Municipal benchmark yields were steady to firmer by a basis point 10-years and out Thursday as U.S. Treasuries were stronger and equities sold off led by tech stocks.

The municipal primary dominated the day with several large deals pricing. The correction to higher yields over the past week is allowing investors to be more selective with credits. Chicago schools saw 10- to 20-basis point cuts from price talk circulated Tuesday, showing investors demanded more for the junk-rated credit now that all municipal yields have climbed into a higher range.

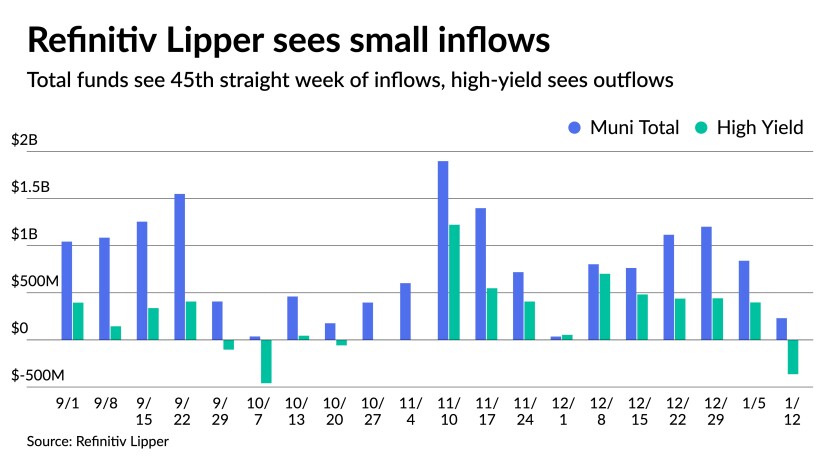

Fund flows back this up with Refinitiv Lipper reporting $231.1 million of inflows but $363.8 million of outflows from high-yield, the first since mid-October and the last correction, showing further indications that high-yield was hit hardest, creating more selective investor sentiment.

Municipal to UST ratios rose slightly on the day’s moves. The five-year was at 55%, 69% in 10 and 80% in 30, according to Refinitiv MMD’s 3 p.m. read. ICE Data Services had the five at 51%, the 10 at 71% and the 30 at 79%.

In the primary, Goldman Sachs priced for the Board of Education of the City of Chicago’s (/BB/BB+/BBB/) $866.12 million of dedicated revenue bonds.

It showed the first tranche, $500 million of unlimited tax general obligation bonds, with bonds maturing in 12/2042 with a 4% coupon at 2.88% versus 2.68% in price talk, 4s of 2043 at 2.91%, 5s of 2043 at 2.71%, 4s of 2047 at 3.00% versus 2.80% in price talk, and 5s of 2047 at 2.80%, callable 12/1/2031.

The second tranche, $366.12 million of unlimited tax general obligation revenue bonds, saw bonds maturing in 12/2022 with a 4% coupon yield 0.73%, 4s of 2035 at 2.54% (+10 from price talk), 4s of 2037 at 2.73% (+20) and 4s of 2041 at 2.85% (+20), callable 12/1/2031.

Final pricing was not yet available at press time.

Raymond James & Associates priced for Comal Independent School District in Texas (Aaa//AAA/) $418.865 million of unlimited tax school building bonds. Bonds in 2/2023 with a 4% coupon yield 0.32%, 5s of 2027 at 0.90%, 5s of 2032 at 1.35%, 4s of 2042 at 1.79%, 2.625s of 2047 at 2.65%, callable in 2/1/2031.

Barclays Capital Inc. priced for the Department of Water and Power of the City of Los Angeles (Aa2//AA-/AA/) priced $375 million of power system revenue bonds, 2022 Series A. Bonds maturing in 7/2027 with a 5% coupon yield 0.9%, 5s of 2032 at 1.29%, 5s of 2037 at 1.50%, 5s of 2042 at 1.68%, 5s of 2046 at 1.81% and 5s of 2051 at 1.85%, callable 7/1/2031.

