Municipals were slightly firmer Tuesday as large deals priced in the primary saw yields lowered upon repricing. U.S. Treasuries were firmer out long and equities rallied.

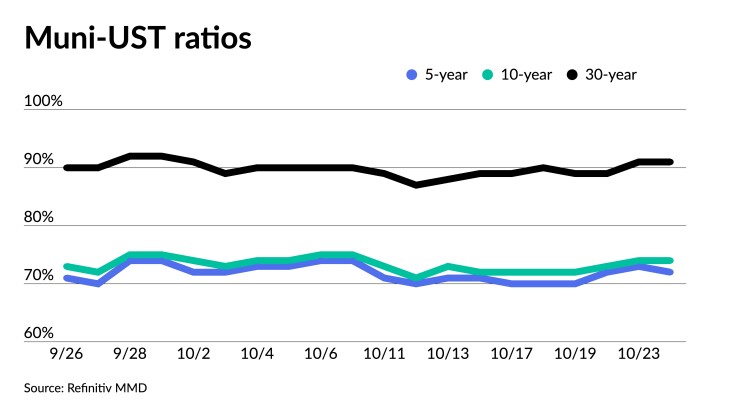

The two-year muni-to-Treasury ratio Tuesday was at 71%, the three-year was at 72%, the five-year at 72%, the 10-year at 74% and the 30-year at 91%, according to Refinitiv Municipal Market Data’s 3 p.m., ET, read. ICE Data Services had the two-year at 73%, the three-year at 74%, the five-year at 72%, the 10-year at 73% and the 30-year at 90% at 3:30 p.m.

Munis experienced some firmness Tuesday as triple-A yields were bumped up to three basis points, depending on the scale.

“Whether or not that’s going to be for more than a nanosecond remains to be seen,” said Jeff Lipton, managing director of credit research at Oppenheimer Inc.

October is not typically a well-performing month for munis, he noted.

Munis are returning negative 0.85% month-to-date but are outperforming the October UST selloff. USTs are returning negative 0.94% month-to-date, while corporates are in the red 1.74% month-to-date.

Year-to-date, all fixed-income cohorts are negative. Munis are moderately outperforming USTs, but both munis and USTs are underperforming corporates year-to-date. Bloomberg’s main muni index shows losses of 2.22% year to date.

“Although fixed income cohorts will very well end the year in the red, munis are likely to outperform,” Lipton said.

Net supply is at negative $8.8 billion, according to Bloomberg, compared to several weeks ago when the supply deficit was narrower. Bond Buyer 30-day visible supply sits at $10.75 billion.

“The supply deficit is on the rise, but I don’t believe that we are looking at a supply deficit that would likely have a dramatic impact to the positive on muni bond performance,” he said.

There could be some support, but he said the market needs stability to have fund flow conviction.

Beyond market volatility, the “story for the bond market” is November’s Federal Open Market Committee meeting next week, according to Lipton.

There is a “very de minimis probability” the Fed will hike rates 25 basis points, down from the 25% to 30% assumptions of a quarter-point rate hike a few weeks ago, he said.

Market participants are digesting the Fed’s “higher for longer” narrative, though Lipton points out there is more to the story.

If the “Fed comes to its natural conclusion of the current tightening cycle and the fed funds rate effectively stays where it is, one of the developments that has been supportive of higher bond yields is this idea that any pivot to an easing bias has been pushed deeper into 2024,” he said.

“It’s not necessarily the ‘higher for longer’ but for a good while market participants were looking for clear signals as to when the Fed was going to pivot,” he noted.

Even though there are cracks in the “economic veneer,” there’s still considerable economic resiliency.

Although the Fed’s tightening cycle has resulted in meaningful disinflationary progress, there’s more work to be done in terms of achieving price stability.

The Fed’s mantra has been to do everything to bring inflation down to 2%, but market participants — including Lipton — are wondering whether that 2% is realistic.

“Do we need to have 2% inflation, [or] can the economy function with 3% inflation?” he asked.

Inflation has been about cut in half from the beginning of the tightening cycle, he added.

Market stability has been scarce throughout 2023, with “stakeholders hanging on every word of Fedspeak, in search of the slightest policy clue pointing to the end of the central bank’s tightening cycle,” Lipton said.

They are also looking for what conditions need to be present for a pivot to occur, which appears to have been “pushed deeper” in 2024, he said.

If it had not been for that expectation, market stability “would likely be making more than just the cameo appearance,” Lipton said.

