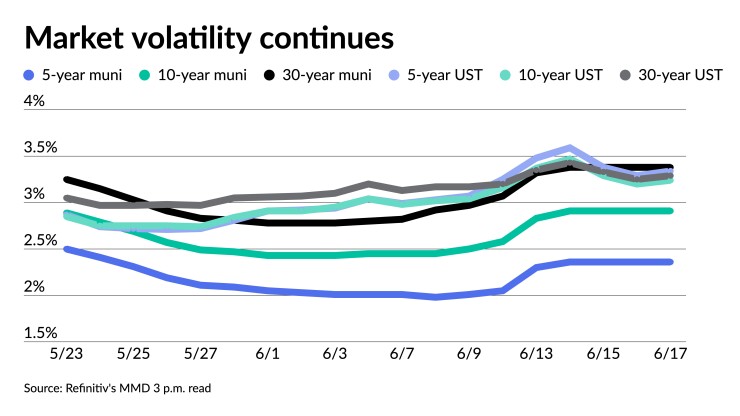

Municipals were little changed Friday after being swept along in a selling rampage at the start of the week, while U.S. Treasuries were weaker and equities were in the black.

Muni-to-UST ratios rose, with the 30-year topping 100% for the first time since late May. Ratios were at 71% in five years, 90% in 10 years and 103% in 30, according to Refinitiv MMD’s 3 p.m. read. ICE Data Services had the five at 71%, the 10 at 88% and the 30 at 101% at a 4 p.m. read.

Investors will be greeted Monday with an increase in supply with the new-issue calendar estimated at $6.398 billion in $3.629 billion of negotiated deals and $2.769 million of competitive loans.

The new-issue calendar for the week is led by $1.6 million of tax and revenue anticipation notes from Los Angeles, California, in a negotiated deal and $1.2 billion of general obligation bonds from gilt-edged Georgia in five competitive deals.

Other notable deals in the primary include $390 million of revenue bonds from the Department of Water and Power of the City of Los Angeles, California; $313 million from the National Finance Authority, New Hampshire, $300 million of taxables from the Fred Hutchinson Cancer Center, Washington; and $300 million of revenue bonds from the Commonwealth Transportation Fund, Virginia.

In the competitive market, Tarrant County College District, Texas, will sell $378 million of GOs and New Mexico brings $256 billion of revenue bonds.

Several issuers pulled deals after the massive selloff on Monday spooked issuers. Nassau County, New York, pulled its competitive loan and has placed it back on the calendar for Thursday.

“After a short-lived lull at the end of last month, rate volatility prior to the [Federal Open Market Committee] spiked to an extreme, and had a rather dramatic spillover effect into the municipal market, and the already weak market environment has become extremely challenging,” said Barclays strategists Mikhail Foux, Clare Pickering and Mayur Patel.

Nevertheless, they think “an even-keel approach is probably most appropriate this year.”

“We have not put much faith in the furious rally that started in late May, but we are also not panicking right now,” they said. “Clearly, summer months will be quite choppy, but rather than trimming exposure, we will be looking for opportunities to add on weakness, as tax-exempts have a lot of value at current yields.”

Nassau County, New York, pulled its competitive loan

Fund outflows, though, saw some of the largest in recent history this week, Barclays strategists said. Refinitiv Lipper reported Thursday $5.6 billion of outflows, the highest figure of outflows for 2022.

“Outflows will likely continue for some time although not at such a rapid pace as this week. Much will depend on how well new supply is received by investors when the pipeline starts growing later this summer,” according to Barclays PLC.

So far, issuance has been rather subdued in June with the 30-day visible pipeline rather benign for taxables and tax-exempts. Total issuance for the month as of Thursday was $13 billion, down 118.2% from $28.37 billion over the same time period in 2021. Bond Buyer 30-day visible supply sits at $11.81 billion.

However, they believe this lull won’t last.

Muni-UST ratios for “shorter maturities and even the belly of the curve are still well-below their fair values, not even talking about the highs reached in mid-May,” they said.