J.P. Morgan Securities priced for the Rhode Island Housing and Mortgage Finance Corp. (Aa1/AA+///) $124.925 million of non-AMT homeownership opportunity social bonds. Bonds in 10/2026 with a 5% coupon yield 1.02%, 5s of 4/2027 at 1.09%, 5s of 10/2027 at 1.18%, 2.1s of 4/2032 at par, 2.15s of 10/2032 at par, 2.35s of 10/2036 at par, 2.55s of 10/2042 at par, callable in 4/1/2031; and 3s of 10/2051 at 1.51% (PAC bonds).

In the competitive markets, the Florida Board of Education (Aaa/AAA/AAA/) sold $159.78 million of public education capital outlay refunding bonds to BofA Securities. Bonds in 6/2023 with a 5% coupon yield 0.37%, 5s of 2027 at 0.94% and 5s of 2033 at 1.37%, noncall.

The Port of Seattle (Aaa/AA-/AA-/) sold $94.645 million of taxable, limited tax general obligation and refunding bonds to Raymond James & Associates. Bonds priced at par: 0.50% in 12/2022, 0.95% in 2023, 1.75% in 2027, 2.15% in 2032, 2.75% in 2037, 2.98% in 2041, callable in 12/1/2031.

Late Wednesday, Wells Fargo Bank priced for Louisiana (Aa2/AA-//) $642.79 million of gasoline and fuels tax revenue refunding bonds. The first tranche, $620.995 million of taxable bonds, 2022 Series A, saw bonds maturing in 5/2022 with a 0.723% coupon yields on par, 1.82s of 2027 on par, 2.401s of 2032 on par, 3.052s of 2038 on par and 2.952s of 2041 on par, callable 5/1/2032.

The second tranche, $21.795 million of tax-exempt bonds, 2022 Series B, saw bonds maturing in 5/2033 with a 5% coupon yields 1.54%, 4s of 2039 at 1.85% and 3s of 2041 at 2.27%, callable 5/1/2032.

It may seem like a slow start to the new year, but the overall pace of the municipal market is brisk, and Thursday’s firmer tone helped support secondary market activity and new-issue demand, according to a New York trader.

“I think the municipal market is still trying to get its feet under it with the new year starting; this is the first real week of any supply,” he said.

There is definitely improvement from earlier in the week, when municipal yields rose by three to six basis points on Monday on elevated selling pressure, while short U.S. Treasuries also saw pressure, he noted.

“I think munis are reacting positively to the firmer tone in Treasuries today,” he said, adding that investors don’t like “choppy” markets. “The recent volatility was definitely putting people on their heels.”

On the buy-side, municipals’ strong fundamentals and historical high quality is keeping the asset class supported as the first quarter gets under way, according to Joe Boyle, fixed income product manager at Hartford Funds.

While the previous strong demand that drove the municipal market in 2021 has waned slightly as the increase in individual taxes may be less severe than first expected, municipals continue to have a positive backdrop compared to the negative backdrop in other traditional fixed income classes on the back of rising rates, Boyle said.

“Muni markets relative to traditional core had a strong year and investors likely want to lock that in,” he said. “Demand for total return will exist in fixed income and investors are turning over every rock.”

CUSIP requests decline in December

The aggregate total of all municipal securities — including municipal bonds, long-term and short-term notes, and commercial paper — fell 10.6% in December versus November totals, according to CUSIP Global Services. On an annualized basis, total municipal CUSIP identifier request volumes were down 5.8% versus 2020 totals. For muni bonds specifically, there was a decline of 12.7% month-over-month and requests fell by 2.6% overall in 2021.

“Although municipal request volume has slowed year-over-year, we’ve still seen an incredibly strong appetite for new issuance among equity and debt market participants in 2021,” said Gerard Faulkner, director of operations for CUSIP Global Services. “The combination of a favorable interest rate environment and relatively healthy markets suggests this trend will continue through the early part of the New Year.”

