Investors digested three mammoth deals of $1 billion or more in the primary market on a heavy day of issuance as municipals remained unchanged, Treasuries were mostly steady, and more than $2.5 billion flowed into long-term municipal bonds.

The primary market activity was brisk Tuesday as all eyes turned to the Federal Open Market Committee’s July minutes for sentiment over a possible spike in inflation and answers to the debate over the end of the pandemic-era emergency programs.

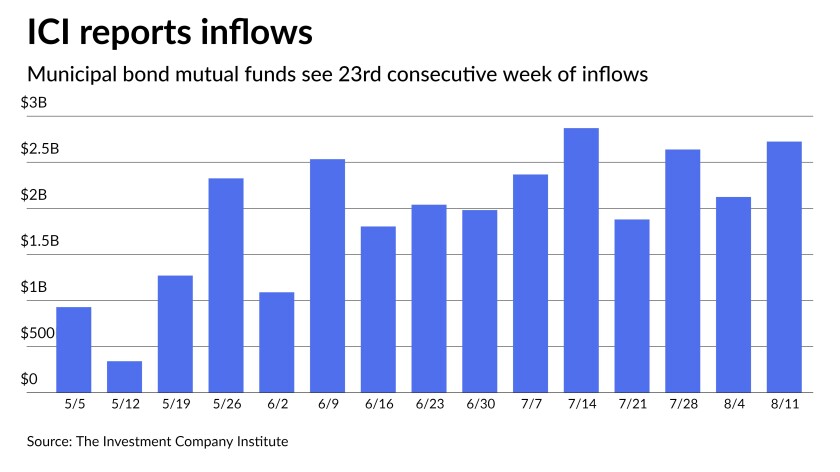

Long-term municipal bond funds and exchange-traded funds saw combined inflows of $2.724 billion in the week ended Aug. 11, the Investment Company Institute reported.

For a third day in a row this week, the benchmark triple-A general obligation bonds were unchanged from 2022 to 2051, according to Refinitiv Municipal Market Data.

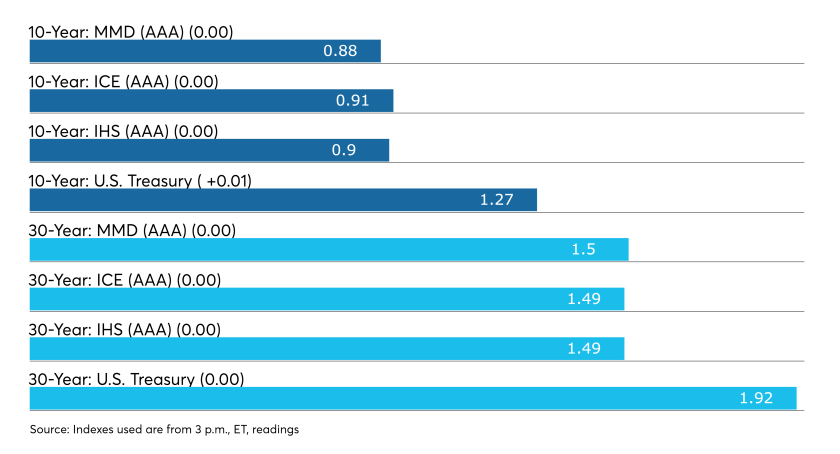

The U.S. Treasury benchmark ended at 1.272% in 10 years, which was two basis points weaker than at the close the prior day, and 1.913% in 30 years. The municipal to Treasury ratio ended at 69% in 10 years and 78% in 30 years.

“The lack of bid wanteds isn’t creating any weakness or strength,” a Florida trader said, noting that the Treasury auction of $27 billion of 20-year bonds at a yield of 1.85% was just one reason for the pressure on the short end.

“The Fed minutes are just another reason for the lack of secondary participation,” the trader said. “You have what feels like decent money in investors’ hands, but also a lot of patience due to the fear of inflation and rising rates,” he added.

The minutes from the central bank’s meeting revealed that Federal Reserve officials felt the employment benchmark for decreasing support for the economy “could be reached this year,” but had not yet been satisfied.

“Most participants anticipated that the economy would continue to make progress toward those goals,” the minutes said.

With Treasuries off a touch and a glut of billion-dollar deals pricing in the primary market, the short end traded sideways on Tuesday, he said.

The presence of billion-dollar deals from New York City, the New York Liberty Development Corporation, and Miami-Dade County, he said, were mostly to blame for the lethargy.

“The activity remains light in here,” the trader explained of the secondary market.

