Municipals were firmer in spots, while U.S. Treasury yields rose 10 years and in ahead of Wednesday’s consumer price index report. Equities ended mixed.

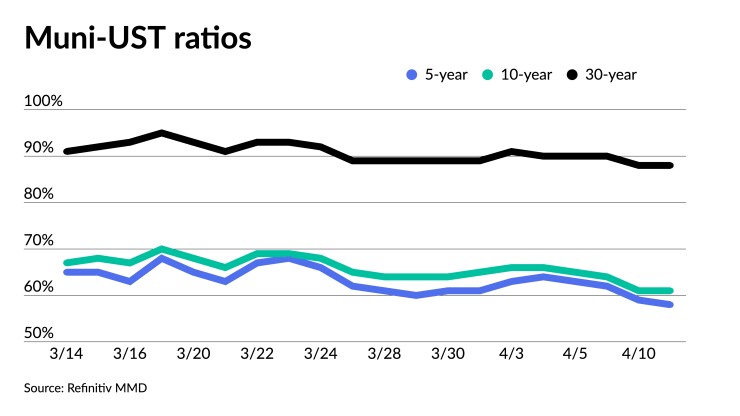

Triple-A yields were bumped up to three basis points Tuesday while UST yields rose up to two basis points 10 years and in, moving municipal-UST ratios near their 12-month lows, according to Refinitiv MMD.

The two-year muni-Treasury ratio was at 55%, the three-year at 56%, the five-year at 58%, the 10-year at 61% and the 30-year at 88%, according to Refinitiv MMD’s 3 p.m. ET read. ICE Data Services had the two-year at 57%, three-year at 56%, the five-year at 57%, the 10-year at 61% and the 30-year at 89% at 4 p.m.

Prior to Friday, “last week was mostly a good one for U.S. fixed income, yields falling on continuing expectations of slower growth,” said Matt Fabian, a partner at Municipal Market Analytics.

However, Friday’s solid jobs “reading pushed things in a different way, and U.S. Treasuries lost roughly half of their prior weekly gains, even if taxable yields still ended 4-8bps lower,” he said.

“Friday’s holiday, no MSRB trade reporting, and thin staffing meant a zero response from tax-exempt AAA benchmarks,” he said.

MMA’s Consensus curve, Fabian said, “ended the week 13-16bps better, the curve bull steepening slightly.”

Due to this outperformance through inaction, ratios were pushed “down to or through the lows of early March; the spread between offered-side 10yr taxable municipal to tax-exempt AAAs is only a few bps away from its peak widest,” he said.

“This could set a bias to weakness in municipal prices starting [this week], but constructive market technicals — solid positive price momentum — and fundamentals — still thin supply and stable if not robust demand — may not tolerate much of that,” he said.

On the demand side, both traditional funds and exchange-traded fund flows, “have slowed to a crawl one way or the other despite solid YTD gains in related fund NAVs,” he said.

Fabian said, “the lack of fund asset growth is also despite the apparently intensifying week-to-week volatility in flows into the 2a7 funds that has made a good case for short fixed rate allocations vis-à-vis the unpredictable SIFMA/7-day resets.”

The second half of 2023 may see a slowdown, perhaps even a mild recession, said Daniel Close, the newly named head of municipals at Nuveen.

When it comes to inflation, central banks are no longer lagging behind since monetary policy has “fully caught up,” he stated.

The market suggests the Fed may be somewhat overshooting at this stage, he said, given that two-year USTs are about 75 basis points below Fed funds.

“Inflation is no longer rising, but it’s still higher than Fed Chairman Jerome Powell and the Fed would like to see,” he said.

The consumer price index report on Wednesday will be crucial; the consensus predicts a 5.1% increase in headline inflation from the previous year. This will be the last CPI print before the May Federal Open Market Committee meeting.

Close anticipates another rate increase at the May meeting. The Fed has increased rates by 475 basis points this cycle.

Credit fundamentals remain very strong, according to Close, who notes munis have “historically done very well in slowdowns and recessionary periods given that these are essential service monopolistic providers.”

He said technicals remain favorable and supportive. There is net negative supply, “meaning more bonds are being called and more bonds are being matured than new-issue paper,” he said. Close sees this continuing to happen in the near-term future.

“You don’t see many other fixed-income classes with negative net supply,” he said. “But the biggest reason we’ve seen this negative net supply, especially for the last four years, is because issuance has been suppressed because of the Tax Cuts and Jobs Act.”

“What that says is that a meaningful component of our market is pre-refunded bonds, so now if a state or local government would like to go in and refund debt, they would have to do so on a taxable market,” Close continued. “As a result, we’ve seen supply suppressed for the last several years.”

In 2022, supply was down 21% year-over-year. This trend has continued into 2023, with the first three months of the year all seeing a dip in supply.

In the primary Tuesday, Citigroup Global Markets priced for the Los Angeles County Metropolitan Transportation Authority (Aa1/AAA/NR/NR/) $230.880 million of Proposition C senior sales tax revenue refunding bonds, Series 2023-A, with 5s of 7/2024 at 2.28%, 5s of 2028 at 2.02%, 5s of 2033 at 2.07% and 5s of 2038 at 2.68%, callable 7/1/2033.

Raymond James priced for the Texas City Independent School District (/AAA//) $131.390 million of unlimited tax school building bonds, Series 2023, with 5s of 8/2024 at 2.47%, 5s of 2028 at 2.20%, 5s of 2033 at 2.32%, 5s of 2038 at 2.94%, 4s of 2043 at 3.76%, 4s of 2048 at 3.98% and 4s of 2053 at 4.02%, callable 8/15/2032.