Requests for new corporate identifiers, meanwhile, rose in December, helping total corporate CUSIP request volume edge higher in 2021 versus the previous year. CUSIP identifier requests for the broad category of U.S. and Canadian corporate equity and debt rose 11.9% versus November totals. The increase was driven largely by a surge in requests for U.S. medium-term notes. On a year-over-year basis, corporate CUSIP request volume rose 3.8% versus full year 2020 totals

Small inflows post-correction

In the week ended Jan. 12, weekly reporting tax-exempt mutual funds saw $231.121 million of inflows, Refinitiv Lipper said Thursday. It followed an inflow of $840.848 million in the previous week and marks the 45th consecutive week of inflows.

Exchange-traded muni funds reported inflows of $350.607 million, after inflows of $246.341 million in the previous week. Ex-ETFs, muni funds saw outflows of $119.485 million after inflows of $594.508 million in the prior week.

The four-week moving average fell to $847.635 million from $980.815 million in the previous week.

Long-term muni bond funds had inflows of $118.140 million in the latest week after inflows of $717.697 million in the previous week. Intermediate-term funds had inflows of $275.655 million after inflows of $224.168 million in the prior week.

National funds had inflows of $308.661 million after inflows of $826.058 million while high-yield muni funds reported outflows of $363.862 million in the latest week, after inflows of $398.025 million the previous week.

AAA scales

Refinitiv MMD’s scale was unchanged out to nine years and a basis point bump thereafter at the 3 p.m. read: the one-year at 0.33% and 0.46% in two years. The 10-year at 1.18% and the 30-year at 1.64%.

The ICE municipal yield curve showed yields were slightly firmer outside of 10-years: 0.32% in 2023 and 0.50% in 2024. The 10-year was steady at 1.22% and the 30-year yield was down one basis point to 1.64% in a 4 p.m. read.

The IHS Markit municipal analytics curve was unchanged: 0.34% in 2023 and 0.47% in 2024. The 10-year at 1.19% and the 30-year at 1.67% as of a 4 p.m. read.

Bloomberg BVAL was little changed save for out long: 0.33% in 2023 and 0.47% in 2024. The 10-year at 1.22% and the 30-year down one basis point to 1.65% at a 4 p.m. read.

Treasuries were better and equities sold off.

The five-year UST was yielding 1.467%, the 10-year yielding 1.698%, the 20-year at 2.102% and the 30-year Treasury was yielding 2.042% near the close. The Dow Jones Industrial Average lost 148 points or 0.41%, the S&P was down 1.26% while the Nasdaq lost 2.19% near the close.

More inflation data

While producer prices just missed most expectations, the numbers remain high, including the annual rise in the measure, which was the highest December to December climb in history.

PPI gained 0.2% in December and 9.7% year-over-year, while the November rise was revised up to a 1.0% jump from the initially reported 0.8% increase. Excluding food and energy, PPI rose 0.5% in the month after a 0.9% gain in November and is 8.3% higher than a year ago.

Economists polled by IFR Markets expected PPI to grow 0.4% in the month and 9.8% on an annual basis, while the core was seen climbing 0.5% in the month and 8.0% year-over-year.

“In the near-term continued supply bottlenecks and mounting labor and input costs are likely to continue to put upward pressure on prices, while the Omicron variant and associated surge in COVID-19 cases may further skew inflationary risks to the upside,” said Berenberg Capital Markets Chief Economist for the U.S. Americas and Asia Mickey Levy.

“There are some indications goods inflation is easing: on a three-month annualized basis durable goods prices rose 4.8%, a sharp decline from July’s 11.2%,” he said. But as supply issues ease and the pandemic dissipates, he expects demand for services will climb and “lead to a further moderation” of rising goods prices.

“Anecdotal evidence suggests sustained increases in labor and input costs are increasingly affecting businesses’ inflationary expectations and price setting behavior,” Levy said.