However, they noted, “the long end is getting much more attractive with the 10s30s curve at one of its steepest points in recent history — and this week investors are finally starting to take notice.”

Investors, though, should not rush. Barclays strategists aren’t sure the highs in ratios reached in May — 105% for 10-year and 110% for the 30-year — “will be revisited again, even though tax-exempts might still underperform near term, more so for shorter- and medium-term maturities.”

Moreover, high-quality, fixed-income investments, like munis, present opportunities going forward, as they “suddenly look very attractive,” Christian Hoffmann, portfolio manager at Thornburg Investment Management, based in Santa Fe, with $42 billion in client assets, said in a written statement following the FOMC meeting on Wednesday.

Hoffmann, who called the FOMC meeting “one of the most consequential in recent memory,” said the firm has its sights set on the long end of the fixed-income market.

“In our municipal bond portfolios, we are taking advantage of dislocations as well,” Hoffmann told The Bond Buyer.

“Flows have been exceptionally brutal this year, but at many points, this has provided remarkable relative value in fixed income,” including municipals, he said.

The FOMC decision arrived with little surprise and repositioning, Hoffmann said in his written comments.

“While we are aware of the headline risks, they do not drive our investment decisions,” Hoffmann wrote.

“A sky-high inflation report last week and ensuing violent market reaction forced the Fed’s hand to wager more on a larger rate hike.”

“The media flurry foreshadowing 75 basis points suggests the biggest risk is doing less and underwhelming the market,” he wrote.

“The market has had an outsized reaction to CPI last week, with reasonable potential to bounce from here in the short term or simply digest the large moves that have taken place,” Hoffmann added.

In his statement, Hoffmann said the market needs to appreciate the “invisible hand” at work.

“The two-year U.S. Treasury has moved by more than 300 bps in eight months; a huge move in housing affordability and mortgage rates; wealth destruction and bubbles popping; an erosion of CEO and consumer confidence—all of these measures perhaps not fully appreciated by the market,” he said.

So much as the Fed wants to help the market, it may be hurting the market, he noted.

“Unfortunately, the Fed’s precision with creating inflation appears to mirror its ability to tame inflation: weak, lagging and variable,” Hoffmann added.

“The last financial crisis was caused by investment banks, and the next one will be caused by central banks,” he said.

Still, Hoffmann’s base case is still for a recession going forward.

“I think the recession will be a mild variety of six to 10 months, but the notion of a slowdown is becoming more and more entrenched,” he wrote.

AAA scales

Refinitiv MMD’s scale was unchanged at the 3 p.m. read: the one-year at 1.72% and 2.06% in two years. The five-year at 2.36%, the 10-year at 2.91% and the 30-year at 3.38%.

The ICE municipal yield curve was bumped two basis points: 1.76% (-2) in 2023 and 2.07% (-2) in 2024. The five-year at 2.40% (-2), the 10-year was at 2.84% (-2) and the 30-year yield was at 3.34% (-2) at a 3 p.m. read.

The IHS Markit municipal curve was unchanged: 1.75% in 2023 and 2.09% in 2024. The five-year at 2.36%, the 10-year was at 2.92% and the 30-year yield was at 3.38% at 3 p.m.

Bloomberg BVAL saw was little changed: 1.75% (unch) in 2023 and 2.03% (unch) in 2024. The five-year at 2.37% (unch), the 10-year at 2.89% (unch) and the 30-year at 3.36% (-1) at a 3 p.m. read.

Treasuries ended weaker.

The two-year UST was yielding 3.172% (+7), the three-year was at 3.348% (+7), the five-year at 3.346% (+6), the seven-year 3.339% (+6), the 10-year yielding 3.241% (+4), the 20-year at 3.545% (+4) and the 30-year Treasury was yielding 3.290% (+4) at 3:30 p.m.

Primary to come:

Los Angeles, California, is set to price Thursday $1.572 billion of 2022 tax and revenue anticipation notes, serial 2023. Citigroup Global Markets.

The Los Angeles Department of Water and Power (Aa2//AA-/AA) is set to price Wednesday $390.085 million of power system revenue bonds, 2022 Series C, serials 2024-2035 and 2038-2043, terms 2047 and 2052. RBC Capital Markets.

