Municipals were firmer Thursday as muni mutual funds saw inflows top $1 billion and issuers were paid $26 billion of principal. U.S. Treasuries rallied and equities sold off.

Muni yields were bumped two to eight basis points, depending on the scale, while UST yields fell up to 13 basis points on the short end.

The two-year muni-to-Treasury ratio Thursday was at 67%, the three-year at 68%, the five-year at 70%, the 10-year at 69% and the 30-year at 85%, according to Refinitiv Municipal Market Data’s 3 p.m. EST read. ICE Data Services had the two-year at 65%, the three-year at 67%, the five-year at 68%, the 10-year at 68% and the 30-year at 83% at 3:30 p.m.

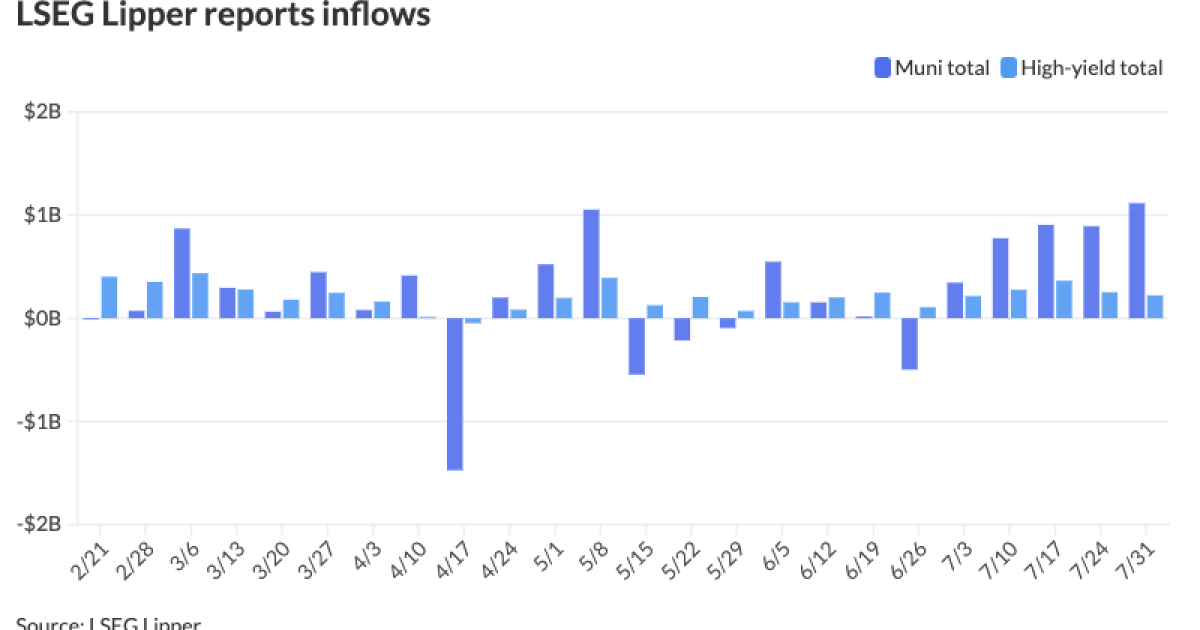

Municipal bond mutual funds saw inflows as investors added $1.112 billion to funds after $892.2 million of inflows the week prior, according to LSEG Lipper.

This is the second-largest amount of inflows into mutual funds this year. The largest was in the week ending January 31, when they hit $1.413 billion.

“Price performance that progressed through the first three weeks of July failed to show any further momentum into month-end, but the result was enough to move most municipal sectors back into the positive on a year-to-date basis,” said Kim Olsan, senior fixed income portfolio manager at NewSquare Capital.

Munis returned 0.91% in July, “which places it in the top four best results over the last year,” she said.

Positive performance for the month, pushed year-to-date returns into positive territory, seeing gains of 0.50%.

“High-yield munis posted a 1.10% return in July but has an impressive 5.28% gain in 2024 — the highest result of any U.S. fixed-income sector,” Olsan said.

“A combination of a healthy economy and risk tolerance has generated steady weekly flows into HY muni strategies,” she said.

Taxables “rode the UST wave in July, gaining 2.60% and beating out UST (+2.19%) and corporate bond (+2.38%) indices,” Olsan said.

“The supply effect, along with a UST rally, helped the sector — year-to-date issuance is down 17% from 2023 but could see a revival in coming months if rates rally further and opportunity develops for municipal refundings,” she said.