In the primary market Tuesday, Morgan Stanley priced and repriced for institutions $850 million of GO sustainability decided unlimited ad valorem property tax bonds, Series QRR (2023), for the Los Angeles Unified School District (Aa3//AAA/AAA/), with yields bumped up to five basis points from Monday’s retail pricing. The first tranche, $801.530 million of tax-exempt bonds, saw 5s of 7/2024 at 3.72% (-3), 5s of 2028 at 3.50% (-2), 5s of 2033 at 3.67% (-2), 5s of 2038 at 4.21% (-3), 5s of 2043 at 4.48% (-5) and 5.25s of 2048 at 4.67% (-2), callable 1/1/2034.

The second tranche, $48.470 million of taxables, saw 5.7s of 1/2024 price at par, noncall.

Goldman Sachs priced and repriced for institutions $738.485 million of green transmission project revenue bonds, Series 2023A, for the New York Power Authority, with yields bumped up to 11 basis points from Monday’s retail pricing: 5s of 11/2026 at 3.71% (-6), 5s of 2028 at 3.73% (-3), 5s of 2033 at 3.93% (-5), 5s of 2038 at 4.38% (-11), 5.25s of 2043 at 4.73% (-5), 5s of 2048 at 5.03% (-7), 5s of 2053 at 5.08% (-7), 5.125s of 2058 at 5.22% (-3) and 5.125s of 2063 at 5.30% (-5), callable 11/15/2033.

Jefferies priced for Chicago (/AA//) $515.500 million of Build America Mutual-insured senior lien airport revenue and revenue refunding bonds on behalf of the Chicago Midway Airport. The first tranche, $211.940 million of AMT bonds, Series 2023A, saw 5s of 1/2027 at 4.50%, 5s of 2028 at 4.53%, 5s of 2033 at 4.68%, 5.5s of 2038 at 4.98%, 5.75s of 2043 at 5.17%, 5.75s of 2048 at 5.29% and 5.5s of 2053 at 5.48%, callable 1/1/2033.

The second tranche, $303.560 million of non-AMT bonds, Series 2023B, saw 5s of 1/2025 at 4.00%. 5s of 2028 at 3.86%, 5s of 2033 at 4.12% and 5s of 2036 at 4.40%, callable 1/1/2033.

Wells Fargo Bank priced for the Pennsylvania Housing Finance Agency (Aa1/AA+//) $409.605 million of single family mortgage revenue bonds. The first tranche, $389.370 million of non-AMT social bonds, Series 2023-143A, saw all bonds price at par — 4.7s of 4/2034, 4.95s of 10/2038, 5.3s of 4/2044 and 5.375s of 10/2046 — except 6.25s of 10/2053 at 5.09%, callable 4/1/2033.

The second tranche, $20.235 million of taxables, Series 2023-143B, saw all bonds price at par: 6.381s of 10/2038 and 6.458s of 2043, callable 4/1/2033.

Jefferies priced and repriced for the Phoenix Civic Improvement Corp. (Aa2/AAA//) $383.810 million of junior lien wastewater system revenue bonds, Series 2023, with yields bumped up to 12 basis points from the preliminary pricing: 5s of 7/2028 at 3.57% (-9), 5s of 2033 at 3.77% (-7), 5s of 2038 at 4.27% (-12), 5s of 2043 at 4.63% (-5) and 5.25s of 2047 at 4.76% (-6), callable 7/1/2033.

In the competitive market, Fayetteville, North Carolina, (Aa2/AA/AA/), sold $171.105 million of Public Works Commission revenue bonds, Series 2023, to BofA Securities, with 5s of 3/2026 at 3.70%, 5s of 2028 at 3.57%, 5s of 2033 at 3.70%, 5s of 2038 at 4.31%, 5s of 2043 at 4.57%, 4.5s of 2049 at 4.85% and 5s of 2053 at 4.80%, callable 3/1/2033.

The Pinellas County School District, Florida, sold $100 million of tax anticipation notes to Wells Fargo Bank, with 5s of 6/2024 at 3.88%, noncall.

Secondary trading

California 5s of 2024 at 3.68%. Washington 5s of 2024 at 3.80% versus 3.80% Friday and 3.77% Thursday. Massachusetts 5s of 2025 at 3.70%.

Georgia 5s of 2028 at 3.51% versus 3.44%-3.42% on 10/4. Connecticut 5s of 2028 at 3.67%. North Carolina 5s of 2029 at 3.65%.

NY Dorm PIT 5s of 2032 at 3.79%-3.81% versus 3.78% Friday and 3.72% on 10/18. NYC 5s of 2033 at 3.89%. California 5s of 2034 at 3.80%-3.79% versus 3.79% Monday and 3.73% on 10/18.