Most analysts expect inflation to slow later this year, as does Gary Schlossberg, global strategist, Wells Fargo Investment Institute. “However, the real test for the market is whether or not they will be satisfied with a disappointingly flat trajectory lower, as rents and other services prices pick up some of the slack from slowing goods costs,” he said.

Fed Gov. Lael Brainard, much like Fed Chair Jerome Powell, who testified on Tuesday before the Senate Banking Committee, “continued to reinforce a message of the Fed’s diligence toward inflation and employment,” said John Farawell, managing director and head of municipal trading at Roosevelt & Cross.

“Acknowledging these trying times for the economy she tried to communicate the central bank’s role in battling inflation and supply change issues in a non-partisan way. This wasn’t easy as politics seemed to continue to be part of some of the committee’s agenda.”

Despite the politics, he said, Brainard responded in “a competent manner.”

Bond yields, Farawell said, “will signal what the market thinks about the future economic trends and inflation.”

Inflation has become the second biggest concern of CEOs, according to The Conference Board, with 55% of surveyed executives saying they believe inflation will persist into 2023 and perhaps beyond.

Brainard said inflation is too high and the Fed is determined to reducing price pressures. “Our monetary policy is focused on getting inflation back down to 2% while sustaining a recovery that includes everyone,” she said. “This is our most important task.”

Sen. Pat Toomey (R-PA) noted Brainard opposed the easing of financial regulations and took an “activist role” in environmental issues. Brainard was also questioned by Sen. Thom Tillis (R-NC) about her contribution to Hillary Clinton’s presidential campaign, which he said didn’t mesh with the Fed’s independence. She responded, had she known Fed officials rarely make political contributions she would not have given the money.

“The most visible takeaway from Brainard’s remarks,” said Wells Fargo’s Schlossberg, “was the shift from promoting growth to containing inflation. The shift by one of the Board’s most dovish suggests greater unanimity in the policy tilt from growth to inflation control.

The bond market rallied, he said, “given the stronger commitment to controlling inflation,” while stocks slipped as investors’ expectations tilted “a degree or two toward more aggressive rate increases.”

But the Fed’s “hawkish slant” will be pressured, Schlossberg said, “both by an unfavorable combination of slowing growth and persistent inflation pressures, as the economy feels the brunt of the Omicron outbreak on the reopening and supply-chain disruptions.”

And Brainard’s comments could provide a “counterweight,” should President Biden’s nominees to fill the three empty Fed seats be dovish, as expected, he said, as they “will face resistance at the policy deliberations from a more hawkish rotation of bank presidents to the FOMC.”

Federal Reserve Bank of Philadelphia President Patrick Harker said he expects three rate hikes this year, beginning as early as March, and possibly a fourth if inflation continues at an elevated pace.

“The inescapable logical conclusion of this situation ― inflation higher than we want and a very robust jobs market ― is to tighten monetary policy,” he said according to prepared text of a speech released by the Fed. “I expect us to complete our taper of asset purchases by March. Then, we can probably expect a rate hike of 25 basis points. We could very well continue to raise rates throughout the year as the data evolve.”

Federal Reserve Bank of Richmond President Thomas Barkin hedged on when he expected liftoff, saying the Federal Open Market Committee “will be free to begin normalizing rates, should circumstances support that” once asset purchases end in March.

Inflation will determine the Fed’s moves, he said. “The closer that inflation comes back to target levels, the easier it will be to normalize rates at a measured pace,” Barkin added. “But were inflation to remain elevated and broad-based, we would need to take on normalization more aggressively.”

Also released Thursday, initial jobless claims rose to 230,000 on a seasonally adjusted basis in the week ended Jan. 8 from 207,000 a week earlier, while continuing claims fell to 1.559 million in the week ended Jan. 1 from 1.753 million a week earlier.

Economists expected 205,000 claims in the week.

“This may well be the first report suggesting Omicron is leading to new job loss,” said Mark Hamrick, senior economic analyst at Bankrate. “The future path of the pandemic remains highly uncertain, but the underlying job market narrative overall continues to be one of scarcity of available applicants and workers.”

Christine Albano contributed to this report.