In August, muni investors will be paid $47 billion of principal, a 26-month high, and $14 billion of interest, an 18-month high, said Pat Luby, head of municipal strategy at CreditSights.

August 1 sees $26 billion of matured and called bond proceeds paid out to muni investors, along with $8 billion of interest, he said.

August’s redemptions will be the largest of 2024 for issuers in California, Texas and Maryland, he said.

“After August’s surge in redemptions, potential reinvestment demand will fall off sharply as the total amounts of bonds scheduled to mature or get called in each of the last four months of the year are lower than this year’s average,” Luby said.

In the primary market Thursday, BofA Securities priced for the Port of Seattle (A1/AA-/AA-/) $819.975 million of intermediate lien revenue refunding bonds. The first tranche, $169.79 million of non-AMT bonds, Series 2024A, saw 5s of 3/2025 at 2.94%, 5s of 2029 at 2.87%, 5s of 2034 at 3.05%, 5s of 2039 at 3.33% and 5s of 2040 at 3.40%, callable 3/1/2034.

The second tranche, $650.185 million of AMT bonds, Series 2024B, saw 5s of 7/2025 at 3.53%, 5s of 2029 at 3.58%, 5s of 2034 at 3.76%, 5.25s of 2039 at 3.93%, 5.25s of 2044 at 4.18% and 5.25s of 2049 at 4.30%, callable 7/1/2034.

Raymond James priced for Tallahassee, Florida, (Aa3/AA//) $199.19 million of energy system refunding revenue bonds, Series 2024, with 5s of 3/2025 at 2.95%, 5s of 2029 at 2.89%, 5s of 2034 at 3.10%, 5s of 2039 at 3.33% and 5s of 2042 at 3.62%, callable 10/1/2034.

J.P. Morgan priced for the Detroit Regional Convention Facility Authority (/A+/AA-/) $109.63 million of convention facility special tax revenue refunding bonds, Series 2024C, with with 5s of 10/2025 at 3.06%, 5s of 2029 at 3.09%, 5s of 2034 at 3.30% and 5s of 2039 at 3.48%, callable 10/1/2033.

In the competitive market, the Florida Department of Transportation (Aa2/AA/AA/) sold $220.17 million of turnpike revenue bonds, Series 2024C, with 5s of 7/2025 at 2.90%, 5s of 2029 at 2.80%, 5s of 2034 at 2.89%, 5s of 2039 at 3.19%, 4s of 2044 at 3.95% and 4s of 2049 at 4.02%, callable 7/1/2034.

Glendale, California, (/A+//) sold $166.685 million of electric revenue bonds, 2024 Second Series, to BofA Securities, with 5s of 2/2025 at 2.70%, 5s of 2029 at 2.58%, 5s of 2034 at 2.67%, 5s of 2039 at 2.93%, 5s of 2044 at 3.40% 5s of 2049 at 3.60% and 5s of 2054 at 3.73%, callable 2/1/2034.

AAA scales

Refinitiv MMD’s scale saw bumps: The one-year was at 2.83% (-3, no Aug roll) and 2.81% (-3, -1bp Aug roll) in two years. The five-year was at 2.69% (-6, no Aug roll), the 10-year at 2.76% (-6, no Aug roll) and the 30-year at 3.62% (-6) at 3 p.m.

The ICE AAA yield curve was bumped two to seven basis points: 2.86% (-2) in 2025 and 2.80% (-3) in 2026. The five-year was at 2.68% (-7), the 10-year was at 2.75% (-5) and the 30-year was at 3.59% (-4) at 3:30 p.m.

The S&P Global Market Intelligence municipal curve was bumped three to eight basis points: The one-year was at 2.85% (-3) in 2025 and 2.80% (-5) in 2026. The five-year was at 2.71% (-6), the 10-year was at 2.73% (-8) and the 30-year yield was at 3.58% (-6) at 3 p.m.

Bloomberg BVAL was bumped five to seven basis points: 2.82% (-5) in 2025 and 2.78% (-5) in 2026. The five-year at 2.68% (-6), the 10-year at 2.69% (-6) and the 30-year at 3.58% (-6) at 3:30 p.m.

Treasuries rallied.

The two-year UST was yielding 4.164% (-13), the three-year was at 3.974% (-13), the five-year at 3.850% (-11), the 10-year at 3.983% (-10), the 20-year at 4.351% (-8) and the 30-year at 4.274% (-8) at 3:40 p.m.