Massachusetts 5s of 2049 at 4.79% versus 4.85% Friday. NYC 5s of 2051 at 5.03% versus 4.79% on 10/16. Metropolitan Water District of Southern California 5s of 2053 at 4.55%-4.53% versus 4.53% Monday and 4.29% on 10/16.

AAA scales

Refinitiv MMD’s scale was bumped up to two basis points: The one-year was at 3.76% (-2) and 3.65% (-2) in two years. The five-year was at 3.49% (-2), the 10-year at 3.59% (unch) and the 30-year at 4.53% (unch) at 3 p.m.

The ICE AAA yield curve was bumped one to three basis points: 3.71% (-3) in 2024 and 3.69% (-3) in 2025. The five-year was at 3.51% (-2), the 10-year was at 3.55% (-2) and the 30-year was at 4.55% (-1) at 3:30 p.m.

The S&P Global Market Intelligence municipal curve was bumped up to two basis points: The one-year was at 3.79% (-2) in 2024 and 3.69% (-2) in 2025. The five-year was at 3.54% (-2), the 10-year was at 3.60% (unch) and the 30-year yield was at 4.54% (unch), according to a 3 p.m. read.

Bloomberg BVAL was bumped one to two basis points: 3.79% (-2) in 2024 and 3.73% (-2) in 2025. The five-year at 3.51% (-2), the 10-year at 3.60% (-2) and the 30-year at 4.56% (-1) at 3:30 p.m.

Treasuries were firmer out long.

The two-year UST was yielding 5.102% (+3), the three-year was at 4.912% (+2), the five-year at 4.818% (+1), the 10-year at 4.826% (-3), the 20-year at 5.158% (-5) and the 30-year Treasury was yielding 4.940% (-7) at 3:45 p.m.

Primary to come

The New York Transportation Development Corp. (Baa3/BB+//) is set to price Wednesday $881.225 million of special facilities revenue bonds, Series 2023, for Delta Air Line’s LaGuardia Airport Terminals C&D Redevelopment Project, terms 2035, 2040. Citigroup Global Markets.

The Chicago Board of Education (/BB+/BB+/BBB/) is set to price Thursday $600 million of dedicated revenues unlimited tax GOs, Series 2023A. BofA Securities.

Freddie Mac (/AA+//) is set to price Wednesday $364.010 million of sustainability structured pass-through certificates, consisting of $182.005 million of Series ML-18, Class A, serial 2037; and $182.005 million of Series ML-18, Class X, serial 2037. Citigroup Global Markets.

Cape Coral, Florida (/AA//), is set to price this week $138.085 of BAM-insured North 1 West Area utility improvement assessment refunding. Morgan Stanley.

The Virginia Small Business Financing Authority (Aaa///) is set to price Wednesday $125 million of Pure Salmon Virginia Project environmental facilities revenue bonds, Series 2022, serial 2052. Wells Fargo Bank.

The Illinois Finance Authority is set to price Thursday $100 million of LRS Holdings Project solid waste disposal revenue bonds, consisting of $30 million of green bonds, Series 2023A, and $70 million of bonds, Series 2023B. J.P. Morgan.

Competitive

The California Public Works Board is set to sell $299.820 million of lease revenue bonds, 2023 Series D, at 11:30 a.m. Wednesday and $55.275 million of lease revenue bonds, 2023 Series E, at 11 a.m. Wednesday.

Minnesota (/AA+//) is set to sell $449.935 million of certificates of participation, Series 2023, at 11:15 a.m. Wednesday and $26.030 million of taxable State General Fund appropriation bonds, Series 2023A, at 11:30 a.m. Wednesday, and

Nevada (Aa1/AAA/AA+/) is set to sell $433.725 million of GO capital improvement bonds, Series 2023A, at 10:45 a.m. Wednesday; $29.415 million GO open space, parks and natural resources bonds, Series 2023C, at 11:30 a.m. Wednesday; $13.865 million of GO natural resources and open space bonds, Series 2023B, at 11:30 a.m. Wednesday; and $5.895 million of GO Safe Drinking Water Revolving Fund matching bonds, Series 2023D, at 10:45 a.m. Wednesday.

The Virginia Public School Authority (Aaa/AAA/AAA/) is set to price $134.600 million of special obligation school financing bonds, Series 2023, at 10:30 a.m. Thursday.

The Albermarle County Economic Development Authority (Aa1/AA+/AA+/) is set to sell $109.650 million of public facilities revenue bonds, Series 2023A, at 11 a.m. Thursday, and $59.195 million of taxable public facilities revenue notes, Series 2023B, at 10:15 a.m.