It is a “challenge” sourcing demand inside of five years, while demand is “extremely spotty” between 11 and 15 years, he noted.

“Although there is a little uptick seven years and longer, there is nothing to create opportunity, despite a decent supply today and [improving] ratios.”

In primary action, Citigroup priced and repriced New York City’s (Aa3/AA/AA-/AA+) $1.04 billion of Fiscal 2022 Series A Subseries A-1 tax-exempt general obligation bonds and Fiscal 2022 Series 1 reoffering GOs.

The $950 million of Fiscal 2022 Series A Subseries A-1 GOs were priced to yield from 0.10% with a 3% coupon in 2023 to 1.90% with a 4% coupon in 2042. A 2047 term was priced as 5s to yield 1.90%, and a split 2050 maturity was priced as 3s to yield 2.32% and as 4s to yield 2.07%.

The $89.505 million of Fiscal 2022 Series 1 reoffering GOs were priced as 5s to yield from 0.47% in 2026 to 1.08% in 2030.

The deal was priced for institutions after a two-day retail order period where more than $300 million was spoken for by individual mom and pop investors, according to traders.

JPMorgan Securities won the city’s $250 million competitive sale Wednesday of taxable fiscal 2022 Series A and Subseries A-2 GOs with a true interest cost of 1.4811% Coupons ranged from 0.31% in 2023 to 1.88% in 2031.

The New York Liberty Development Corp. was set to price $1.225 billion after a one-day retail order period on Tuesday, although the pricing scale was not available by the close of trading.

Miami-Dade County came to market with the largest sale in PortMiami’s history with $1.24 billion of seaport revenue bonds.

Wells Fargo Corporate & Investment Banking priced the $200.83 million of Series A-1 (A3//A/) consisted of serials ranging from 4% coupons in both 2039 at a 1.98% yield and 2041 at a 2.04% yield. A 2045 term was priced at 4%s at a 2.17%, while the $216.05 million of series A-2 (A3//A/), was priced with 3% coupons from 2045 to 2050, with 2.30% and 2.39% yields, respectively.

The $184.86 million of series B-1 (Aa3//AA-/), which contained 4% coupons in 2046 and 2050, priced at 2.20% and 2.25% yield, respectively, while the $99.66 million of series B-2 (Aa3//AA-/) serials priced with 4% coupons from 2038 at a 1.74% yield to 2043 with a 1.92% yield.

The $383.735 million of taxable Series 2021B Sub-Series 2021 A-3 revenue refunding bonds were priced at par to yield from 25 basis points above the comparable Treasury in 2023 to 158 basis points above Treasuries in 2039.The $158.65 million of taxable Series 2021B Sub-Series 2021 B-3 bonds were priced at par to yield from 28 basis points above Treasuries in 2025 to 160 basis points above Treasuries in 2038.

Assured Guaranty Municipal insured $800.615 million of the Miami-Dade bonds, consisting of the $.200.83 million of Series 2021A Sub-Series 2021 A-1 Seaport revenue refunding bonds subject to the alternative minimum tax, the $216.05 million of the Series 2021A Sub-Series 2021 A-2 Seaport Non-AMT revenue refunding bonds, and the $383.735 million of the taxable Series 2021A Sub-Series A-3 seaport revenue refunding bonds.

New deals

In addition, the Puerto Rico Aqueduct and Sewer Authority made an unexpected appearance this week, refunding all of PRASA’s 2012 Series A and B senior lien bonds, marking the second time since December 2020 that PRASA has accessed the capital markets to pursue substantial reductions in annual debt service, according to a joint press release from the Puerto Rico Fiscal Agency and Financial Advisory Authority and the Puerto Rico Aqueduct and Sewer Authority. The refinancing, which priced Tuesday and was executed through a series of transactions including an exchange, a tender for cash, a current taxable refunding and a forward delivery refunding, will generate approximately $570 million in debt service savings over the life of the refunding bonds, according to the release.

The total $1.8 billion of PRASA’s 2021 revenue bonds Series A and B senior lien bonds were refunded after the issuance which consisted of $1.66 billion in revenue refunding bonds, Series 2021A (senior lien), revenue refunding bonds, Series 2021B (senior lien), federally taxable revenue refunding bonds, Series 2021C (senior lien) and revenue refunding bonds, Series 2022A (senior lien) (forward delivery) and $208 million in premium received due to the sale of the new bonds.

The Pennsylvania Housing Finance Agency (Aa1/AA+//) priced $294.75 million of single-family mortgage revenue social bonds (non-AMT). BofA Securities structured bonds ranging from a 0.08% coupon in 2022 at par to 3% in 2051 at a 0.70% yield.

