentiment. IFR expected current conditions to come in at 88.1 and expectations at 80.3.

“Although there has been a divergence recently between this measure and the comparatively sanguine readings of confidence from the Conference Board, the message here is a direct one: the one-two punch of inflation and a COVID resurgence threaten to disrupt the consumer-led economic expansion,” they said.

Also released Friday, import prices gained 0.3% in July after an upwardly revised 1.1% climb in June, originally reported as a 1.0% increase, while exports rose 1.3% in July after an unrevised revised 1.2% jump a month prior.

Economists anticipated imports to rise 0.6% and exports to gain 0.8%.

Primary to come

The New York Liberty Development Corp. (/A/A-/) is set to price $1.225 billion of taxable 4 World Trade Center Project tax-exempt liberty revenue refunding green bonds on Wednesday. Goldman Sachs & Co. LLC.

New York City (Aa2/AA/AA-/AA+) is set to price on Wednesday $1.039 billion of exempt general obligation bonds, $950 million of fiscal 2022 Series A, serials 2023-2025, 2031-2050 and $89.325 million of reoffering exempts, 2026-3030. Citigroup Global Markets Inc.

New York City is also set to sell $250 million of taxable GOs at 10:45 a.m. Wednesday.

Miami-Dade County, Florida is set to price on Wednesday $202.14 million of series A-1 (A3//A/), serials 2040-2041, term 2046; $221.330 million of series A-2 (A3//A/), serial 2046, term 2050; $180.43 million of series B-1 (Aa3//AA-/), term 2046, 2050; $96.07 million of series B-2 (Aa3//AA-/), serial 2038-2041, term 2044; $383.23 million of series A-3 (A3//A/), serial 2023-2036, term 2040; and $159.325 million of series B-3 (Aa3//AA-/), serial 2025-2038. Wells Fargo Corporate & Investment Banking.

The Kansas Development Finance Authority (Aa3/A+//) is set to price on Tuesday $502.655 million of taxable revenue bonds, serials 2022-2036, term 2051. Citigroup Global Markets Inc.

The City of Houston (Aa3//AA/) is set to price on Tuesday $348.8 million of exempt and taxables consisting of: $179.78 million of public improvement refunding bonds, series 2021A; $166.455 million of taxable public improvement refunding bonds, series 2021B; and $2.565 million of certificates of obligation (Demolition Program), series 2021C. Mesirow Financial Inc.

The Pennsylvania Housing Finance Agency (Aa1/AA+//) is set to price on Wednesday $296.67 million of single-family mortgage revenue social bonds (non-AMT). BofA Securities.

The City of Aurora, Colorado (/AA+/AA+/) through its Utility Enterprise is set to price on Thursday $266.7 million of taxable first-lien water refunding revenue green bonds. Morgan Stanley & Co. LLC.

The California Statewide Communities Development Authority (/A-/A/) is set to price $196.285 million of Front Porch Communities and Services series 2021A revenue bonds on Thursday. BofA Securities.

The California Statewide Communities Development Authority (/A-/A/) is also set to price $109.61 million of taxable Front Porch Communities and Services series 2021A revenue bonds on Thursday. BofA Securities.

The Connecticut Health and Educational Facilities Authority (/BBB+/BBB+/) is set to price on Wednesday $193 million of Stamford Hospital Issue, Series M forward delivery revenue refunding bonds. Goldman Sachs & Co. LLC.

The Rhode Island Housing and Mortgage Finance Corp. (Aa1//AA+/) is set to price on Wednesday $172.455 million of exempt and taxable homeownership opportunity social bonds, $144.59 million exempt Series 75-A And $27.865 million of taxable series 75-T. Morgan Stanley & Co. LLC.

The CMFA Special Finance Agency VIII is set to price on Tuesday $149.76 million of Essential Housing Revenue Bonds, Series 2021A (Elan Huntington Beach), $99.280 million of 2021A-1 Senior Bonds, term 2056, and $50.48 million of 2021A-2 Junior Bonds, term 2047. Jefferies LLC.

The University of North Dakota (A1///) is set to price on Thursday $144.32 million of certificates of participation: $127,525 million of series A, serial 2024, 2027-2030, terms: 2032,2034,2036,2039,2041,2046,2051,2061 and $16.795 million of refunding series B, 2022-2034. Stifel, Nicolaus & Company, Inc.

The Metropolitan District, Hartford County, Connecticut (Aa3/AA//) is set to price on Wednesday $142.445 million of general obligation bonds: $129.53 million of GOs, series 2021A, serials 2022-2041; and $12.914 million of GO refunding forward deliver bonds, Issue of 2021, Series B, serials 2023-2033. Raymond James & Associates, Inc.

The Rhode Island Infrastructure Bank (/AAA/AAA/) is set to price $127.965 million of taxable State Revolving Fund Refunding Revenue Bonds, Series 2021A, (Master Trust), serials 2021-2044. Raymond James & Associates.

The Hays Consolidated Independent School District, Texas (Aaa///) (PSF guarantee) is set to price on Tuesday $125 million of unlimited tax school building bonds. FHN Financial Capital Markets.

The City of Carmel, Indiana Local Public Improvement Bond Bank is set to price $122 million of multipurpose bonds, $87.245 million of Series A (/AA//), serials 2024-2041, and $34.8 million of Series B refunding bonds, serials 2022-2041. Stifel, Nicolaus & Company, Inc.

The Iowa Finance Authority/Palm Beach County Health Facilities Authority (//BBB/) is set to price on Thursday $120.465 million of Lifespace Communities, Inc. revenue refunding bonds. Ziegler.

The Louisiana Energy and Power Authority (/AA//) is set to price $120.325 million of Power Project Revenue Refunding Bonds (LEPA Unit No. 1) Taxable Series 2021A. Assured Guaranty Municipal Corp. Raymond James & Associates, Inc.

The Oregon Housing and Community Services Department (Aa2///) is set to price on Tuesday $99 million of single-family mortgage revenue bonds. BofA Securities, New York

The City of Buena Park, California (/AA+//) is set to price on Tuesday $96.425 million of taxable pension obligation bonds, 2022-2036, term 2043. Stifel, Nicolaus & Company, Inc.