Secondary trading

California 5s of 2024 at 2.40% versus 2.43% Thursday. Wisconsin DOT 5s of 2024 at 2.48%-2.45%. Georgia 5s of 2025 at 2.29%.

NY Dorm PIT 5s of 2028 at 2.14%-2.13%. NYC 5s of 2029 at 2.10%. California 5s of 2029 at 2.16% versus 2.23% original on Thursday.

Wake County, North Carolina, 5s of 2031 at 2.05% versus 2.06% Monday and 2.25% original on 3/28. Tampa waters, Florida, 5s of 2033 at 2.13%. DC 5s of 2035 at 2.22%.

Denver, Colorado, 5s of 2039 at 2.80% versus 2.83% Monday. DC 5s of 2041 at 2.99% versus 3.02% Thursday and 3.24% on 3/30. California 5s of 2042 at 3.12%-3.13% versus 3.17%-3.16% Monday and 3.32%-3.29% original on Thursday.

AAA scales

Refinitiv MMD’s scale was bumped up to three basis points. The one-year was at 2.36% (-3) and 2.23% (-3) in two years. The five-year was at 2.06% (-2), the 10-year at 2.10% (unch) and the 30-year at 3.18% (unch) at 3 p.m.

The ICE AAA yield curve was bumped one to two basis points: 2.46% (-2) in 2024 and 2.32% (-2) in 2025. The five-year was at 2.03% (-2), the 10-year was at 2.08% (-2) and the 30-year was at 3.21% (-1) at 4 p.m.

The IHS Markit municipal curve was bumped up to two basis points: 2.37% (-2) in 2024 and 2.24% (-2) in 2025. The five-year was at 2.05% (-2), the 10-year was at 2.06% (-2) and the 30-year yield was at 3.17% (unch), according to a 4 p.m. read.

Bloomberg BVAL was bumped up to two basis points: 2.35% (-1) in 2024 and 2.27% (-1) in 2025. The five-year at 2.05% (-2), the 10-year at 2.09% (unch) and the 30-year at 3.17% (-1) at 4 p.m.

Treasuries were slightly weaker in spots.

The two-year UST was yielding 4.029% (+2), the three-year was at 3.791% (+2), the five-year at 3.537% (+1), the seven-year at 3.482% (+1), the 10-year at 3.428% (+1), the 20-year at 3.747% (flat) and the 30-year Treasury was yielding 3.623% (-1) at 4 p.m.

Primary to come

The California State Public Works Board (Aa3/A+/AA-/NR/) is set to price Wednesday $467.265 million of various capital projects lease revenue bonds, consisting of $51.245 million of new-money bonds, Series 2023A, serials 2023-2043, term 2047, and $416.020 million of refunding bonds, Series 2023B, serials 2023-2037. RBC Capital Markets.

The Irvine Facilities Financing Authority, California (/AA//) is set to price Wednesday $434.608 million of Build America Mutual-insured Irvine Great Park Infrastructure Project special tax revenue bonds, Series 2023A, consisting of $418.360 million of current interest bonds, serials 2026-2043, terms 2048, 2053 and 2058, and $16.248 million of capital appreciation bonds, serials 2049-2050, term 2045. Stifel, Nicolaus & Co.

The Idaho Housing and Finance Association (Aa1/NR/AA+/NR/) is set to price Wednesday $368.145 million of Transportation Expansion and Congestion Mitigation Fund bonds, Series 2023A, serials 2024-2043, term 2048. Citigroup Global Markets.

The Modesto Irrigation District Financing Authority, California (/A+/AA-/) is set to price Thursday $174.575 million of electric system revenue bonds, consisting of $126.575 million of new-money bonds, Series 2023A, and $48 million of refunding bonds, Series 2023B. Goldman Sachs.

Raleigh, North Carolina, is set to price Thursday $150.565 million of GOs, consisting of $145.835 million of public improvement bonds, Series 2023A, serials 2024-2043, and $4.730 million of taxable housing bonds, Series 2023B, serials 2024-2043. PNC Capital Markets.

The South San Francisco Unified School District (Aa1///) is set to price Wednesday $149.995 million of Election of 2022 GOs, Series 2023, serials 2024-2025 and 2033-2043, terms 2048 and 2052. RBC Capital Markets.

The Rhode Island Health and Educational Building Corp. (A2/A/NR/NR/) is set to price Wednesday $114.070 million of Providence College Issue higher education facility revenue bonds, Series 2023, serials 2025-2043, terms 2047 and 2053. Citigroup Global Markets.

The Ventura Unified School District, California (A1///), is set to price Thursday $113.000 of Election of 2022 GOs, Series A, serials 2024-2025 and 2032-2043, terms 2048 and 2052. RBC Capital Markets.

Competitive

Anne Arundel County, Maryland, (Aaa/AAA//) is set to sell $203.345 million of GOs, including $135.830 million of consolidated general improvement bonds, Series 2023, and $67.515 million of consolidated water and sewer bonds, Series 2023, at 10:45 a.m. eastern Wednesday.

The county is also set to sell $63.670 million of GOs, consisting of $41.405 million of refunding consolidated general improvement bonds, Series 2023, and $22.265 million of refunding consolidated water and sewer bonds, Series 2023, at 11:15 a.m. Wednesday.

Louisiana (Aa2/AA-//) is set to sell $251.105 million of GOs, Series 2023-A, at 10:15 a.m. eastern Thursday.

New Mexico is set to sell $233.320 million of capital projects GOs, Series 2023, at 10 a.m. Thursday.

Portland Public Schools, Oregon (Aa1/AA+//), is set to sell $230.775 million of GOs, Series 2023, Bidding Group 1, at 11 a.m. Thursday.

The school system is also set to sell $189.225 million of GOs, Series 2023, Bidding Group 2, at 11:15 a.m. Thursday.