Raymond James priced the Metropolitan District of Hartford County, Connecticut’s (Aa3/AA//) $146.045 million of general obligation bonds as $130.81 million of GOs, Series 2021A, and $15.23 million of GO refunding forward deliver bonds, Issue of 2021, Series B.

Goldman Sachs was set to price the Connecticut Health and Educational Facilities Authority’s (/BBB+/BBB+/) $193 million of Stamford Hospital Issue, Series M forward delivery revenue refunding bonds.

Morgan Stanley priced the Rhode Island Housing and Mortgage Finance Corp.’s (Aa1//AA+/) $172.455 million of exempt and taxable homeownership opportunity social bonds, $144.59 million exempt Series 75-A and $27.865 million of taxable Series 75-T.

The Series 75-A non-AMT social bonds were priced with coupons ranging from 0.10% at par in 2022 to 3% in 2051 with an 0.87% yield. The taxable series ranged from 0.20% coupon in 2022 to 1.55% in 2028, all priced at par.

The day’s other deals saw similar strong demand for bonds inside 10-years, where retail investors are flocking lately, the Florida trader said.

ICI: Muni bond funds see $2.72B inflow

Long-term municipal bond funds and exchange-traded funds saw combined inflows of $2.724 billion in the week ended Aug. 11, the Investment Company Institute reported Wednesday.

It marked the 23rd week in a row the funds saw inflows. In the previous week, muni funds saw an inflow of $2.228 billion, ICI said.

Long-term muni funds alone had an inflow of $2.513 billion in the latest reporting week after an inflow of $2.123 billion in the prior week.

ETF muni funds alone saw an inflow of $210 million after an inflow of $105 million in the prior week.

Taxable bond funds saw combined inflows of $11.375 billion in the latest reporting week after inflows of $5.647 billion in the prior week.

ICI said the total combined estimated inflows from all long-term mutual funds and ETFs were $19.906 billion after inflows of $16.341 billion in the previous week.

Tapering debate

With the price stability goal met, and maximum employment “close to being satisfied,” Federal Open Market Committee members said it could be appropriate to reduce its asset purchases later this year, according to minutes of its latest meeting.

“Most participants noted that, provided that the economy were to evolve broadly as they anticipated, they judged that it could be appropriate to start reducing the pace of asset purchases this year because they saw the Committee’s ‘substantial further progress’ criterion as satisfied with respect to the price-stability goal and as close to being satisfied with respect to the maximum-employment goal,” the minutes of the July 27-28 meeting said.

Some said conditions could support tapering “in coming months,” while others believe it “was more likely to become appropriate early next year because they saw prevailing conditions in the labor market as not being close to meeting the Committee’s ‘substantial further progress’ standard or because of uncertainty about the degree of progress toward the price-stability goal.”

The discussion also suggested the panel believes Treasuries and mortgage-backed purchases should be done proportionally, as Federal Reserve Board Chair Jerome Powell suggested in his post-meeting press conference that the FOMC did not want to cut MBS purchases quicker than Treasuries as some had suggested.

The minutes seem at odds with Powell’s statement that the employment goal is “a ways away.” Despite a strong employment report, which showed nonfarm payrolls up 943,000 and the jobless rate down to 5.4%, analysts believe it will take at least one more strong report to give the Fed confidence to begin taper warnings.

Indeed, Federal Reserve Bank of Boston President Eric Rosengren said earlier this month that he’d be ready to support tapering if the next report is strong, although he’s not a voter this year, while others have said they’d like to see more solid reports and still some have said they’ve seen enough and are willing to back a reduction in asset purchases.

“The Fed remains in wait-and-see mode as the Delta variant may temporarily delay the full reopening of the economy and restrain hiring and labor supply,” said Ed Moya, senior market analyst for the Americas at OANDA. “The Fed isn’t any closer to formally announcing the reduction of their extraordinary support. Fed tapering is clearly in training camp mode, with Jackson Hole likely being a preseason game, and either the September or most likely the November FOMC meeting being the time to announce how they will pullback stimulus.”

Other analysts agreed.

“The minutes only emphasized the central bankers’ uncertainty about the path of the economy and monetary policy heading into 2022,” said Matt Weller, global head of market research at StoneX’s retail division, Forex.com. “Reading between the lines though, the majority of U.S. central bankers appear to be comfortable starting to reduce QE this year as long as there are no major downside shocks to the economy.”

The next FOMC meeting is Sept. 21-22. Next week is the Kansas City Fed’s Jackson Hole summit. The markets will closely watch Powell’s keynote from there.