The National Finance Authority, New Hampshire, (/BBB///) is set to price Wednesday $313.122 million of social municipal certificates, Series 2022-1 Class A and Class X, serial 2036 and Series 20221 Class X, serial 2036. Citigroup Global Markets Inc.

The Fred Hutchinson Cancer Center, Washington, (A2//A+/) is set to price Thursday $300 million of taxable corporate CUSIPs, Series 2022, term 2052. Barclays Capital.

The Commonwealth Transportation Fund, Massachusetts, (Aa1/AA+//AAA/) is set to price Wednesday $300 million of Rail Enhancement Program revenue bonds, consisting of $200 million of sustainability bonds, 2022 Series A, term 2050 and $100 million of bonds, 2022 Series B, term 2052. Wells Fargo Bank.

The Metropolitan Water District of Southern California (Aa1/AAA//) is set to price Wednesday $273.730 million of water revenue refunding bonds, 2022 Series A. Morgan Stanley & Co.

The Palm Beach County Health Facilities Authority, Florida, (/BBB-/BBB/) is set to price Thursday $164.745 million of Juniper Medical Center Project hospital revenue bonds, Series 2022, consisting of $140.235 million, Series A, serials 2028-2042, terms 2047 and 2052 and $24.510 million, Series B, serials 2028-2043. RBC Capital Markets.

Gallatin County, Montana, is set to price Thursday $160 million of taxable sustainability Bridger Aerospace Group Project industrial development revenue and revenue refunding, Series 2022. D.A. Davidson & Co.

Midland, Texas, (Aa1//AAA/) is set to price Wednesday $159.815 million of taxable general obligation refunding bonds, Series 2022A, serials 2022 and 2030-2050. Raymond James & Associates.

Charleston, South Carolina, (Aaa/AAA//) is set to price Wednesday $143.145 million of waterworks and sewer system capital improvement revenue bonds, Series 2022, serials 2026-2042, terms 2047 and 2052. Wells Fargo Bank.

Wisconsin (Aa1/AA+//AAA) is set to price Wednesday $134.370 million of SIMFA Index Rate general obligation floating rate notes of 2022, Series A. Goldman Sachs & Co.

Broward County, Florida, (A1///) is set to price Thursday $127.610 million of AMT port facilities revenue bonds, Series 2022, serials 2024-2052. RBC Capital Markets.

The Rockwall Independent School District, Texas, is set to price Thursday $114.615 million of unlimited tax school building bonds, Series 2022A. Piper Sandler & Co.

Competitive:

Tarrant County College District, Texas, is set to sell $377.500 million of general obligation bonds, Series 2022, at 10:30 a.m. eastern Tuesday.

Georgia (Aaa/AAA/AAA/) is set to sell $186.565 million of taxable general obligation bonds, Series 2022B, at 12 p.m. eastern Wednesday.

Georgia (Aaa/AAA/AAA/) is set to sell $221.930 million of tax-exempt general obligation refunding bonds, Series 2022C, Bidding Group 4, at 11:30 a.m. Wednesday.

Georgia (Aaa/AAA/AAA/) is set to sell $243.355 million of tax-exempt general obligation bonds, Series 2022A, Bidding Group 1, at 10 a.m. Wednesday.

Georgia (Aaa/AAA/AAA/) is set to sell $250.860 million of tax-exempt general obligation bonds, Series 2022A, Bidding Group 2, at 10:30 a.m. Wednesday.

Georgia (Aaa/AAA/AAA/) is set to sell $260.515 million of tax-exempt general obligation refunding bonds, Series 2022C, Bidding Group 3, at 11 a.m. Wednesday.

New Mexico (Aa2/AA-/) is set to sell $256.290 million of severance tax bonds, Series 2022A, at 9:45 a.m. Wednesday.

Nassau County, New York, (A1/AA-/A/) is set to sell $245.180 million of general obligations general improvement bonds, 2022 Series A, at 10 a.m. eastern Thursday.