FOMC redux

Analysts are convinced the Federal Open Market Committee will consider a rate cut in September if data supports it, but few believe the outcome is set.

“It is important to note that the Fed has not at this time committed to a September rate cut,” said Wells Fargo Investment Institute economists. “In our opinion, upcoming jobs data and inflation reports will be key to the September decision. Stronger-than-expected employment reports and stronger-than-expected inflation data could put a September rate hike in doubt.”

“The Fed went to great lengths not to push back against [a September rate cut], but I’d also argue they didn’t say they are going to move in September,” said Jeff Klingelhofer, portfolio manager at Thornburg Investment Management. “I think they threaded the needle exactly like they were supposed to.”

He noted the plethora of data that will come in before the next meeting, and the potential for it to be stronger than expected.

“I think the data will continue to suggest we’re on a path to September,” Klingelhofer said. “I think that’s a policy mistake personally, but the Fed is likely to move that direction unless we get a significant data surprise on the positive angle — so either higher inflation or a much stronger job market than markets are expecting.”

He expects a “precautionary” cut in September, but, “from there they’re likely to disappoint the market in the sense that they’re going to move very progressively and cautiously with potential rate cuts being data-dependent.”

Fifty basis points is not an option next meeting, Klingelhofer said. “If we saw it, I think it would be a policy mistake because we’re very quickly forgetting where we’ve come from on the inflation side, we’re quickly forgetting how strong the underlying consumer is and the potential that inflation could come back.”

The market’s assurance of a September move “is wrongheaded,” he said. “I’m sure the Fed wants to cut, but there are still two inflation prints before September, so one bad piece of data could derail efforts.”

Calling the statement “significantly more dovish,” Jay Hatfield, CEO at Infrastructure Capital Advisors, believes the “Fed is behind the curve” and should have cut rates.

“The fact that the Fed has clearly signaled a September cut has caused 10-year bond yields to plunge by over 50bp, which should stabilize the housing market as 30-year mortgage rates decline,” Hatfield said. “The decline in rates should allow the U.S. to avoid a recession during this Fed tightening cycle as the housing sector has historically been the key driver of recessions.”

Andrew Husby, senior U.S. economist at BNP Paribas, noted Fed Chair Jerome Powell offered a “clearer signal” that if data cooperates, a 25-basis-point cut will come in September.

The FOMC “offered enough” to keep markets expecting a September easing of monetary policy, said ING Chief International economist James Knightley.

“Inflation is looking better behaved, the jobs market is softening and consumer spending is cooling,” he said, “and with the policy rate well above neutral, we look for 75bp of cuts this year with the potential for more in 2025.”

Joe Kalish, chief global macro strategist at Ned Davis Research, said “a 25 bp rate cut in September is ‘on the table.’ A 50 bp cut is not.”

He added, “Ten-year yields may have trouble making further progress without fundamental help.”

Data should be soft enough for a September move, said Brian Rose, senior U.S. economist at UBS Global Wealth Management, “but not so bad that they would want to cut at a more aggressive pace.” And he ruled out a rate hike.

Still, he noted, “risks are asymmetric.”

“Inflation data in line with expectations and labor market data that continues to soften but remain healthy will warrant cuts to normalize policy rate, which is understood to be restrictive at this point,” said Gibson Smith, founder and CIO of Smith Capital Investors.

Currently, he said, risks are balanced, “but as inflation continues to come down and the job market normalizes, focus is starting to shift to avoiding material degradation in job growth and the health of the economy.”

Supply and demand in the labor market “are back to better balance, cooling from overheated conditions but not concerning at this point,” Smith said.

The Fed “is in a good position to react” to further labor market softening, he said, “and will do so swiftly if necessary.”

Investors “should position for lower yields on a six- to 12-month horizon by keeping portfolio duration above-benchmark and by owning Treasury curve steepeners,” said Ryan Swift, U.S. bond strategist at BCA Research.

While the markets liked what they heard, Giuseppe Sette, president of Toggle AI, said, “they might be myopic. The historical track record is undeniable: the first rate cut by the Fed harbingers the peak of equity markets, and the beginning of the economic slowdown.”

“Confidence in cuts should encourage a [muni] curve rotation into longer maturity SMA strategies, and to a lesser extent, mutual funds,” Morgan Stanley economists said. “Tax-free money market yields could stay sideways to higher.”

Gary Siegel contributed to this report.