In the economy in general, supply chain and labor issues as well as the increasing cost of materials continue to challenge the housing market, analysts said.

Housing starts fell 7.0% in July to a seasonally adjusted annual rate of 1.534 million from 1.650 million a month earlier while building permits climbed to 1.635 million on a seasonally adjusted annual pace from 1.594 million in June.

Economists polled by IFR Markets expected a pace of 1.602 million starts and 1.610 million permits.

“Starts have now missed expectations for four months in a row,” noted Grant Thornton Economist Yelena Maleyev. “Builders continue to face significant material, labor and land shortages. We expect residential investment to remain soft in the third quarter.”

But, she sees, supply chain problems clearing later this year, and high-end supply will increase, leaving first-time homebuyers shut out.

As home prices continue to rise and building softens, rents will soar, according to National Association of Realtors Chief Economist Lawrence Yun. “There was a housing shortage before the pandemic, and the shortage has been exacerbated during the pandemic,” he said.

Rent payments are included in the calculation of GDP.

Despite supply shortages and other issues, “the industry is on a pace to begin construction on close to 1.6 million homes this year, which would be the best year for housing starts since 2006,” said Mark Vitner, senior economist at Wells Fargo Securities.

Buyer traffic is down, he said, because of affordability and the sparse number of homes available.

Secondary bond trading

ICE Data Services reported the following muni trades Wednesday:

The Washington state Series R-2020C 2GO refunding 5s of July 1, 2022 [93974EGY6] traded in a block of $5 million+ at a price of 104.274, a yield of 0.51%. The 5s were originally priced on April 29, 2020, at 108.662, a yield of 0.96%.

The Delaware state Series 2019 5s of Feb. 1, 2028 [246381NF0] traded in a block of $5 million+ at a price of 127.857, a yield of 0.590%. The 5s were originally priced on Feb. 26, 2019 at 123.868, a yield of 2.06%.

Muni benchmarks

The triple-A benchmark scales were unchanged again Wednesday.

According to Refinitiv MMD, short yields were steady at 0.06% and at 0.08% in 2022 and 2023. The yield on the 10-year stayed at 0.88% while the yield on the 30-year sat at 1.50%.

The 10-year muni-to-Treasury ratio was calculated at 69.8% while the 30-year muni-to-Treasury ratio stood at 78.0%, according to MMD.

The ICE municipal yield curve showed bonds slipped one basis point in 2022 to 0.05% and was steady at 0.09% in 2023. The 10-year maturity was at 0.91% and the 30-year yield was at 1.49%.

The 10-year muni-to-Treasury ratio was calculated at 72% while the 30-year muni-to-Treasury ratio stood at 78%, according to ICE.

The IHS Markit municipal analytics curve showed short yields steady at 0.07% and 0.08% in 2022 and 2023, respectively. The 10-year yield was at 0.90% and the 30-year yield at 1.48%.

In late trading, Treasuries were little changed as equities were mixed.

The 10-year Treasury was yielding 1.27% and the 30-year Treasury was yielding 1.92%. The Dow Jones Industrial Average dipped 0.40%, the S&P 500 decreased 0.30% while the Nasdaq inched up 0.03%.

Primary to come

The City of Aurora, Colorado (/AA+/AA+/) through its Utility Enterprise is set to price on

$266.7 million of taxable first-lien water refunding revenue green bonds. Morgan Stanley & Co. LLC.

The California Statewide Communities Development Authority (/A-/A/) is set to price $196.285 million of Front Porch Communities and Services series 2021A revenue bonds on Thursday. BofA Securities.

The California Statewide Communities Development Authority (/A-/A/) is also set to price $109.61 million of taxable Front Porch Communities and Services series 2021A revenue bonds on Thursday. BofA Securities.

The Connecticut Health and Educational Facilities Authority (/BBB+/BBB+/) is set to price on Wednesday $193 million of Stamford Hospital Issue, Series M forward delivery revenue refunding bonds. Goldman Sachs.

The University of North Dakota (A1///) is set to price on Thursday $144.32 million of certificates of participation: $127,525 million of series A, serial 2024, 2027-2030, terms: 2032,2034,2036,2039,2041,2046,2051,2061 and $16.795 million of refunding series B, 2022-2034. Stifel, Nicolaus & Company, Inc.

The Iowa Finance Authority/Palm Beach County Health Facilities Authority (//BBB/) is set to price on Thursday $120.465 million of Lifespace Communities, Inc. revenue refunding bonds. Ziegler.